Cristian Martin

Vista Power (NYSE:VIST) is likely one of the largest producers and the most important exporter of shale oil in Argentina’s Vaca Muerta basin.

I wrote concerning the firm in October 2021 (the second article on the corporate in In search of Alpha, when the inventory traded at $6.5 in comparison with $30 at this time) and in January 2023, each instances recommending its buy.

These articles have extra detailed descriptions of the corporate. Succinctly, I beneficial the title due to its low value of extraction, low leverage, give attention to oil and never pure fuel, and low valuation.

Since then, the corporate has continued executing the identical technique. It has decreased drilling and lifting prices and has divested belongings to focus much more on shale oil.

At this time, the corporate’s value displays its valuation a bit of higher than earlier than, and due to this fact, the margin of security that the safety affords is decrease. Nonetheless, I imagine the inventory nonetheless trades nicely beneath what the corporate is value, particularly contemplating the funding plans of the corporate.

Self-financed progress

Since I wrote the primary article about VIST, oil costs have risen, decreased, and gone sideways. 2021 was an important bull yr, whereas 2022 was unstable and 2023 a bit of extra secure.

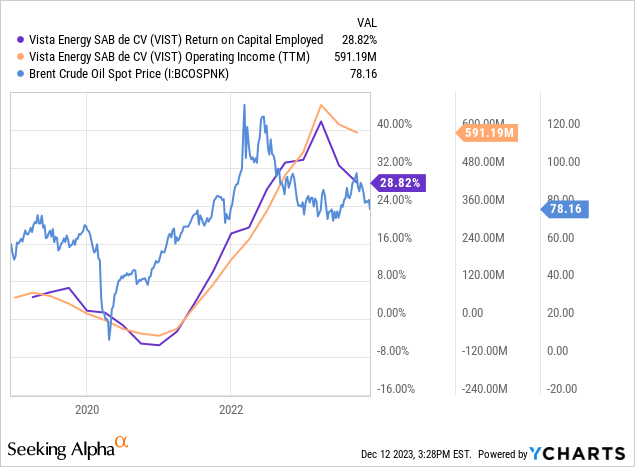

That didn’t matter to VIST. The corporate has constantly elevated manufacturing and may now pump 50 thousand barrels day by day. Additional, the corporate has lowered prices: nonroyalty prices have decreased by 50% since 2018. This has been achieved by working the expertise curve down. The extra the corporate drills, the extra it could possibly enhance its efficiencies.

This has generated an explosion in EBIT that’s correlated with larger oil costs but in addition corresponds to the execution of the corporate’s plan. VIST managed to put up ROCE above 25%.

Additional, VIST has elevated its manufacturing capability by way of the money flows it generates from its belongings with out growing leverage.

This permits the corporate to be in a comparatively comfy place at this time. It might repay all its money owed with one yr of working money flows if it needed to disinvest, even contemplating upkeep CAPEX.

Plans for the longer term

This yr, the corporate offered belongings centered on standard exploration within the Vaca Muerta basin. With out these, the corporate has nearly no working belongings exterior Vaca Muerta unconventional.

VIST desires to proceed specializing in shale oil. The corporate’s plans embody growing manufacturing capability to 70 thousand barrels per day by the top of 2024 and probably 100 thousand barrels by 2026.

Following a constant technique, the corporate doesn’t plan to take debt to finance these investments. It expects to spend $780 million in CAPEX yearly, absolutely financed by way of working money flows. It doesn’t anticipate to pay down debt or dividends, however somewhat, if all the pieces works appropriately and with an oil value of $65, accumulate an extra $1 billion in money.

There will probably be one large problem in VIST’s highway and that’s transport capability. The corporate might broaden quicker than at this time however is constrained by the principle oil pipeline from Vaca Muerta to the export and remedy market of Bahia Blanca. The pipeline is managed by Oldelval, which has introduced enlargement plans, however these rely on receiving financing and a comparatively unstable regulatory framework. I might anticipate the brand new authorities to be open to personal funding that might increment exports, however that is nonetheless a danger.

A easy mannequin

The corporate’s low-cost construction and low leverage are its principal belongings. In a commodity business, the low-cost, low leveraged producer is at a lot decrease danger as a result of it could possibly keep on the black throughout market downturns. Doubtlessly, the corporate might purchase belongings from extra leveraged gamers.

