Richard Drury

Written by Nick Ackerman, co-produced by Stanford Chemist.

Western Asset Diversified Income Fund (NYSE:WDI) continues to perform well and provide investors with a fully covered double-digit yield. The closed-end fund’s discount had narrowed materially at the beginning of 2024 but has widened back out once again. It has been a bit shallower since our previous update last December. Overall, the current discount once again puts the fund back into our ‘Buy’ discount target.

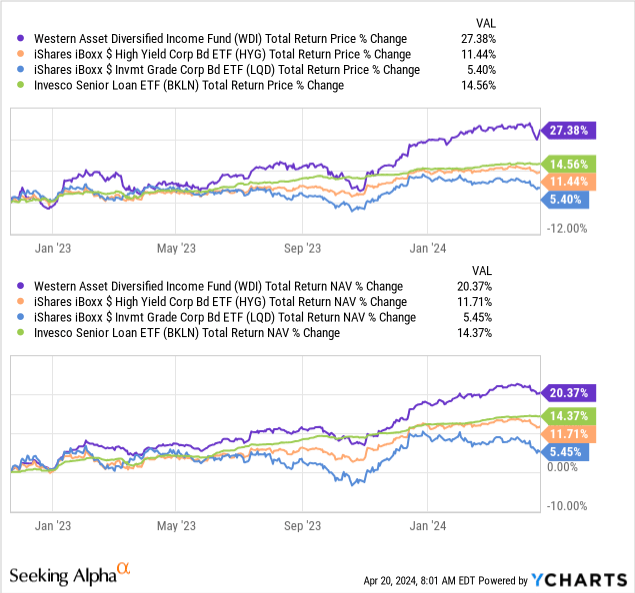

Since our last update, that narrowing discount helped to ‘boost’ the overall total returns. This has put it at a level where it was competitive with the S&P 500 Index. Of course, that’s not an appropriate benchmark for a multi-sector fixed-income fund, but it can give us a glimpse into how equities were performing during this period.

WDI Performance Since Prior Update (Seeking Alpha)

WDI Basics

- 1-Year Z-score: 0.95

- Discount: -8.13%

- Distribution Yield: 12.09%

- Expense Ratio: 1.73%

- Leverage: 31.30%

- Managed Assets: $1.18 billion

- Structure: Term (anticipated liquidation date, June 24, 2033)

WDI’s objective is “to seek high current income. As a secondary investment objective, the fund will seek capital appreciation.” They will bring a “flexible and dynamic” approach. They anticipate doing this by rotating sectors and securities in response to market conditions, focusing on what we believe are undervalued securities with attractive fundamentals.

Performance – Discount Nearing Opportunity Once Again

I have been invested in WDI for quite a while and have been following it for a bit longer than that. Overall, WDI could still be considered a newer fund, at least relatively speaking, as it was incepted in mid-2021. That was probably one of the worst times to launch a leveraged fixed-income fund as it fell precipitously into 2022 as the Fed raised rates aggressively.

Since I originally went more bullish on the fund in the middle of 2022, the performance has been quite strong. In fact, if we refer to that article’s performance breakdown from Seeking Alpha, the fund once again shows a total return that is competitive against the S&P 500 Index.

WDI Performance Since ‘Buy’ Rated Article (Seeking Alpha)

Ultimately, the goal of a multi-sector bond CEF is not to compete against an equity index but to provide a steady income stream to investors.

For full transparency, I didn’t end up taking a position until November 21, 2022. So when I see it mentioned, “just look at a chart,” when inferring how terrible an investment WDI has been since its launch, well, that really has no bearing. My chart looks a little different…

YCharts

If we flip back to standardized periods of performance against the fund’s benchmark—in its relatively short history—we have a mixed picture.

WDI Annualized Performance Vs. Benchmark (Western Asset)

Of course, 2022 saw a significantly sharper drop in the market price as the fund went to a deep discount. That’s often the case with new CEFs, as they IPO and then plunge to a 10% discount. This is even true for CEF 2.0s despite coming with a term structure (in which the terms can generally be extended by the Board or even eventually switched to perpetual with some action from the shareholders).

