Alexandr Lebedko

Introduction and thesis

WD-40 Firm (NASDAQ:WDFC) is a worldwide shopper merchandise firm identified for its iconic WD-40 Multi-Use Product, in addition to a variety of family upkeep and cleansing merchandise. The corporate was based in 1953 and is headquartered in San Diego, California.

WD-40 is a improbable enterprise that’s managed impeccably. Its unequalled model is utilized to its most to generate main margins, with out underinvestment in R&D. Merchandise launched beneath its “WD-40 Specialist” section are outgrowing the broader enterprise and are primed to have a bigger influence on the top-line going ahead.

Alongside this, its broader technique of optimizing business (exploiting premiumization and e-commerce) and operational (techniques and provider relationships) worth ought to enable for margin appreciation within the coming years.

We see restricted components that may cease this enterprise from persevering with to compound within the coming years.

Regardless of this, we fee the inventory a maintain. Administration is presently working towards what we imagine to be optimistic targets, creating important threat to its share worth as a consequence of market expectations. This has led to a valuation we can’t justify, with a NTM EBITDA a number of of 30x and a FCF yield of 1.6%. We propose traders stay affected person or search higher alternatives elsewhere.

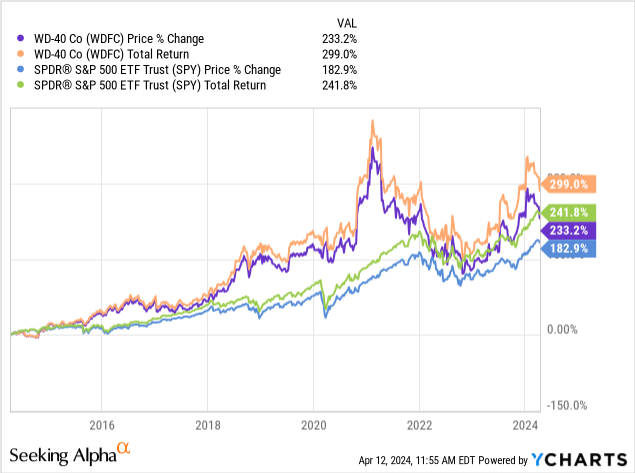

Share worth

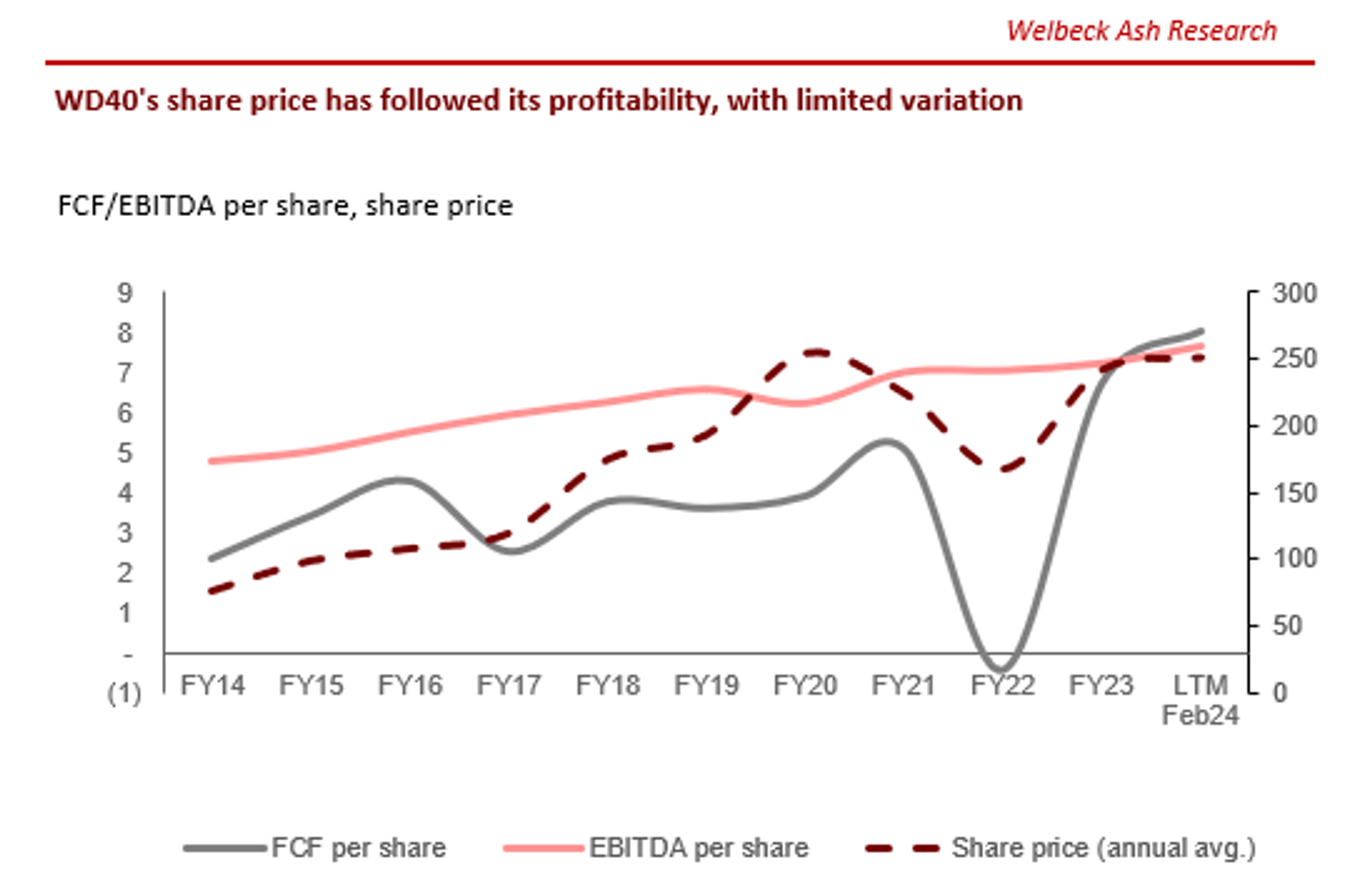

WD-40’s share worth has carried out nicely over the last decade, persistently outperforming the market. This has been delivered primarily via monetary growth and the optimization of shareholder returns.

