Jacek_Sopotnicki

Funding Thesis:

Warner Bros. Discovery (WBD) is a media and entertainment business that operates primarily within the segments of Studios, Networks, and DTC. Some notable manufacturers they personal embrace DC, Recreation of Thrones, Harry Potter, and plenty of extra family names whereas some of the first platforms they function by means of are TNT Sports activities, Max, and CNN. Warner Bros. Discovery was fashioned by means of a Reverse Morris Belief the place AT&T (NYSE:T) spun off warner media and merged it with Discovery.

Warner Bros. Discovery Manufacturers (In search of Alpha)

The market has not rewarded the brand new Enterprise nicely with Warner Bros. Discovery falling nearly 70% because it started buying and selling round $8 from its peak of just about $25. The first issues surrounding the enterprise are the large debt load of over $40 billion that the enterprise boasts in addition to worries about the structural decline in WBD’s linear networks which account for the overwhelming majority of their money technology but have declined over the previous few years. Though the issues surrounding WBD are legitimate, I imagine a lot of it’s overblown and misunderstood presenting an enormous alternative to purchase this enterprise at a steep low cost to its intrinsic worth. I imagine that almost all of the declines in WBD’s linear networks phase will likely be met with principally proportional features of their DTC phase as they start to maximise profitability domestically and increase internationally which is a principally untapped market with great potential. Furthermore, though WBD’s debt load is giant, they’ve managed to pay again $5 billion in just the past year bringing their web debt to only 4x EBITDA. As WBD continues to provide huge sums of money and pay down their debt whereas EBITDA will increase, their leverage ratio will quickly drop as shareholder fairness within the firm will increase. Fairly presumably probably the most missed component of WBD is that the enterprise generated over $6 billion in free cash flow over the previous yr that means the enterprise trades at lower than 4x free money move because of their roughly $20 billion market cap. Even when accounting for WBD’s web debt of $40 billion, the enterprise nonetheless trades at simply 10x free money move to enterprise worth. Though their free money move was barely inflated previously yr as a result of writer and actors strike, even when WBD’s money flows barely drop or stay the identical over the following few years, their upside potential stays great.

Breakdown of Segments:

As beforehand talked about, Warner Bros. Reviews their outcomes by means of their segments of Studious, Networks, and DTC. Their studios phase has been traditionally unpredictable as a result of risky nature of how movies carried out and their means to provide them at a well timed price. Lots of the current movies WBD launched have been doing nicely such because the blockbuster hit “Barbie”, “Willy Wonka” and “Dune 2” though their administration has hinted in direction of a weaker content pipeline within the following years as a result of impression of the strikes. Their linear networks have traditionally accounted for almost all of the profitability throughout the enterprise but have been declining over the previous few years as cord-cutting continues and shoppers start pivoting in direction of streaming companies. Though a lot of their networks are family names comparable to CNN, TNT Sports activities, TLC, Discovery Channel, Foot Community, Cartoon Community, and HGTV, the pattern is cord-cutting is right here to remain though the tempo at which it happens is important. Lastly, their DTC segment which incorporates their streaming service “Max” is their quickest rising phase which ought to act as a automobile to offset the decline of their linear networks. The facility of Max is great and WBD is ready to leverage their various manufacturers and IP to current a service that features a robust move of recent content material from their studious phase in addition to the manufacturing of recent reveals, sports activities streaming from TNT which incorporates the wildly popular March Madness, and 24/7 reside information introduced by CNN. The basically robust nature of their streaming service provides them potential to compete with different giant gamers within the discipline comparable to Netflix, Hulu, and Disney + whereas main development avenues stay of their enlargement internationally. General, WBD’s studios and networks segments usually are not the strongest but the robust IP the enterprise has gathered over time will enable them to proceed rising by means of DTC and hopefully offset potential declines within the different segments. For my part, you will need to observe that for WBD’s to be a worthwhile funding, they don’t must develop very a lot, merely sustaining their present stage of money flows and paying down debt can be greater than sufficient for great appreciation within the share-price to be realized as a result of companies’ present dirt-cheap valuation.