From there, the total NAV returns were also lower relative to their benchmark because that’s the leverage at play.

Leverage does work both ways, though, and that’s why the 2023 rebound was also where the fund could gain some significant ground over its benchmark.

In implementing a portfolio with CEFs, we utilize the discount/premium mechanic in their structure to help exploit further potential opportunities. That can lead to possibly better overall total returns as well.

Our target ‘Buy’ for WDI is at an 8% discount level. I’ve held it all the way through, even when the discount narrowed materially in January of this year; I’m generally more of a buy-and-hold and don’t always exploit these opportunities as efficiently. I tend to wait for even further outsized moves before being prodded to take action. As an example, if WDI moved to a 5 to 10% premium, then I’d certainly consider selling out of my position and moving the cash elsewhere.

With that said, WDI once again highlights the opportunities that investors have as we are once again pushing just over that 8% level and retreating from that narrower discount level early in the year.

Distribution – Fully Covered

Being a leveraged fund, they have suffered the same significant headwinds of the higher rate environment, causing interest expenses to rocket higher. The fund’s total expense ratio has been pushed up to 4.79% – with a fund that already carries a heftier expense ratio of ~1.70% operating expenses.

The weighted average interest rate on their loan climbed from 1.13% when the fund launched to 2.71% at the end of 2022. The end of 2023 has now pushed the interest rate on their loan to an average of 6.11%. This is in line with other CEFs utilizing a leverage facility.

Fortunately, investors in WDI hold a significant allocation to floating rate-based investments. The fund has also been hedging interest rate sensitivity with futures contracts to help manage the duration. The effective duration for the fund was listed at 4.62 years.

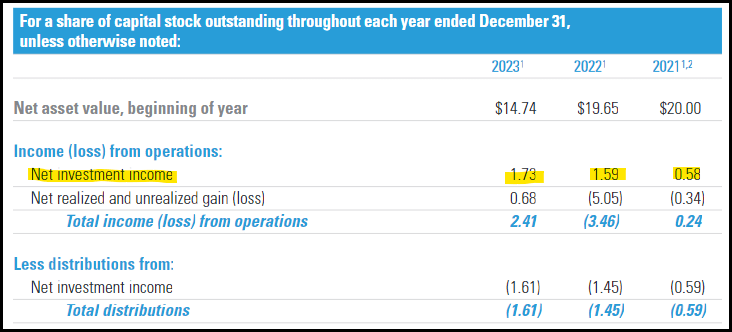

What this means is that the fund’s borrowings experience this lift from a much higher Fed target rate, and so do the underlying investments. That’s why the fund’s net investment income has also increased materially.

WDI NII (Western Asset (highlights from author))

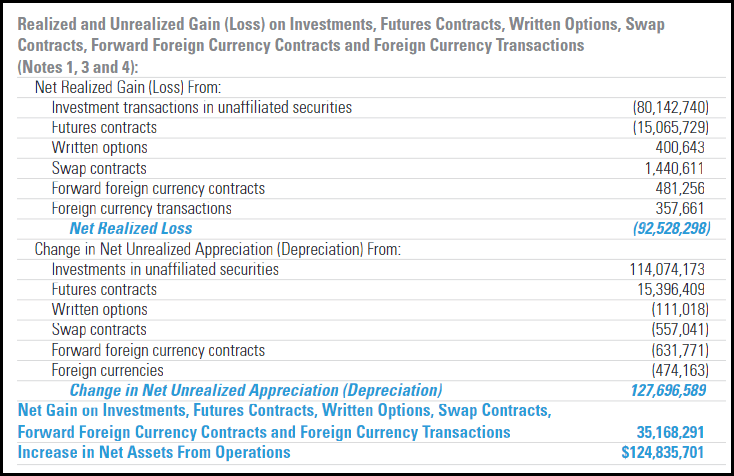

For their derivatives, they saw realized gains in their written options and swap contracts. However, they realized sizeable losses in their futures contracts. Those realized losses were more than offset by their unrealized gains from the futures contracts, though.