Industrial evaluation

Capital IQ

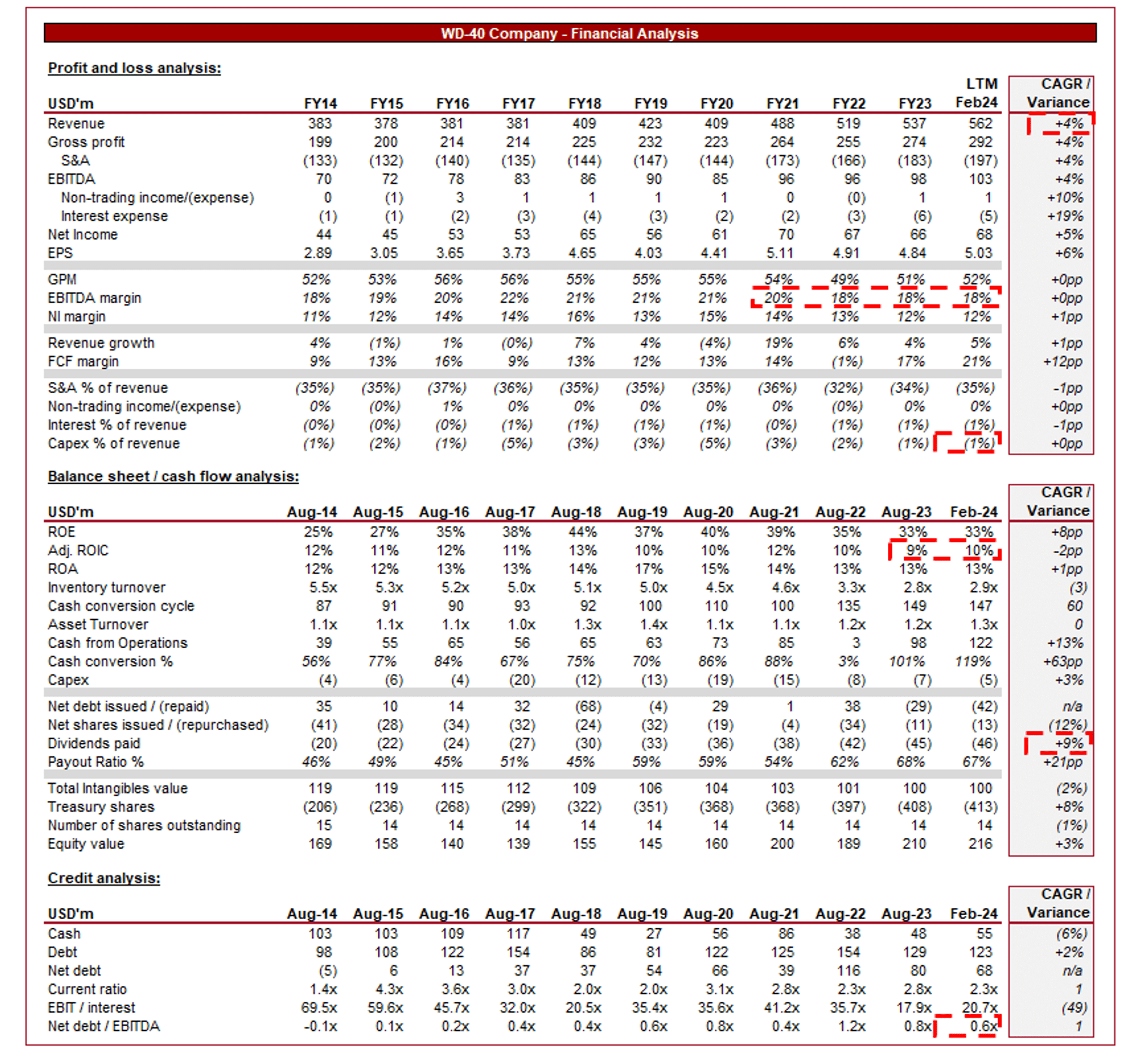

Introduced above are WD-40’s monetary outcomes.

WD-40’s income has grown modestly over the last decade (CAGR: +4%), albeit with a linearity to time of 0.9 and restricted M&A exercise, reflecting a formidable natural trajectory given the maturity of its merchandise.