Warner Bros. Discovery Segments and Manufacturers (WBD investor Presentation)

Monetary Breakdown:

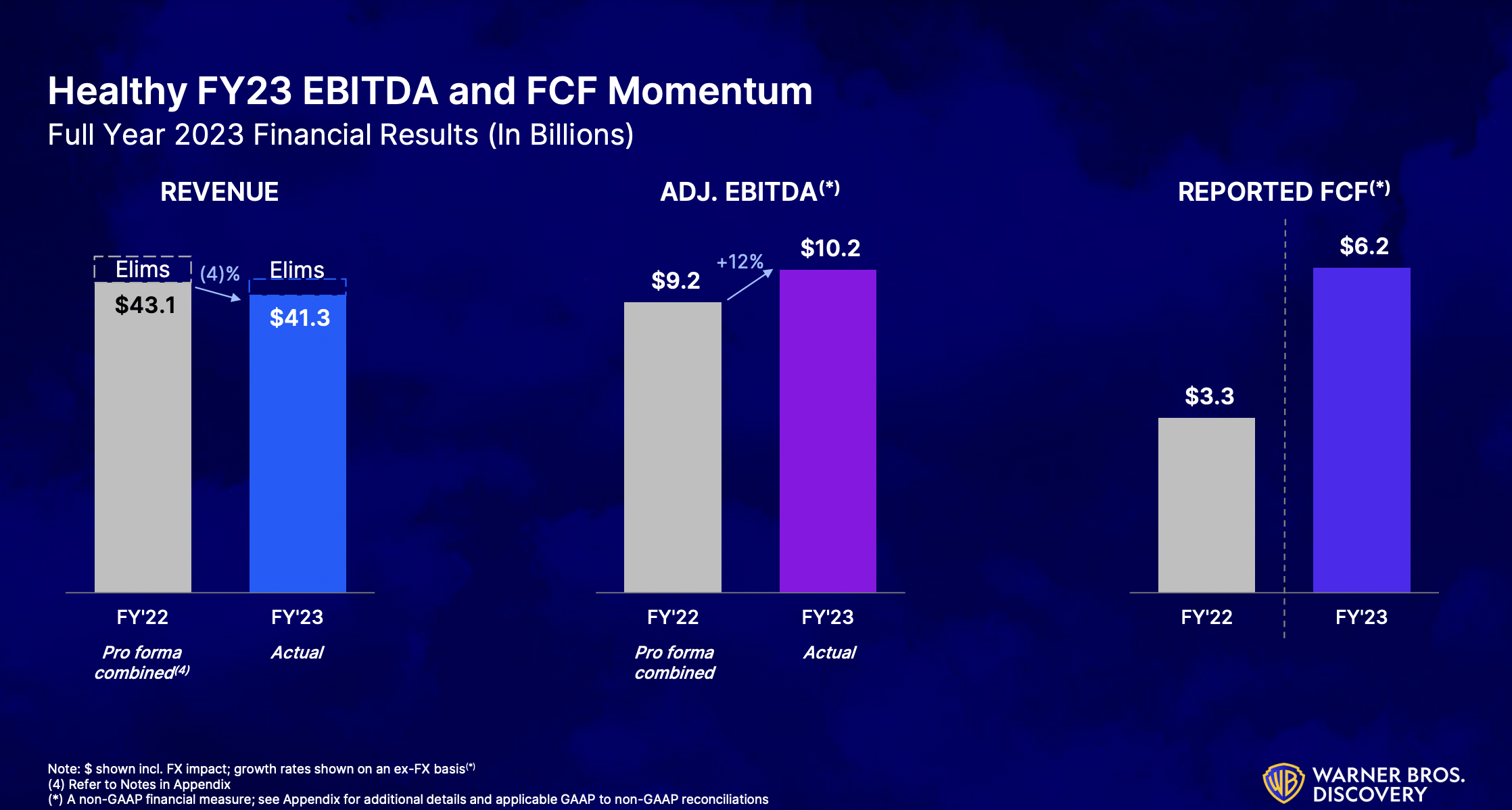

As a result of WBD’s new construction, there are a lot of one time expenses of non-cash items which impression their profitability of a GAAP foundation in a way that doesn’t replicate the precise money the enterprise produces. As a result of impression of one-time non-cash bills, I’ll primarily give attention to just some gadgets, income, web debt, EBITDA, and free money move. Financially, these are the few key metrics which can be wanted to judge the viability of the enterprise. For the complete yr 2023, WBD’s revenue declined barely by 4% on a pro-forma foundation from $43.1 billion to $41.3 billion. Throughout that very same time period, their adjusted EBITDA grew 12% to $10.2 billion from $9.2 billion whereas their FCF exploded to $6.2 billion from $3.3 billion within the earlier yr. General, the pattern seems to be that WBD is specializing in maximizing profitability and capturing synergies underneath the brand new enterprise construction.

WBD monetary outcomes 2023 (WBD investor presentation)