WDI Realized/Unrealized Gains/Losses (Western Asset)

They also realized sizeable losses in their underlying investment portfolio, but again, here, the unrealized gains more than made up for those losses. In the end, for 2023, the fund saw a sizeable lift in net assets.

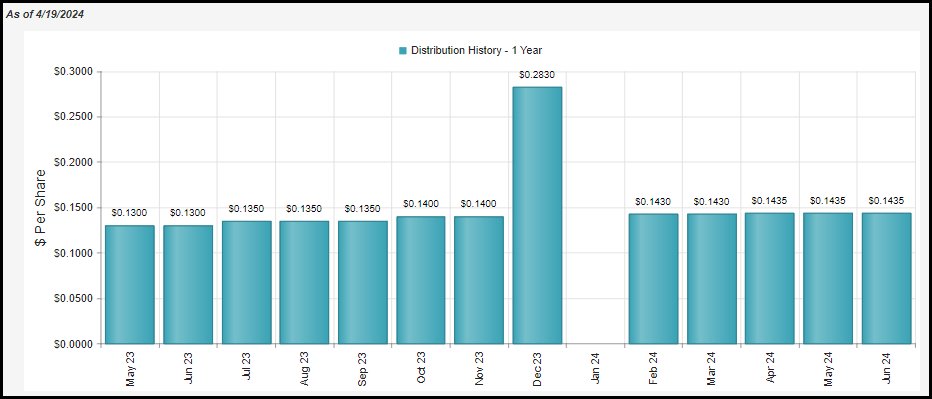

A rising NII has translated into a higher monthly distribution for investors as well. The latest quarterly announcement also once again saw an increase—albeit a small increase.

WDI 1 Year Distribution History (CEFConnect)

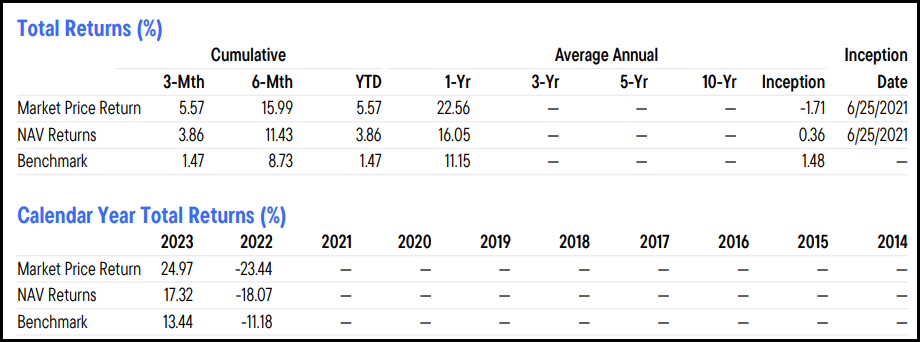

Based on the current monthly distribution, we arrive at a yield of 12.09%. On an NAV basis, this works out to 11.10%. Perhaps more importantly, though, is that the fund’s distribution is fully covered by NII. The current annualized rate comes to $1.722, which works out to just a touch over 100% coverage based on the 2023 NII per share.

Our previous article highlighted this coverage, too, when we took a look at the fund’s quarterly results for the period that ended in September. At that time, NII per share came to $0.44, which suggests that NII is currently running higher than at the annual rate seen in 2023.

The caveat to all of this, though, is that coverage is strong, but not by a wide margin. That means that with the expected rate cuts from the Fed in the next year or two, coverage is highly anticipated to sink below 100%. Whether they decide to adjust the distribution lower when that happens will ultimately be up to the managers and Board, if they want to go from an all income-based distribution currently to an income/potential capital gain or possibly NAV erosion distribution.

