K Neville/iStock via Getty Images

The following segment was excerpted from this fund letter.

Our Korean preferred stocks, the nonvoting shares of Wilh. Wilhelmsen (OTC:WLLSF), and Vistry (OTCPK:BVHMF) all feature characteristics of compound mispricings. The thesis for higher returns include: the closing of the voting, nonvoting, holding company and multiple business valuation gap, evidence of better governance and liquidity and/or the decline or sale of the legacy business. We are also looking for corporate actions such as spinoffs, sales, share buybacks, or holding company transactions and overall cash flow growth.

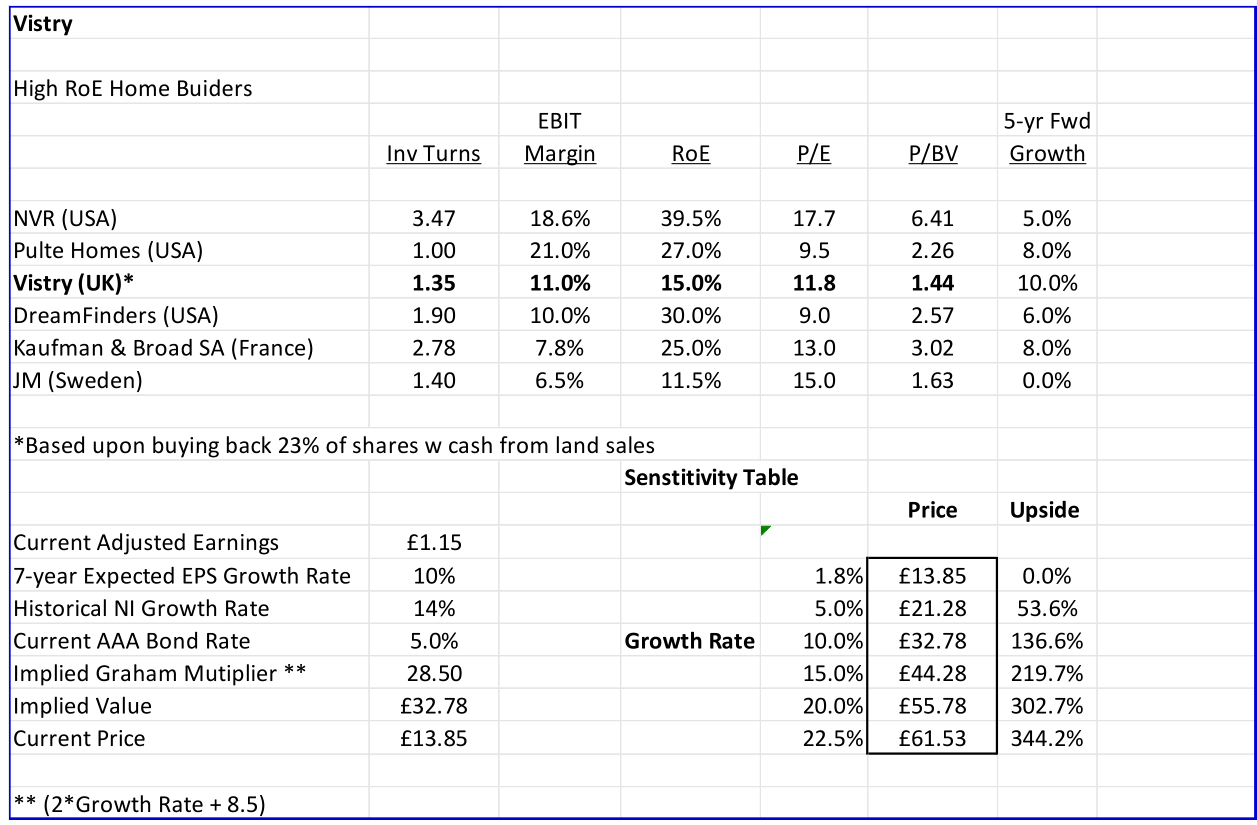

Vistry, one of our largest holdings, is a compound mispricing as it is in the process of exiting its land heavy traditional homebuilding business and becoming a pure play, land light homebuilder, similar to NVR and Dreamfinders in the United States.

Vistry is the largest partnership homebuilder in the UK. It renovates housing and builds new housing in partnership with local housing authorities. The local housing authority provides the land for development or existing buildings for renovation, and the partnership builder executes the planned construction. Some of the completed units are sold at market rates, but most of the units will contribute to the affordable housing stock. Originating the homebuilding agreements requires a network of personnel to develop the relationships and negotiate the deals with local housing authorities. The builder then upgrades and builds the units based upon an agreed scope. The UK recently elected a Labour government committed to expanding the housing stock. Builders like Vistry will be in a good position to provide the services to make this promise a reality.

Since the builder does not purchase the land, the process has historically generated after-tax RoE in the mid-20% in comparison to the mid-teens for the traditional land heavy model. Countryside Properties was the first to develop a partnership only homebuilder. Due to execution issues, Countryside did not meet its goals. After shareholder activism the CEO was ousted and Countryside merged with Vistry. As a part of the merger, Vistry decided to adopt the partnership only model and is now the largest partnership focused homebuilder in the UK. As a part of the transition to a partnership builder, Vistry will generate about £1 billion in excess cash primarily from sale of the land inventory which they expect to use to re-purchase shares. Currently, Vistry generates after-tax RoEs of 15% and is expected to increase to the mid-20s in the next five years. Management expects to generate annual net income in the £500m range over the next 3-5 years which would translate into £1.85 per share, assuming the £1 billion in proceeds from asset sales are used for share repurchases. So in five years, Vistry will be a partnerships home builder with returns on invested capital in the mid 20% and a steady source of revenue from local housing authorities, the UK government and private individuals. Based upon Vistry’s current stock price, Vistry is selling for 7x 3-5 yr forward EPS.

Vistry is a great business operationally and is in a good position to grow. The largest drawbacks at this point are the timing of the partnership builds (potential home construction slipping beyond management’s expectations) and competition. Competition should be nominal as Vistry has much more experience and a larger scale and scope of services versus other competitors in the market. If construction projects are completed and delivered on a slower schedule than planned, holding costs for Vistry will be smaller than traditional home building.

Below is our current valuation of Vistry:

|

Disclaimer This letter does not contain all the information that is material to a prospective investor in the Bonhoeffer Fund, L.P. (the “Fund”). Not an Offer: The information set forth in this letter is being made available to generally describe the philosophies of the Fund. The letter does not constitute an offer, solicitation or recommendation to sell or an offer to buy any securities, investment products or investment advisory services. Such an offer may only be made to accredited investors by means of delivery of a confidential private placement memorandum, or other similar materials that contain a description of material terms relating to such investment. The information published and the opinions expressed herein are provided for informational purposes only. No Advice: Nothing contained herein constitutes financial, legal, tax, or other advice. The Fund makes no representation that the information and opinions expressed herein are accurate, complete or current. The information contained herein is current as of the date hereof but may become outdated or change. Risks: An investment in the Fund is speculative due to a variety of risks and considerations as detailed in the Confidential Private Placement Memorandum of the Fund, and this letter is qualified in its entirety by the more complete information contained therein and in the related subscription materials.

|

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.