On this case, VIST has posted extraction prices of $16 per barrel. This consists of working bills of $5, drilling (or D&A) of $9, and midstream of $1, roughly. On prime of that, we have now so as to add $5 of royalties per barrel. Up up to now, we have now had variable bills. SG&A has proven to be comparatively secure at 10% of revenues, however to be extra conservative, and anticipating increasing manufacturing, we are able to take into account it variable (much less leverage) at $6 per barrel.

This yields a breakeven value per barrel of $27. It signifies that even paying for upkeep CAPEX (included in drilling prices by way of D&A), the corporate wants a whole crash of oil costs to enter working pink. At $27, it could possibly change its wells and maintain manufacturing regular with out dropping cash. That is the corporate’s ‘moat’. Royalties might lower if the brand new authorities decides to get rid of the export taxes presently in place (8% of FOB worth).

As all the time with Argentinian shares, curiosity expense mixes true curiosity with capital changes by way of inflation. Additionally, rates of interest in USD have been extraordinarily low in Argentina due to capital restrictions. VIST has been capable of finance at lower than 5% this yr, and I am fairly certain it isn’t a lower-risk borrower than the Federal Reserve.

My strategy to work round that is to transform all of the debt to pesos utilizing the official fee and apply a conservative rate of interest. For instance, 10% on the above charted $700 million in money owed yields $70 million in curiosity bills going ahead, assuming no additional debt issuing and rolling over the present debt at 10% (at this time, the efficient fee is way decrease).

Lastly, the Argentinian earnings tax fee of 35%.

Now, it is time to work with costs.

There’s a 10-15% value hole between exports and native costs. That is unimportant for our functions for 2 causes: first, we are able to take into account the efficient value per barrel as a combination between the export and the nationwide value; second, the brand new authorities is nearly assured to get rid of this distinction by authorizing free value setting within the home oil market. This convergence alone might improve VIST’s revenues by 5/10% (contemplating 50% of gross sales are within the home market).

Additionally, we have now to imagine a reduction to Brent costs. This has usually been round 10% for exports, so we are able to assume 15% as a combination between the nationwide and export costs (once more, though I imagine this discrepancy will disappear).

Now, we’re able to venture internet earnings for a sequence of potential costs. The account is straightforward. VIST costs are 85% of Brent costs. From this, we take away $27 in variable prices per barrel. We multiply the working earnings per barrel by the 70 thousand barrels anticipated day by day (25.5 million per yr). Then, we take away $70 million in curiosity bills. From the remaining, we take away 35% of earnings taxes.

| Brent costs | 50 | 55 | 60 | 65 | 70 |

| VIST costs | 42.5 | 46.7 | 51 | 55.3 | 59.5 |

| VIST op inc per barrel | 15.5 | 19.7 | 24 | 28.3 | 32.5 |

| VIST op inc (million USD) | 387 | 502 | 612 | 721 | 828 |

| VIST pre tax inc (million USD) | 317 | 432 | 542 | 651 | 758 |

| VIST internet inc (million USD) | 206 | 280 | 352 | 423 | 492 |

This mannequin isn’t advanced and doesn’t faux to be so. The concept is to indicate how, with some conservative measures (SG&A as a variable value, larger rate of interest, and 35% decrease oil costs), the corporate continues to be buying and selling at worth costs.

Conclusions

VIST presently trades at a market cap of $2.5 billion.

Given its present value and financing construction, it is a 12x a number of of what the corporate might probably earn, with the Brent oil barrel at $50. Contemplating the more moderen $70 per barrel, it turns into 5x.

To me this implies the corporate affords quite a lot of margin of security. Oil costs ought to fall to pre-pandemic ranges for the corporate to commerce at what may very well be thought-about an appropriate 8% earnings yield. The corporate stays undervalued if oil costs are sustained at present ranges or rise larger.

Additional, its administration has proven the capability to develop the corporate with out leveraging whereas on the similar time enhancing prices. It is a signal of high quality. Lastly, some enhancements in Argentina’s laws (eradicating 8% export taxes and unifying home and worldwide costs) might additional enhance VIST’s earnings beneath all situations.