Enterprise Mannequin

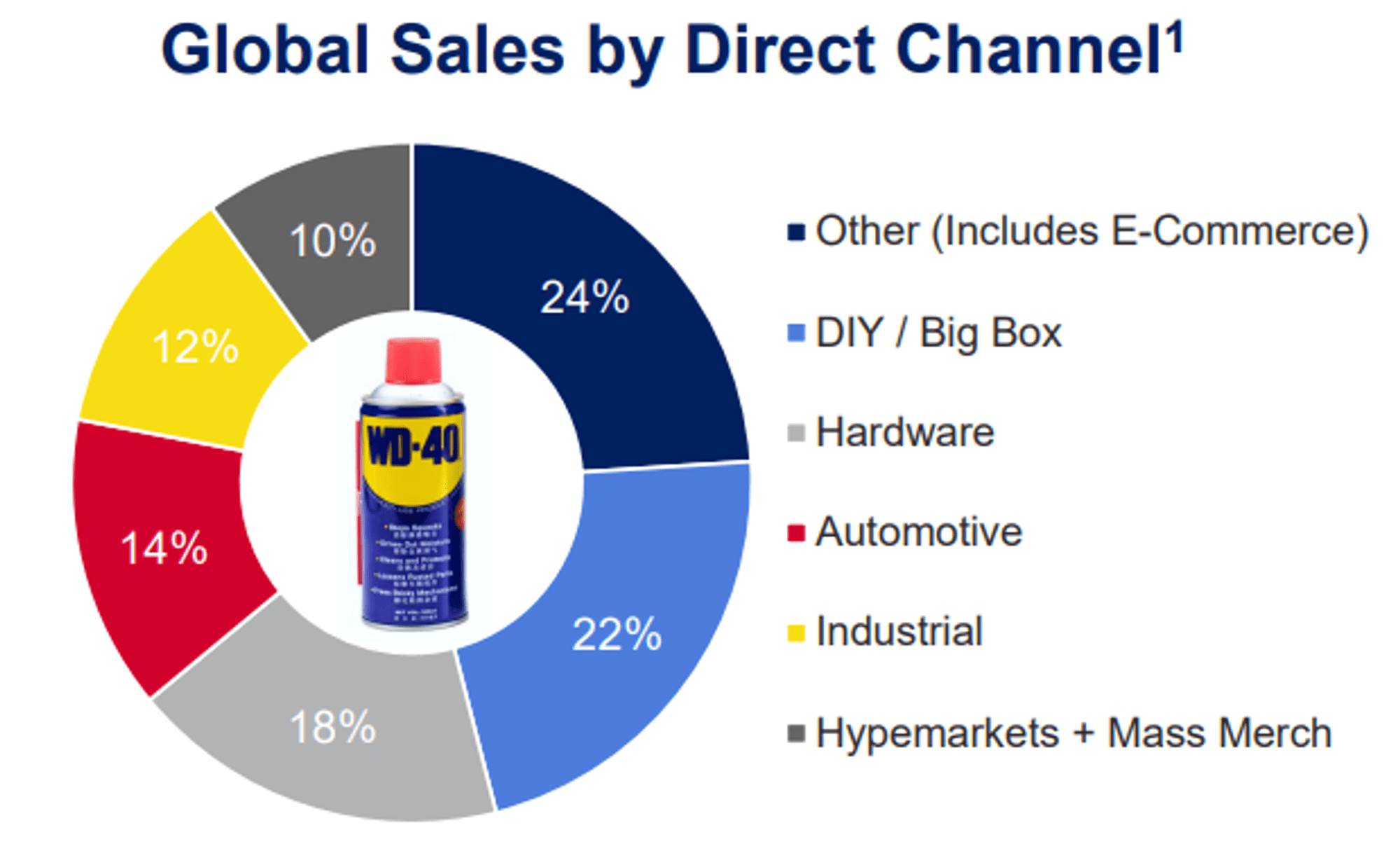

WD-40 gives a various vary of upkeep and cleansing merchandise beneath its flagship model “WD-40”, together with the unique “WD-40 Multi-Use Product” (81% of FY23 income), in addition to specialised formulations like WD-40 Specialist and WD-40 BIKE (13%). Along with its WD-40 merchandise, the corporate operates a Homecare & Cleansing section (6%). These merchandise cater to each the patron and industrial channels.

In an virtually distinctive method, the “WD-40” model is globally acknowledged. Over the a long time, the corporate has constructed an insurmountable status for reliability, effectiveness, and innovation, incomes the belief of shoppers, professionals, and companies alike. Its merchandise dominate its section, with competitors primarily within the type of lower-cost, much less efficient alternate options.

The corporate’s WD-40 upkeep merchandise present a excessive utility throughout numerous industries, permitting for persistent income development with financial growth. Its merchandise stay market-leading in high quality, while Administration strategically focuses the enterprise to seize incremental prospects, understanding it is going to have a excessive recurring gross sales fee.

Provided that WD-40’s income is basically wholly generated by the “WD-40” model, the corporate has strongly emphasised innovation and product growth to broaden the worth proposition of its merchandise. While this has incrementally supported its aggressive place, “WD-40 Specialist” solely includes 13% of income, limiting the advantages of diversification.

Diversification for WD-40 comes with its operational capabilities. The corporate has a robust worldwide presence, with operations and distribution networks spanning a number of international locations and areas worldwide. Additional, its model is highly effective sufficient that its merchandise obtain preferential stocking throughout retailers and segments. Equally to the above, nonetheless, this acts to take care of its market dominance however doesn’t essentially drive incremental development potential past financial growth.

WD-40

Aggressive Positioning

WD-40’s aggressive place relies on two key elements. Firstly, the corporate’s product, notably the “Multi-Use Product”, is genuinely comfortably forward of its friends, with its scale making certain reinvestment will defend its market place.

Secondly, the “WD-40” model has unequalled recognition and status globally, for each high quality and reliability. has sturdy model loyalty amongst shoppers and companies, resulting in sturdy recurring income.

Technique

Administration is presently delivering what it refers to as a four-by-four strategic framework, 4 must-win battles, and 4 strategic enablers.

