kokouu/E+ through Getty Pictures

The Announcement

Vroom (NASDAQ:VRM) introduced yesterday that they are going to be winding down their used vehicle dealership business. They mentioned they are going to be halting each shopping for and promoting on Vroom.com and trying to promote their present stock by way of wholesale channels. It appears that evidently the rationale for this resolution was that they not may entry financing wanted to develop and that growth was essential to ever attain profitability.

I applaud administration for realizing there was no option to get their present operations to profitability and simplifying the enterprise earlier than they get into an even bigger gap. Their hand might have been pressured, since they clearly had been trying to get additional financing and preserve scaling up, however could not discover sufficient financing to get it accomplished. In my eyes although, that is the good transfer. They grew to become a public firm through the pandemic when there was tons of cash accessible for IPOs and so they had been attempting to scale up with used automobile costs that had been sky-rocketing from the pandemic. Actuality hit shortly after though- used automobile costs dropped and getting new stock stayed costly since all dealerships had been searching for extra. There simply wasn’t a lot margin left for a low barrier to enter the market.

Moreover, I feel the used automobile shopping for market is simply too fragmented. Apart from Vroom and Carvana (CVNA), there are CarMax (KMX), impartial old-school dealerships, and lots of others. There are a number of opponents, with few providing any actual worth over the others. This drives it to be a low-margin, low-barrier-to-entry enterprise. With all the complications of delivery vehicles and titles and differing state and federal rules, the prices mount shortly. In my eyes, it might take a a lot, a lot bigger scale to function an ecommerce automobile enterprise profitably.

What’s Left?

For many who do not observe Vroom very intently, you would possibly ask, “Isn’t buying and selling cars their entire business?” The brief reply isn’t any. Whereas Vroom will get nearly all of its revenues from their ecommerce operations, it additionally owns United Auto Credit score Company and CarStory.

United Auto Credit score Company (UACC) is their financing division in a way. Whereas Vroom will not have their very own vehicles to supply captive financing on, they’ve third-party prospects that use UACC and so they can proceed to finance autos that manner.

Whereas auto-financing is a fairly easy tack-on enterprise for Vroom, I am rather less certain how they become profitable from CarStory. Within the Vroom wind-down announcement hyperlink above, they state that CarStory is, “a leader in AI-powered analytics and digital services for automotive retail.” The title CarStory, to me, additionally signifies that they preserve a historical past of vehicles, with accidents and servicing data, just like CarFax.

Nevertheless, after I go to Carstory.com, it appears to only be a website that means that you can seek for autos to purchase by location/worth/make/mannequin/kind/and so forth. All vehicles I’ve tried clicking on, simply hyperlink to CarFax, so I assume CarStory does not present their very own historical past. In abstract, CarStory to me simply looks like a database of used autos that makes use of CarFax to point out a historical past. So evidently CarStory is usually a database of used autos (owned by many alternative entities, not simply Vroom’s used autos) and perhaps they leverage the massive quantities of information to provide insights on pricing, sale velocity, and so forth.

Valuation

So now with the background information of what Vroom is doing and what items will likely be left, valuing the remaining firm principally comes right down to how a lot of their present tangible ebook worth we predict they may be capable of maintain onto whereas they wind down, and the way a lot worth might be attributed to their remaining items (UACC and CarStory).

At this time, after the ~40% sell-off following the announcement, their market cap is round $42M and their tangible ebook worth was final listed on their Q3 2023 earnings as $119.6M. Put one other manner, their present share worth as of writing that is $0.30 and their tangible ebook worth per share is $0.86. I like to make use of tangible ebook worth as a result of it takes out any goodwill and different intangibles that get included in basic ebook worth. In these types of wind-down or sell-off asset situations, there may be normally little or no or no worth in intangibles. These values present that as of the top of Q3 2023, there can be nearly triple the worth within the property (after subtracting debt) than the present market cap.

Nevertheless, assuming that Vroom did not all of the sudden develop into worthwhile, we all know that they may have misplaced more cash in This fall, in addition to proceed to lose cash through the wind-down interval. They misplaced between $0.40 – $0.50 of tangible ebook worth every of the previous few quarters, so there’s a number of proof that the tangible ebook worth on the finish of This fall will likely be fairly near their present market cap.