This isn’t the only fund that has this to consider, as all floating-rate-based funds will be faced with the same dilemma. With some flexibility for the WDI managers due to WDI being a multi-sector fixed-income fund, they might have some more wiggle room to start locking in fixed-rate debt instruments closer to the anticipated rate-cutting cycle.

For tax purposes, as is the case for most interest-based receiving CEFs, expect mostly ordinary income classifications. WDI has classified every distribution in 2021, 2022, and 2023, all as ordinary dividends.

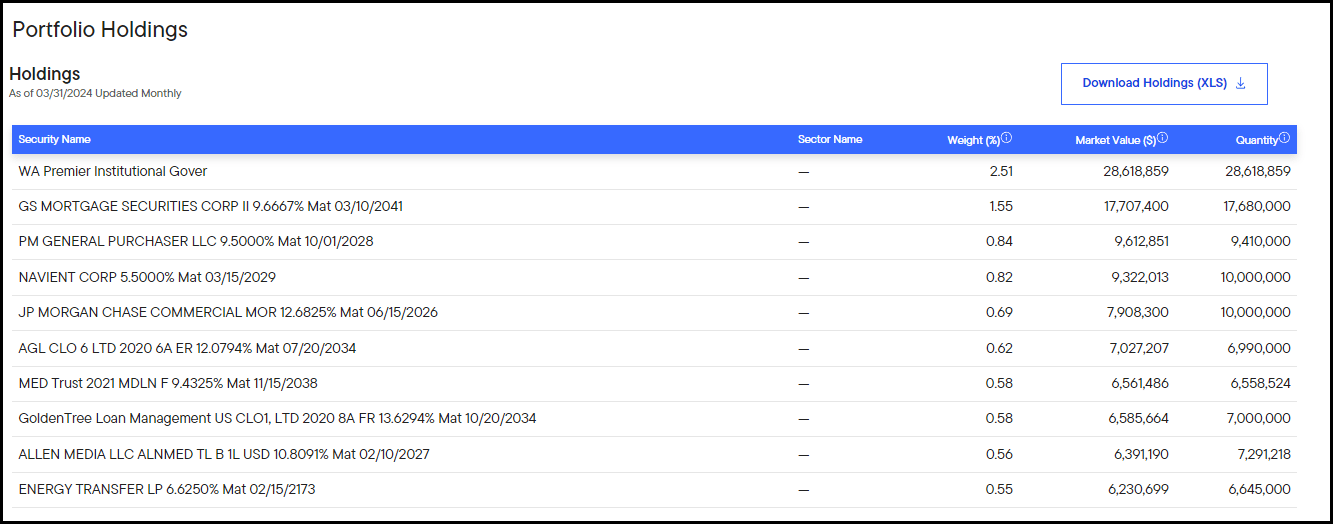