These are damaged down as follows, with our feedback in opposition to every:

Battles to win

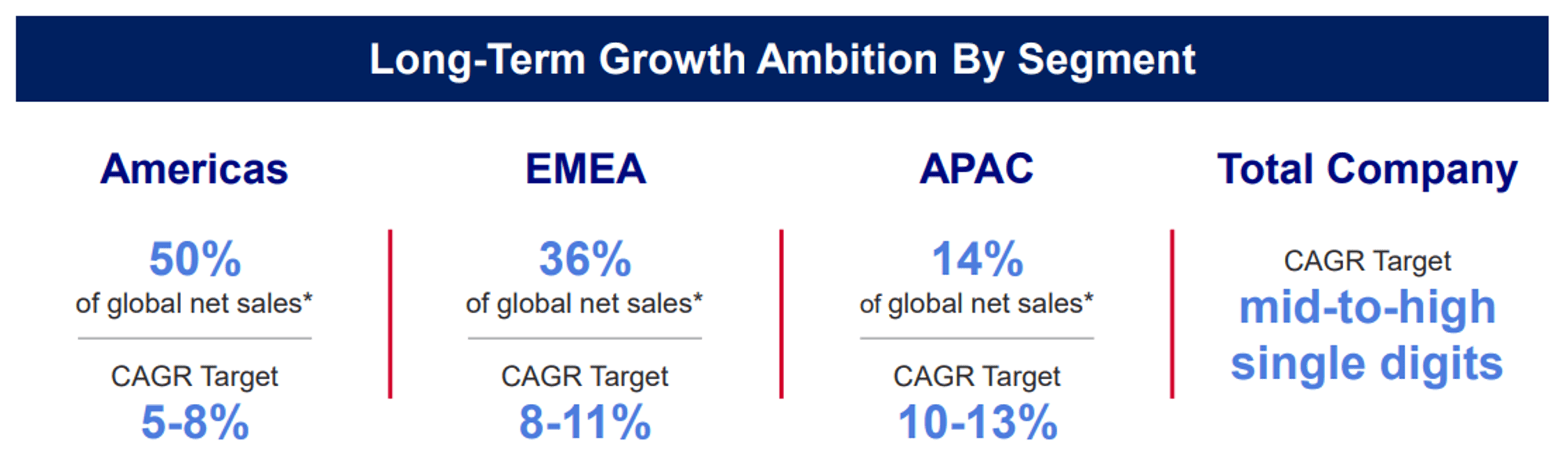

- Lead geographic growth – Administration estimates its whole worldwide development potential to be ~$1b, pushed largely by quickly growing international locations, equivalent to China, India, Bangladesh, and Saudi Arabia. WD-40 is in search of to align itself brand-wise to those markets, understanding its merchandise will naturally acquire traction in construction-heavy markets.

- Speed up premiumization – Administration is in search of to enhance the standard of its merchandise and end-user expertise, permitting for development and margin enchancment. We imagine this is a vital part of its technique, as WD-40 is slowly diversifying its merchandise, however may enhance its unit economics, additional offsetting threat. Its premiumization section has achieved a 5Y CAGR of +7.3% (concentrating on >10%).

- Drive WD-40 Specialist development – Naturally, Administration is concentrating on product growth beneath the “WD-40” model. The vary is growing nicely and we imagine it’s doubtless an underappreciated development story as a consequence of its sluggish growth (solely 13% of income). The section has grown at a CAGR of +14.2% within the final 5 years, reflecting compounding returns from historic funding. Administration is concentrating on a >15% CAGR. This mentioned, it’s price highlighting that its Homecare & Cleansing section is presently beneath strategic evaluate, saying it might search the sale of its US and UK portfolio, signaling an entire give attention to WD-40.

- Turbo-charge digital commerce – Equally to level 2, offsetting product growth threat is the scope for enhancing unit economics. The advantage of e-commerce is that WD-40 can lower out the retailer, enhancing margins.

Enablers

- Guarantee a people-first mindset – While we hate people-related strategic objectives (maximizing worth from workers ought to all the time be the case), it’s price highlighting that WD-40 has a really skilled Administration group and an worker retention fee of >89%.

- Construct a sustainable enterprise – Focusing on web zero emissions and has ambitions to be a frontrunner in its section.

- Obtain operational excellence within the provide chain – Administration is investing closely in its provide chain capabilities, apparently selecting to outsource manufacturing and distributions, but having a hands-on method that enables it to ship excellence, equivalent to <90 stock and 90%+ on-time deliveries. The enterprise basically will get asset-light advantages whereas delivering asset-heavy operational capabilities; that is improbable execution.