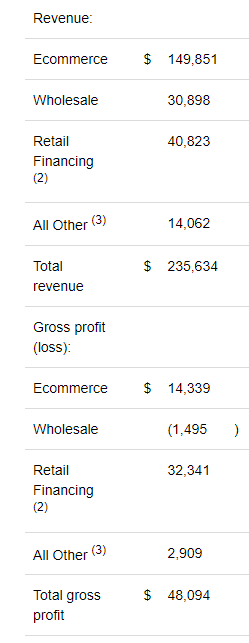

I additionally need to level out that they introduced they are going to be promoting their autos wholesale, which normally loses cash, even on the gross revenue stage (excluding operational prices). Principally, I take this to imply that whereas promoting vehicles by way of ecommerce is extra worthwhile on a unit stage, they’re selecting to cease promoting that manner instantly as a result of it nonetheless prices a lot extra to run from an operations perspective. Put one other manner, they assume they may lose much less cash by promoting in bulk wholesale, even whereas promoting particular person autos at a loss as a result of they’ll wind down operations quicker and lay off extra workforce instantly. Here is a breakdown of Vroom’s newest quarter for revenues and gross earnings:

Q3 2023 Earnings Outcomes (Q3 2023 Earnings Outcomes)

With some fast calculations, we are able to see that the gross revenue margin on Ecommerce was ~10% in Q3, Wholesale was unfavorable, Retail Financing was ~80%, and All Different (which incorporates CarStory) was ~20%. One huge optimistic from this data is that Retail Financing is by far their most worthwhile phase on a gross revenue foundation (I did not see any escape of administrative prices by phase) and they’re in fact conserving that phase. One huge unfavorable is that we see simply how dangerous of a deal they get once they need to promote vehicles by way of their Wholesale phase. Since they mentioned they are going to be promoting all remaining stock this fashion, I’ve to imagine they are going to be taking a loss on these property and never getting the complete worth out of them that’s at present listed on the stability sheet.

The entire above bodes even worse for his or her tangible ebook worth because it doubtless means they will not even get as a lot out of their property as is listed on their stability sheet. Between their property doubtless needing a haircut, the related prices of shedding a workforce (severance packages and such), and the truth that they will nonetheless need to preserve sufficient personnel on to run their different companies and the whole lot related to being a public firm, I anticipate their tangible ebook worth to truly be unfavorable in spite of everything that’s taken into consideration.

However now again to the valuation of the remaining items. Vroom announced they had been shopping for UACC for $300M again towards the top of 2021 and completed the acquisition in early 2022. I anticipate there may be nonetheless worth left in UACC, however I additionally doubt it’s price as a lot as they paid for it. Since public corporations nearly at all times pay a premium when shopping for one other enterprise, I’d assume they might solely be capable of promote UACC for round half, although I admit that is a complete guess. Maybe it is price even much less or maybe they expanded the enterprise and it is now price greater than they purchased it for.

Vroom additionally purchased CarStory for $120M again on the finish of 2020. For a similar causes, I assume it’s price lower than they paid for it, however it’s an enormous query mark as effectively. The truth that they declare they’ve an AI providing most likely helps their valuation proper now, however to me, it is nonetheless principally only a automobile sale database. In complete, I’ll be assigning round $200M for UACC and CarStory in complete.

After subtracting out the unfavorable tangible ebook worth I anticipate from winding down operations and including this assigned worth very roughly estimated at $200M for UACC and CarStory, that might depart as a lot as $150-$200M in tangible worth left. Which will seem to be rather a lot in comparison with their present market cap of $42M, however since they do not plan on promoting off UACC or CarStory as a part of this wind-down, I might prefer to see the working margins of what stays of the corporate earlier than deciding if it is a inventory price holding. As with all holding, it is solely price what you may promote it for and since Vroom does not plan on promoting off UACC or CarStory, it does not actually matter what their worth is till they do or till we are able to see how a lot revenue they’ll generate alone.

Conclusion

I went into this text to see if the sell-off was too giant and if there was any meat left on the bone, so to talk. Nevertheless, it appears to me that there’s doubtless a unfavorable worth left within the remaining automobile property after accounting for the debt left on the stability sheet and the continued prices of winding down operations.

There’s a respectable likelihood that UACC and CarStory can find yourself being price greater than the deficit I anticipate they will be in after promoting off their automobile stock property. We all know that UACC is their most worthwhile phase on a gross revenue foundation, however that’s normally true with financing. Whereas financing may be very worthwhile and there is a cause so many banks exist, it takes carrying a number of loans on the stability sheet and is riskier from a credit score perspective. It additionally stays to be seen what number of basic and administrative prices they will have after winding down the ecommerce phase.

Even when there may be some worth left within the remaining companies after winding down their automobile dealership enterprise and accounting for debt left, it’s a threat with considerably restricted upside and a number of unknowns. Following this evaluation, I feel there’s a respectable likelihood that UACC and CarStory will likely be price greater than what they will lose in winding down, however I personally don’t plan on doing any speculative shopping for on the remaining items, till I get extra info on their operational efficiencies additional into the method.

Editor’s Notice: This text covers a number of microcap shares. Please pay attention to the dangers related to these shares.