WDI’s Portfolio

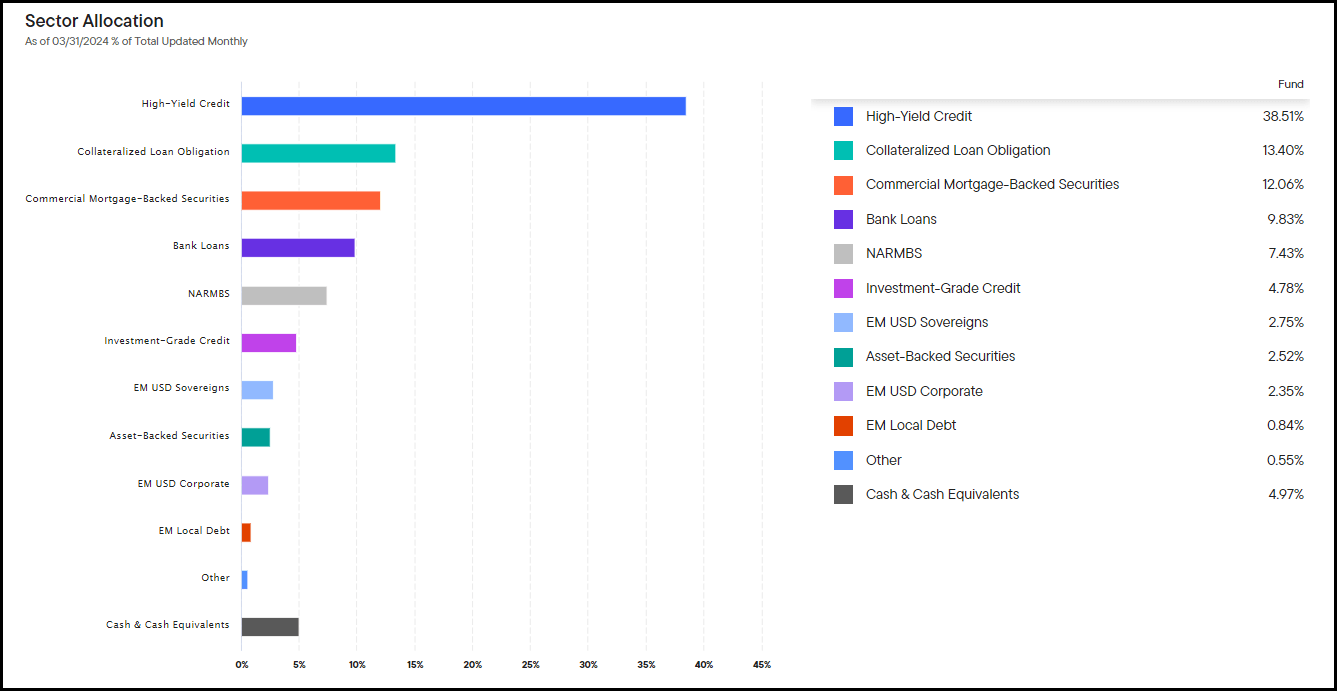

Speaking of floating versus fixed, here is a look at the fund’s latest breakdown in their portfolio by sector.

WDI Sector Allocation (Western Asset)

The largest weighting here is to the high-yield credit sleeve, which it was previously. This is going to be the fixed-rate bond sleeve of the portfolio. Following that up, we have the collateralized loan obligation or CLO sleeve, commercial MBS, and bank loans, which are going to be overwhelmingly floating rate categories from which they’ve benefited in the now higher rate environment.