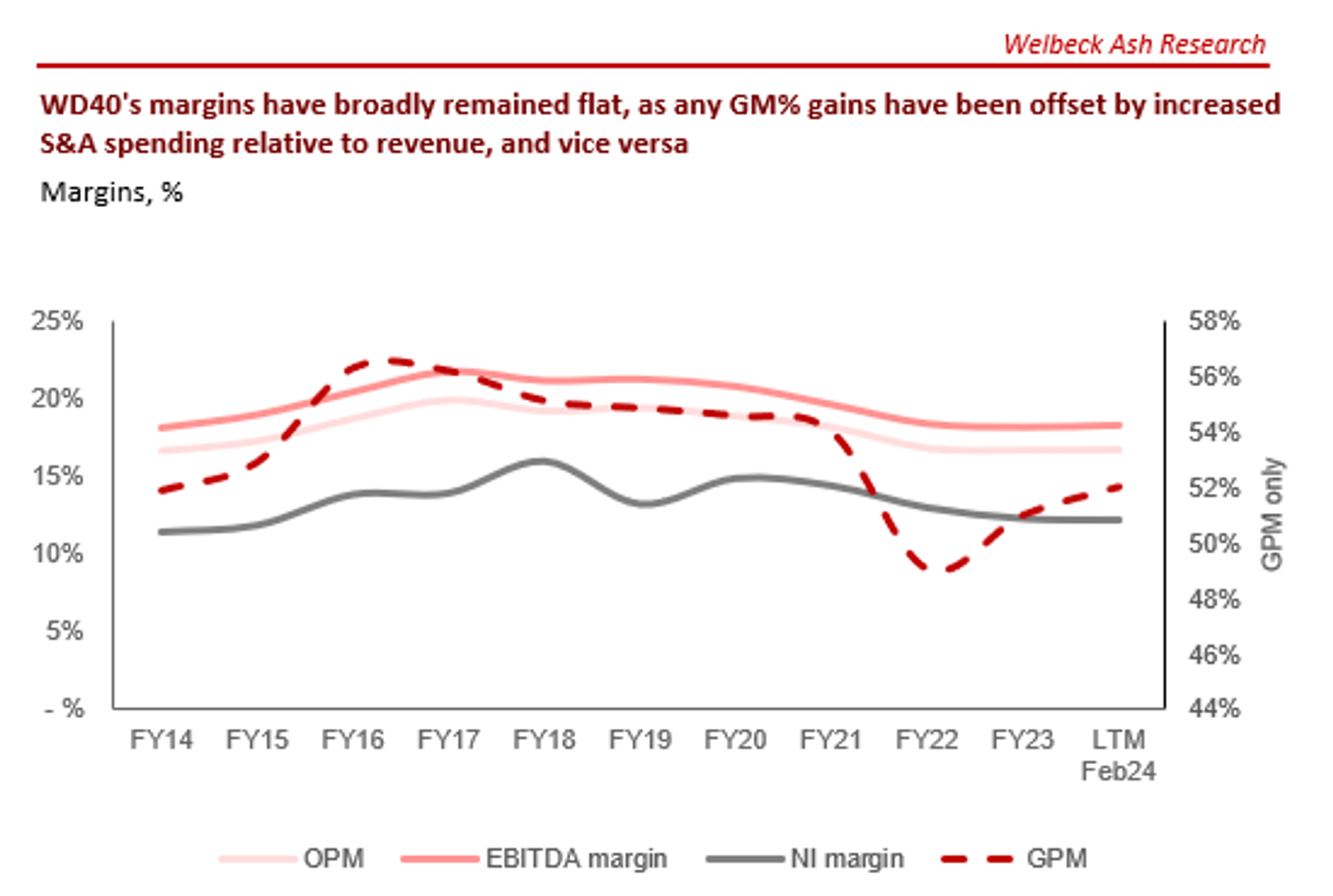

- Drive productiveness by way of techniques – Administration is in search of to modernize its techniques and capabilities, partially utilizing applied sciences, to make sure it maximizes economies of scale and worth. WD-40 has extraordinarily respectable margins, with an EBITDA-M of 19%, and has proven room for additional enchancment given its historic peaks in FY17-FY19.

While it’s clear we aren’t completely satisfied by WD-40’s enterprise mannequin, its technique and growth achieved to date are spectacular. Administration is clearly self-aware of what WD-40 is (an organization reliant on a model) and what it’s not (a diversified FMCGs enterprise). Administration is efficiently delivering incremental worth via numerous levers, minimizing the stress to create new, standout merchandise.