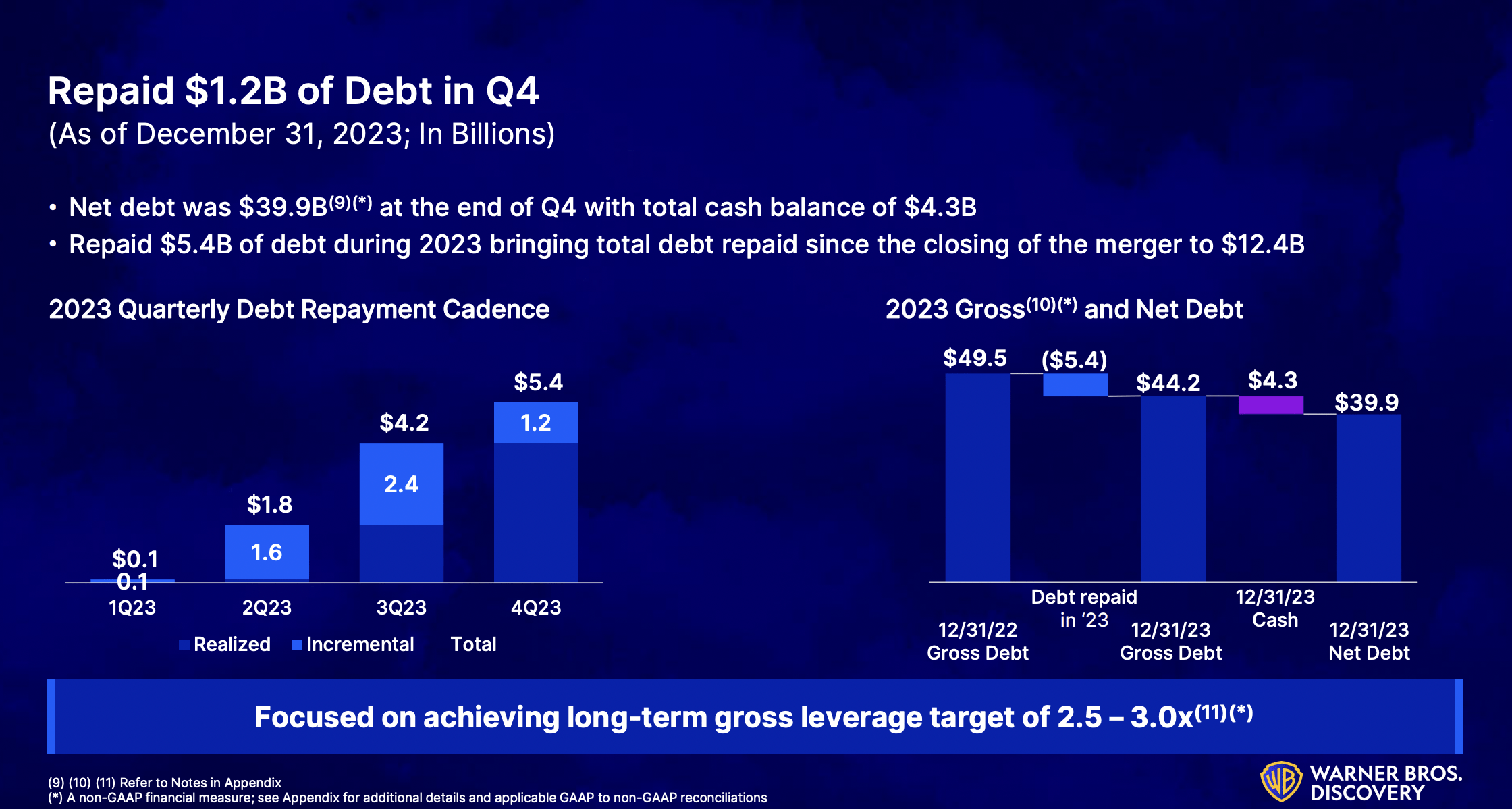

WBD’s boosted their synergies target to $5 billion from the unique $3 billion they anticipated. Moreover, WBD will probably be unable to keep up their previous yr stage of free money move as hinted within the earnings name by means of the lack of guidance and other commentary but a drop in free money move yr over yr doesn’t jeopardize the funding thesis in any regard. Even when their free money move dropped a considerable 17% to $5 billion WBD would nonetheless commerce at simply 4x free money move whereas they will proceed paying down their debt at a speedy price. With reference to their debt, WBD at the moment has $39.9 billion in web debt after repaying $5.4 billion previously yr. Though their debt load continues to be 4x EBITDA which is above their goal vary of 3x EBITDA, assuming they will keep no less than 5 billion in free money move and pay down roughly $3.5 billion a yr they might attain 3x leverage in lower than 3 years.

WBD Debt compensation (WBD investor presentation)

Massive Debt Load:

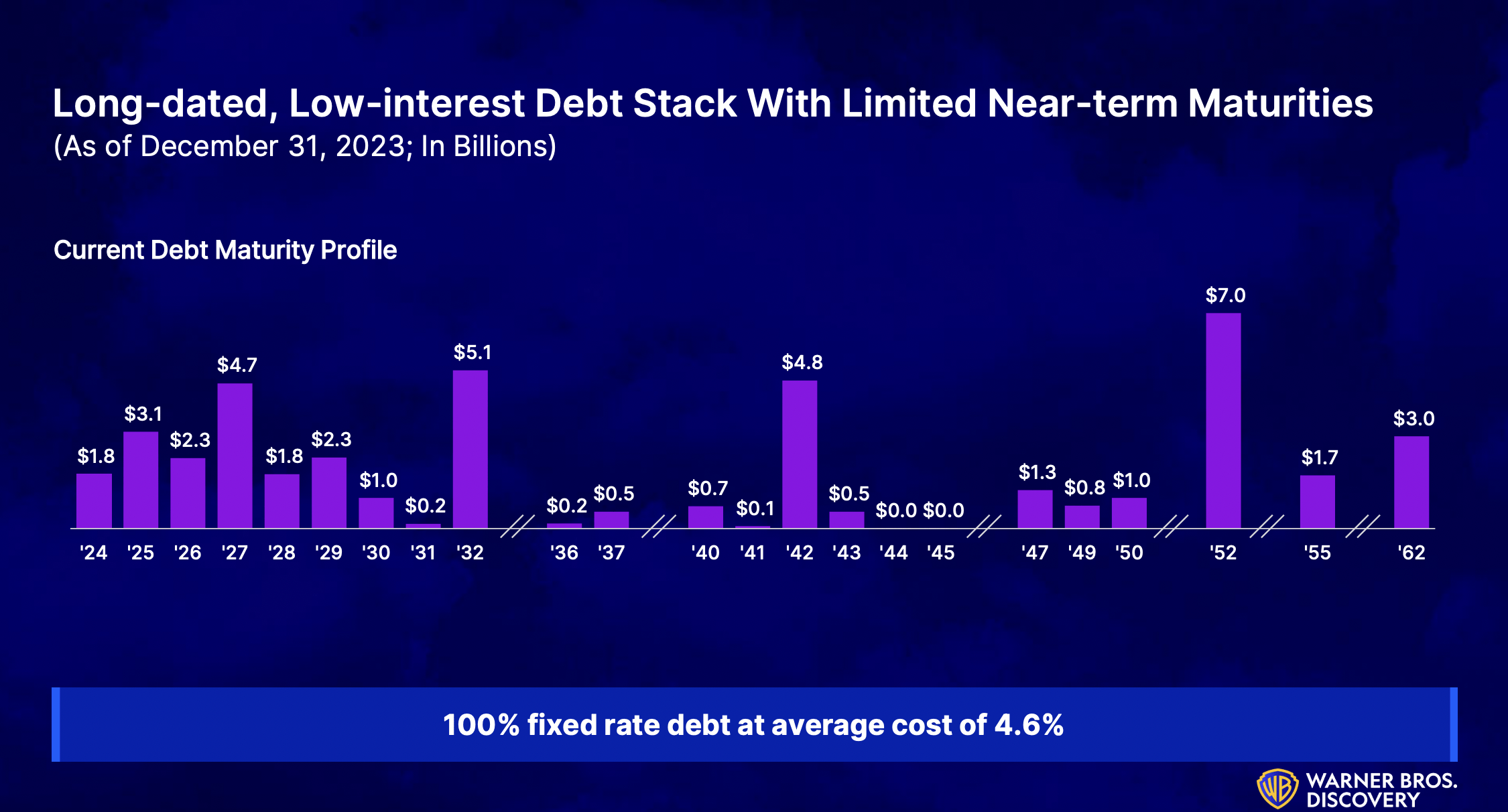

The first impediment that many individuals view when investing in WBD’s is the large debt load and the present excessive rate of interest surroundings. The market utterly misunderstands WBD’s debt scenario. First, excessive rates of interest are literally a fantastic factor for the enterprise not a nasty factor. Let me clarify. Presently, 100% of WBD’s debt is fixed at an average cost of 4.6% due to this fact rises in rates of interest do not instantly impression the curiosity on their debt load to any extent. Moreover, increased rates of interest are a danger if WBD has to refinance debt on account of a considerable amount of their debt maturing in a single yr. When observing their debt maturity profile, it seems this isn’t a significant concern as even the biggest funds they should make within the subsequent 10 years in 2027 and 2032 of $4.7 and $5.1 billion respectively can simply be managed by their present ranges of free money move.

WBD Debt Maturity Profile (WBD investor presentation)

Now, it is necessary to debate how increased rates of interest are a greater factor for WBD by way of paying down their debt. When rates of interest rise the value of bonds fall. This can be a main profit for WBD as they will retire debt at beneath face worth. Though WBD is just not allowed to pay again debt holders earlier than the maturity date as a result of covenants on their debt, they will purchase their debt on the open market and pay themselves the curiosity to beat such an impediment.

Valuation:

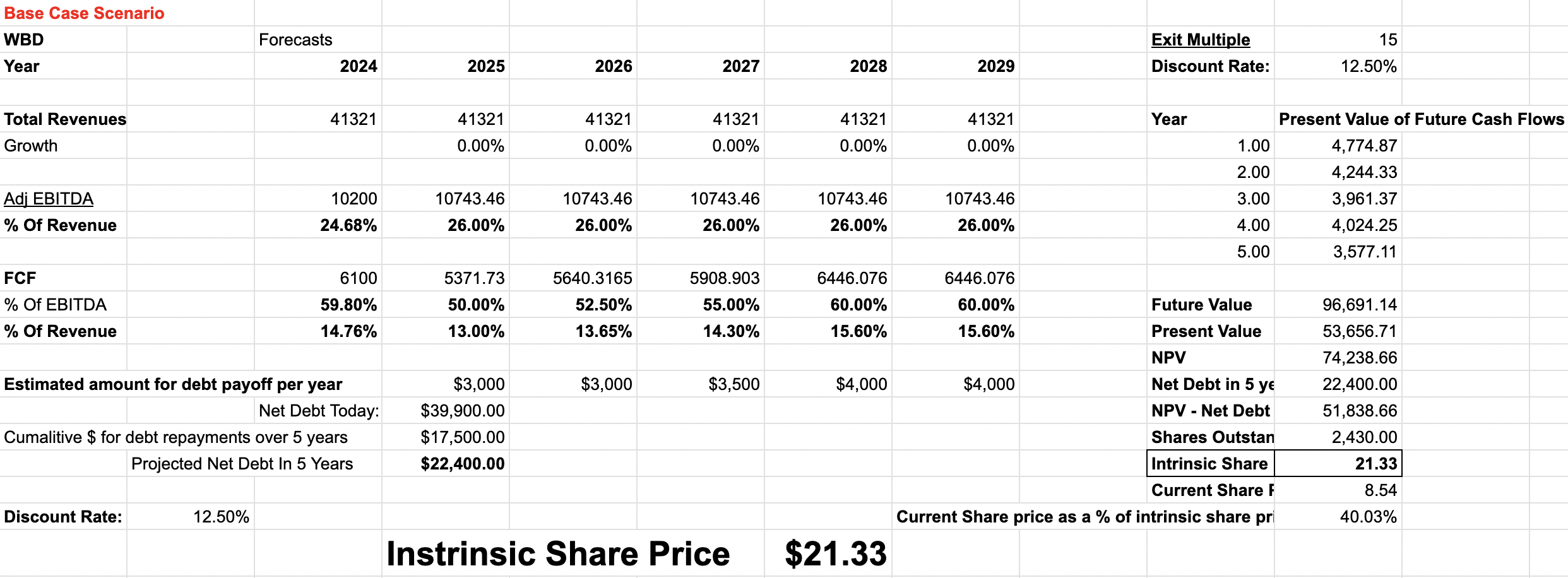

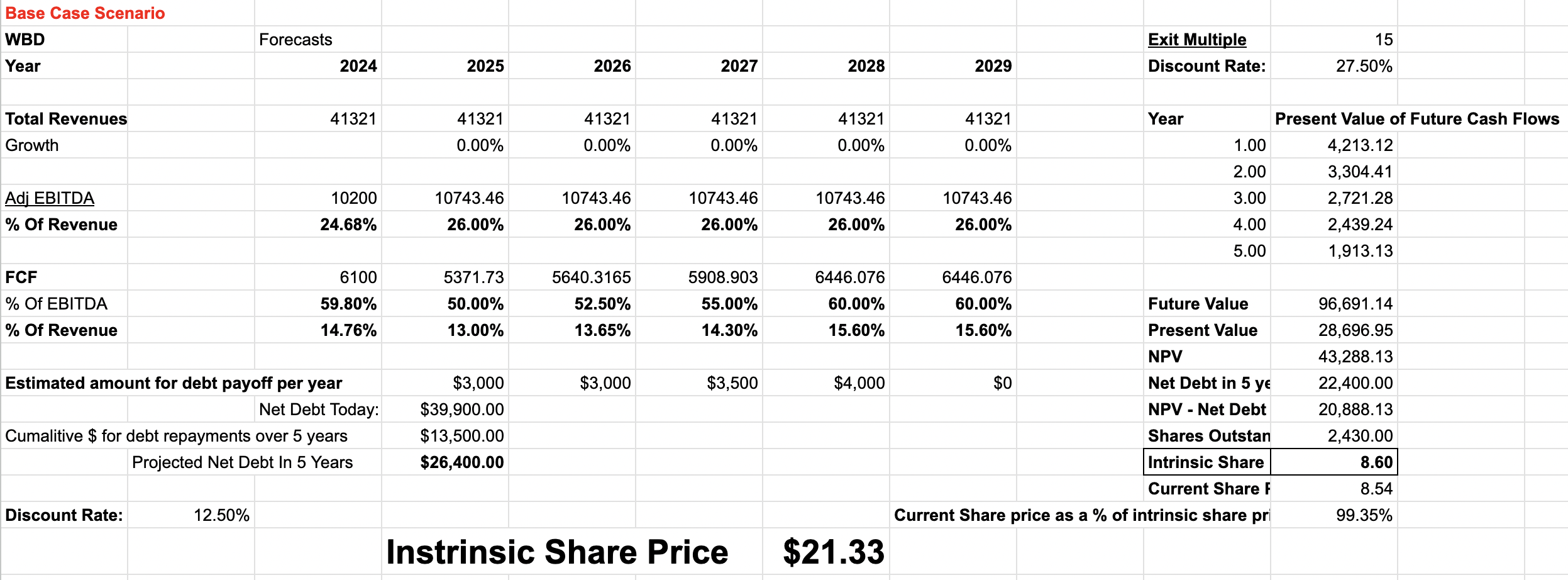

To worth WBD I’ll leverage a reduced money move evaluation (DCF) with extraordinarily conservative assumptions to reveal how undervalued the inventory is. Within the case of WBD, to adequately account for the companies’ means to pay down their debt over the following 5 years which is the time horizon I will likely be utilizing to investigate the enterprise, the web debt determine I’ll enter will likely be a projection of their web debt 5 years from now as an alternative of as we speak which contradicts how companies’ are sometimes valued utilizing a DCF evaluation. My reasoning behind inputting their debt determine 5 years from now as an alternative of as we speak is that the curiosity bills WBD pays over the following 5 years are already accounted for within the projection of their free money move due to this fact I’d be double penalizing them by subtracting the worth of their debt from the market cap I arrive at on account of the DCF evaluation.

WBD DCF mannequin (Rasoli Analysis: In search of Alpha Financials)

The assumptions I made above are extraordinarily conservative but give WBD an intrinsic share worth of $21.33 as we speak to attain a 12.5% price of return over the following 5 years. I assumed that WBD wouldn’t develop their revenues at all around the subsequent 5 years, EBITDA would solely barely enhance, and their free money move would develop solely barely over 5% in totality over that 5 yr interval. The assumptions I made with reference to their debt compensation are extraordinarily conservative as their debt compensation doesn’t exceed $4 billion in a single yr though WBD repaid over $5.2 billion in simply the previous yr alone whereas debt compensation will stay their #1 precedence over the following few years. When altering the low cost price on the mannequin till the intrinsic share worth is identical as the present share worth which might replicate the anticipated price of return if the inventory is purchased at as we speak’s stage over the following 5 years, we discover {that a} 27.5% return from as we speak’s costs could be anticipated.

WBD DCF Mannequin (Rasoli Analysis: In search of Alpha Financials)

General, even underneath such extraordinarily conservative assumptions WBD has an intrinsic share worth of $21.33 as we speak to attain a 12.5% compounded return for the following 5 years or a 27.5% compounded return at as we speak’s share worth.

Threat Elements:

Though WBD seems considerably undervalued, there are vital dangers that might jeopardize the funding thesis.

Declining Networks:

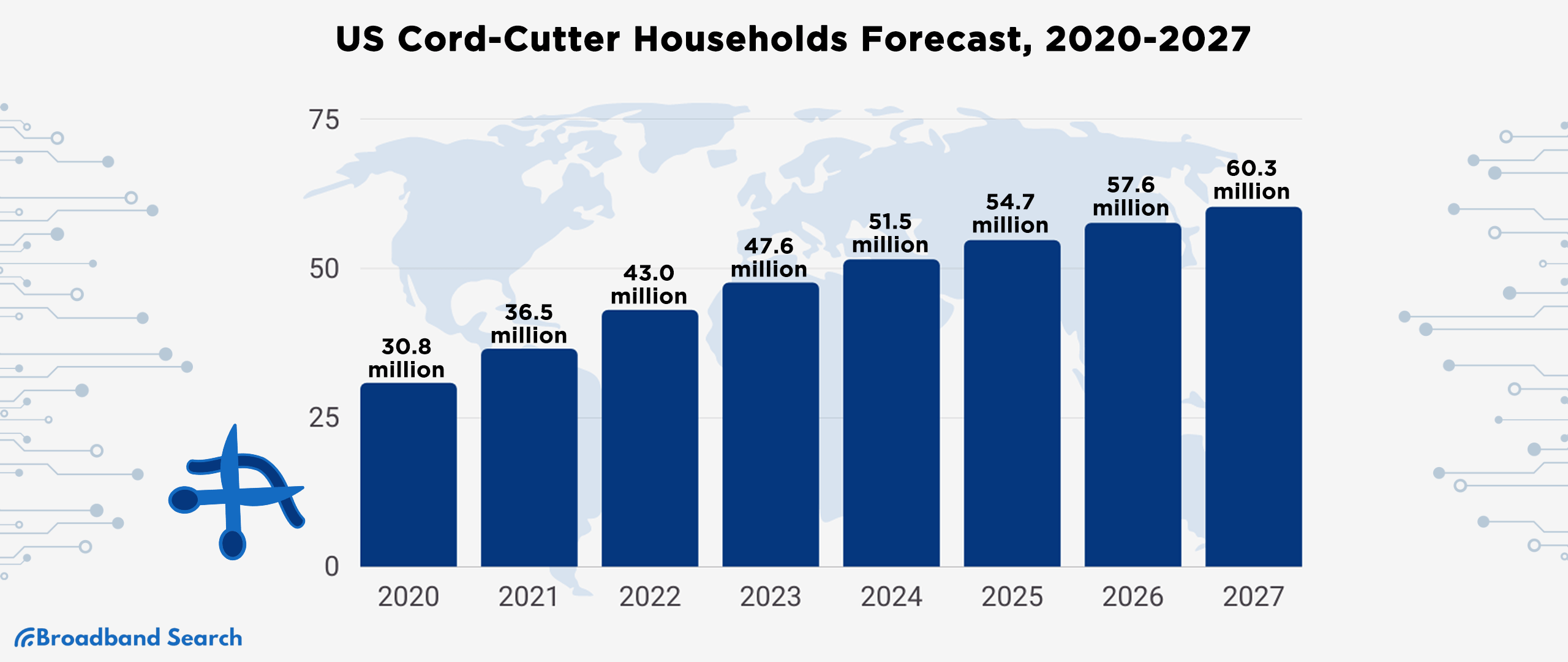

Prior to now quarter for WBD, their networks phase introduced in $2.2 billion in adjusted EBITDA relative to $2.5 billion in adjusted EBITDA introduced in by the enterprise as an entire. Basically, with over 91% of WBD EBITDA coming from their networks phase, a considerable danger is current if their networks proceed to say no at a quicker than anticipated tempo. Though WBD’s DTC phase, Max, ought to be capable to offset a few of the declines within the networks phase that can inevitably occur, it’s potential that it doesn’t offset nearly all of the declines within the networks phase resulting in a gradual decline within the profitability of the enterprise.

Wire Reducing Projections (BroadBand Search)

Macroeconomic dangers:

The danger of a recession for WBD is substantial because of them promoting primarily discretionary merchandise that are the primary merchandise that buyers pull again on throughout a recession. A decline in profitability throughout a recession can poise main dangers as WBD could also be unable to payoff their debt main them to refinance at excessive charges thereby considerably elevating their curiosity bills and additional damaging their profitability.

Remaining Ideas:

Warner Bros. Discovery seems tremendously undervalued as a result of giant quantities of free money move they can produce in addition to the speedy tempo at which they will pay down their debt. In tandem, these components place the corporate to ship substantial returns within the following years regardless of main dangers of their networks phase and main competitors throughout the business. Though the looming danger of a recession can jeopardize WBD means to provide free money move and pay down their debt, the quite a few manufacturers the corporate owns and a few of the strongest IP throughout the media & leisure business place WBD to beat such challenges which will happen.