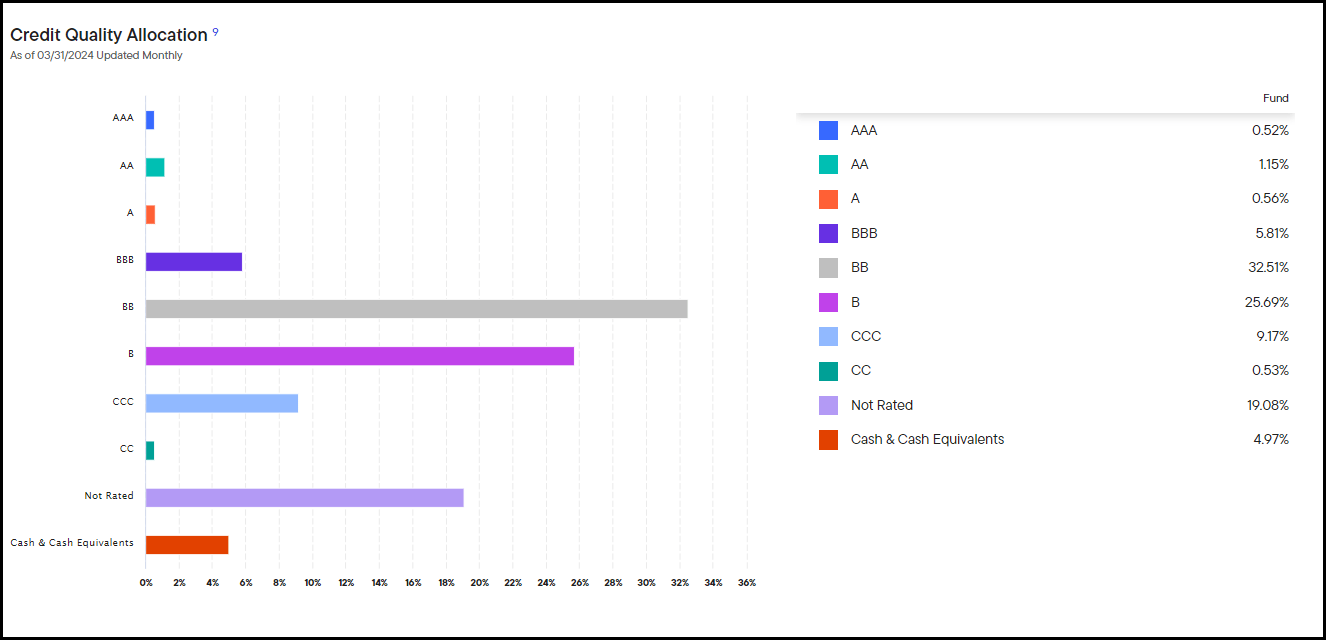

Given the weightings above, it isn’t too surprising to see that most of the portfolio is below-investment-grade.

WDI Portfolio Credit Quality (Western Asset)

Overall, since our last update, the fund has not seen a significant change in any of its allocations for sectors or credit quality.

When looking at the top holdings, the fund’s allocations to each individual position are quite small. The largest weighting is actually to a money-market fund they have cash sitting in. With 335 holdings, that isn’t too surprising and is consistent with the strategy of “junk” CEFs that just invest in hundreds of positions.

WDI Top Ten Holdings (Western Asset)

When you consider that the MBS and CLO securities are pooled investments tied to hundreds or thousands of underlying mortgages and loans, the fund has even more diversification.

This ultimately means that the fund’s performance will not be driven by any handful of holdings, but by the overall economy’s performance and how well that is holding up.

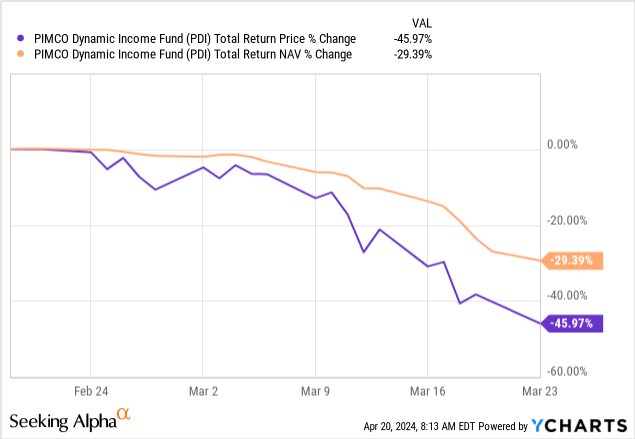

Defaults have been ticking higher and are expected to continue to do so, meaning that’s another general risk to consider before investing in any lower-rated debt currently. I highlighted my performance since buying; being a leveraged fund, I know it is always under threat of those gains being wiped out in an instant. Any black swan event could erase a third or more of the fund in a month or less.

We don’t really have to look that far to see an example of that, either. Here is what the PIMCO Dynamic Income Fund (PDI) experienced from the peak of February 19 to the trough of the March 23, 2020 Covid crash.

YCharts

If one bought during that time, they’ve seen some spectacular total returns. However, it’s just a good reminder of what leveraged funds can and will eventually go through. I felt it was a good time for a reminder, as geopolitical risks have been on the rise lately.

Conclusion

WDI continues to perform well after the rocky launch that put it in front of an aggressive rate-hiking cycle from the Fed, which saw both short and long yields rise meaningfully. However, that same event also enabled the fund to increase its distribution many times based on higher income generation in its underlying portfolio.

The fund has fallen back into our ‘Buy’ zone based on its discount moving wider than 8%. More tactical investors probably took the opportunity to divest their position in early January 2024, which means those investors may want to put WDI back on their watch list.