Financials

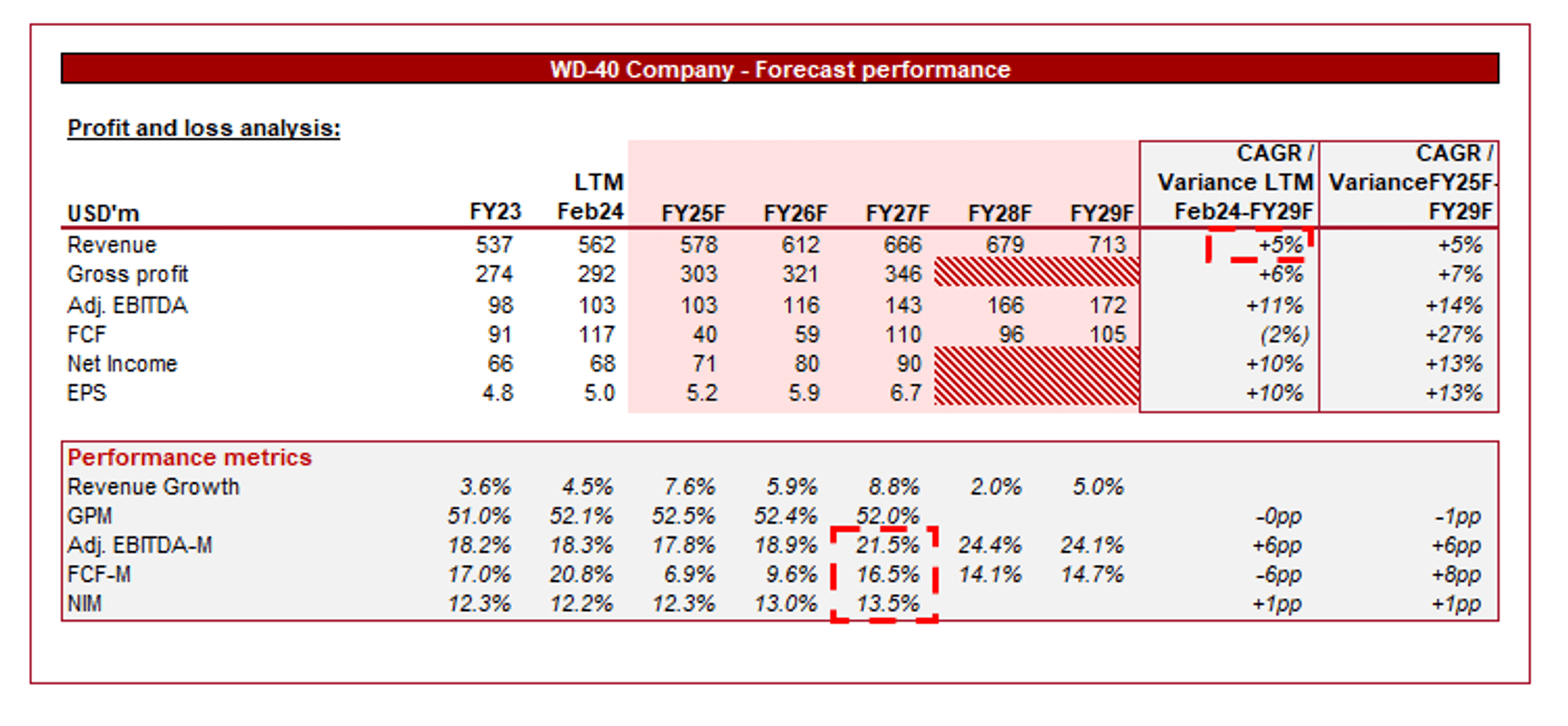

WD-40’s latest efficiency has been underwhelming. The corporate has achieved broadly constant sturdy development, with a top-line development fee of +14.6%, +7.7%, +12.4%, and +6.8% in its final 4 quarters. Nevertheless, its subject has been margin growth, which has been restricted.

WD-40 has pushed top-line development with constant worth will increase, partially as a concerted effort to extend the visibility and gross sales of its premium merchandise, benefiting from combine. Moreover, the corporate, equally to its friends, has persistently lifted costs in response to inflationary circumstances. This development has primarily come from EIMEA in Q2 (+16%), which now we have noticed (in different shopper companies) as a area seeing probably the most delays in worth will increase coming via.

Administration believes there are ~3ppts of EBITDA margin to win again, which we concur with, albeit requires extra motion given inflationary pressures are subsiding and so the scope for worth uplifts may also. Administration should exploit the arbitrage alternative to learn.

Capital IQ

Trying forward, Administration is extremely bullish. It believes a long-term development fee of mid-to-high single-digits could be delivered, pushed largely by EMEA and APAC. This can be a blended evaluation primarily based on the combo shift mentioned above, particularly towards development areas and premium merchandise.

WD-40

We take into account this pretty optimistic. The corporate’s historic development fee has been significantly under this (+4%), albeit is barely masked by the mature development fee of the “WD-40 Multi-Use Product” and the underwhelming developments of the Homecare and Cleansing section. At the same time as “WD-40 Specialist” outgrows different segments and premiumization drives the enterprise, we battle to see how the expansion fee could be lifted past ~7%.

Secondly, while we do imagine ~3ppts of EBITDA-M is capturable, restricted progress is presently being made. In a normalized financial atmosphere, WD-40 will face way more issue driving enchancment relative to present market circumstances.

We imagine development of 5-7% could be achieved, alongside margin enchancment of ~0.5-1ppt of EBITDA-M within the coming years. This displays a extra lifelike trajectory we really feel, adequately quantifying its constructive strategic developments.

Analysts are extra essential than we’re relating to development, forecasting +4%, whereas anticipating higher margin growth.

Capital IQ

Steadiness sheet & Money Flows

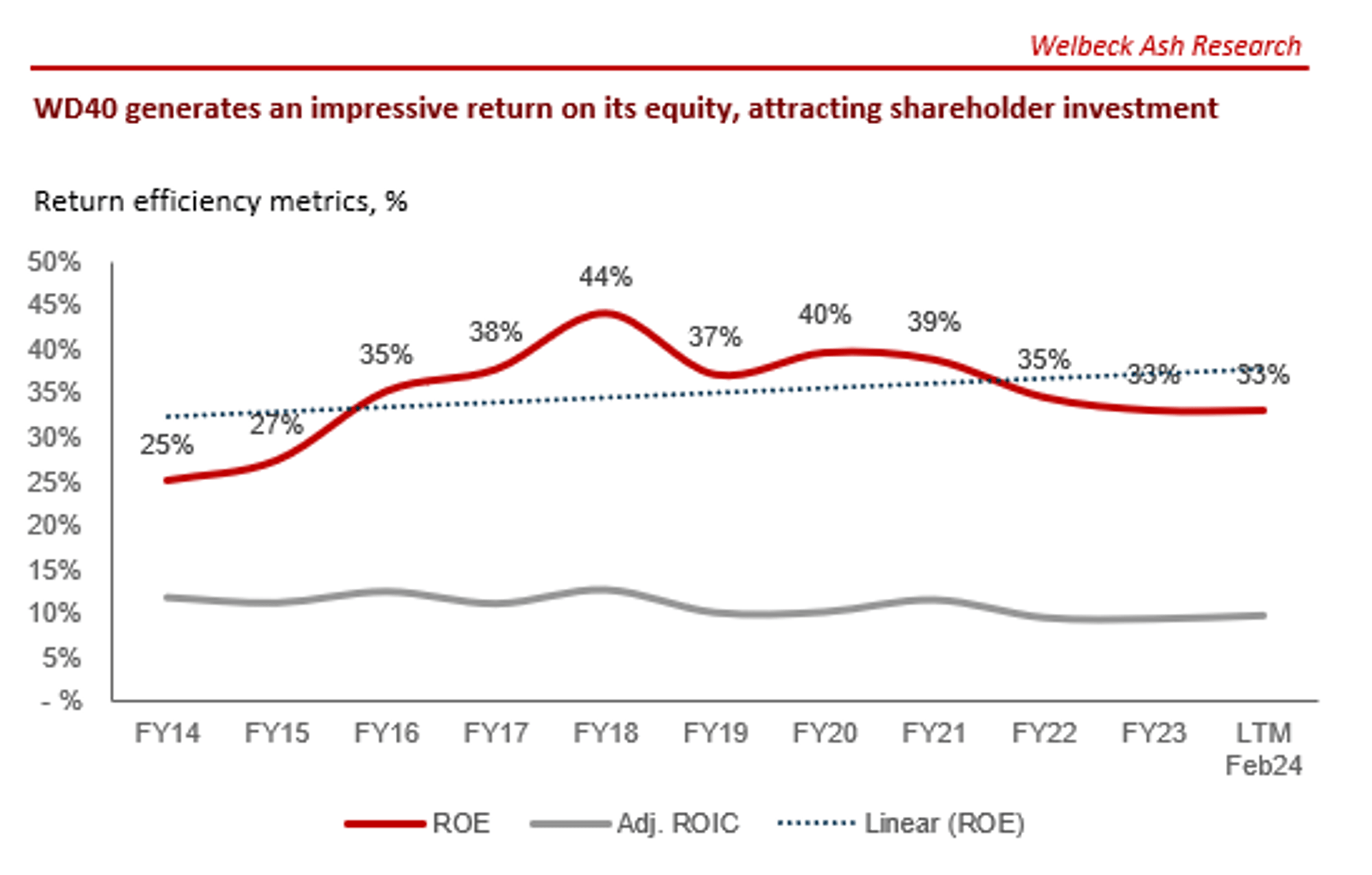

WD-40 is conservatively financed and generates spectacular FCFs, owing to its sturdy absolute margins and minimal capex commitments. This, alongside its asset-light mannequin, has allowed it to generate a formidable ROE.

Administration has supplemented these spectacular returns with distributions, with dividends rising at a CAGR of +9%, alongside periodic buybacks.

The corporate is compelling from a ROE perspective, suggesting the flexibility to generate sturdy long-term returns with incremental development.

Capital IQ

Business evaluation

Looking for Alpha

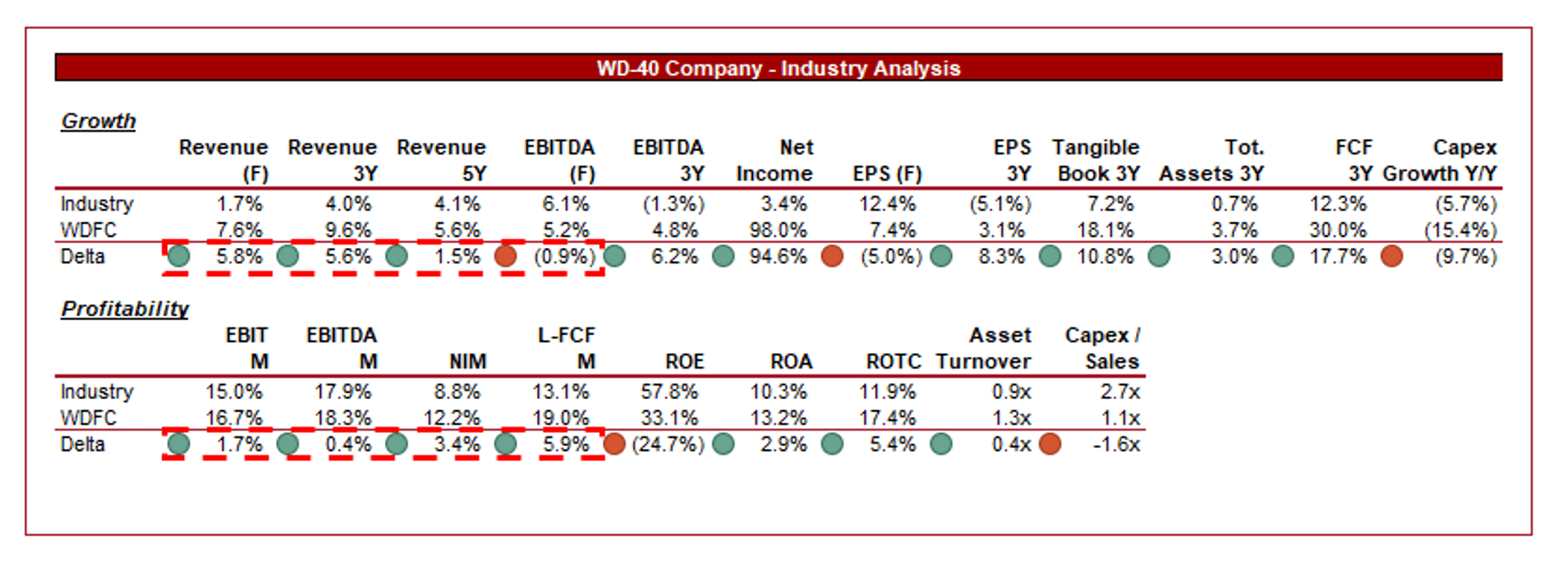

Introduced above is a comparability of WD-40’s development and profitability to the typical of its business, as outlined by Looking for Alpha (12 firms).

WD-40’s efficiency relative to its friends is spectacular, with superior development and margins. As now we have said already, what Administration has carried out with the assets at hand is extremely spectacular. The enterprise is optimized impressively nicely, with genuinely sturdy margins and development regardless of the latest fall in EBITDA-M.

This has been delivered via a mixture of its aggressive benefit and operational capabilities. We see restricted threats to this within the medium time period. Our predicted development fee of 5-7% would take the corporate comfortably above its peer group’s 5Y common.

Valuation

Capital IQ

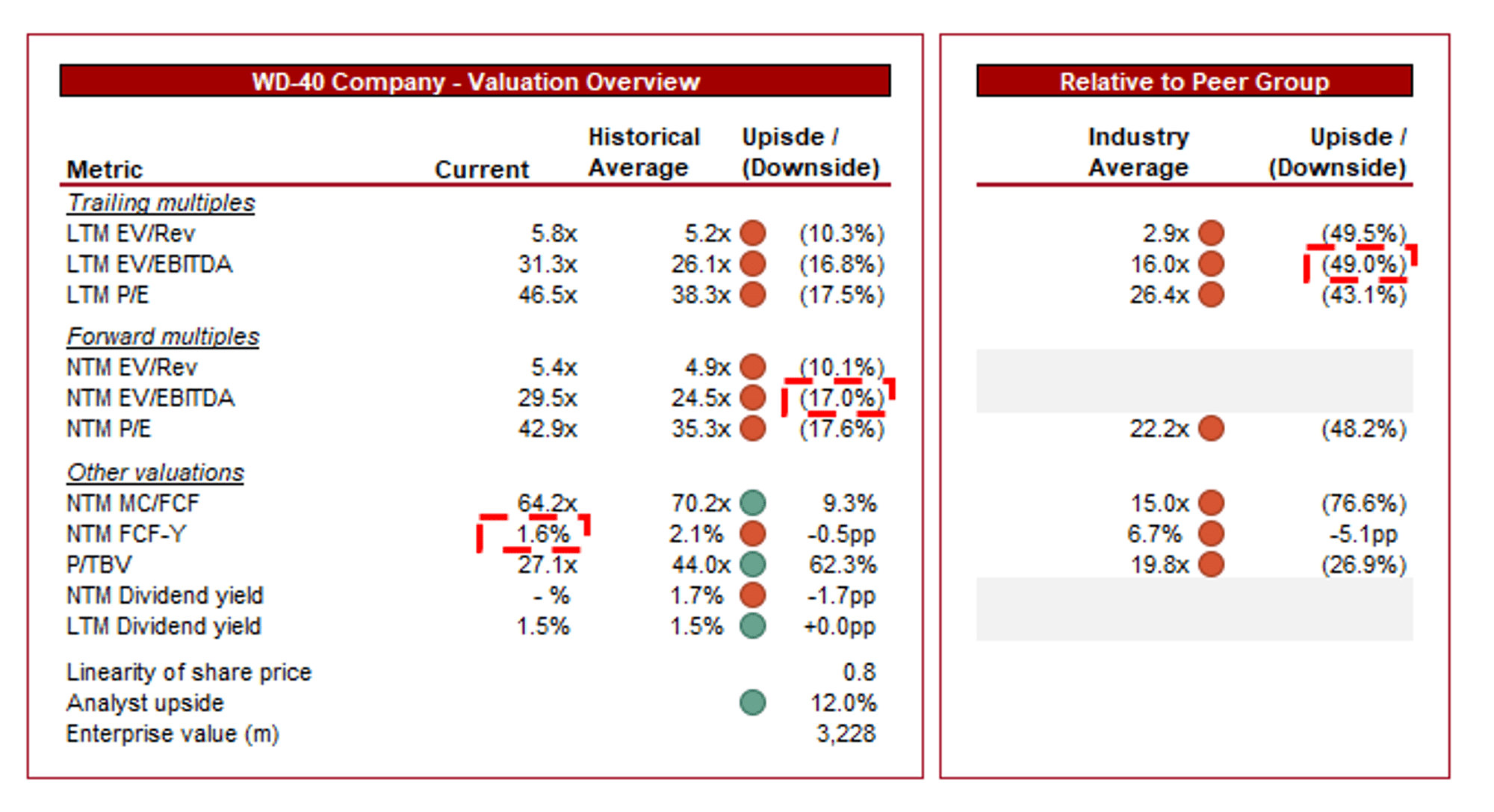

WD-40 is presently buying and selling at 31x LTM EBITDA and 30x NTM EBITDA. This can be a premium to its historic common.

A premium to its historic common isn’t simply justifiable in our view, as though sturdy growth has been achieved via progress towards its strategic aims, the corporate has additionally seen margin erosion. FCF has solely remained elevated because of the tapering of capex spending and supreme working capital administration, which can’t be anticipated to proceed. This mentioned, we might recommend a premium of ~10% could be pretty argued, implying the inventory is barely overvalued.

Additional, WD-40 is buying and selling at a substantial premium to its friends, ~48-50% on an LTM EBITDA / NTM P/E foundation. That is extremely troublesome to justify. The corporate’s ROE and FCF constructive delta clearly recommend a big premium is warranted, however we battle to see the accompanying development that may push the corporate towards worth.

Total, we imagine the inventory is probably going overvalued, with appreciable execution threat related to Administration’s present steering. With a FCF yield of 1.6%, traders are doubtless higher positioned allocating capital elsewhere.

Capital IQ

Key dangers with our thesis

Given Administration’s bullish forecasts, the upside threat is clearly the shortcoming to ship on this, whereas the draw back threat is detrimental margin development.

Closing ideas

WD-40 is a improbable enterprise. The corporate has unimaginable model worth, underpinned by real innovation and market-leading utility to customers. We see restricted dangers to this place and count on the enterprise to efficiently keep its expansionary efforts.

This mentioned, we can’t reconcile its present valuation. For a mature enterprise equivalent to this, traders want a margin for error or face an inefficient allocation of capital. At a FCF yield of 1.6%, we simply don’t see adequate upside, thus ranking the inventory a maintain.