UPCOMING

EVENTS:

- Monday: US/Canada Holiday, China Caixin Manufacturing

PMI, Swiss Manufacturing PMI. - Tuesday: Swiss CPI, Swiss Q2 GDP, Canada Manufacturing

PMI, US ISM Manufacturing PMI. - Wednesday: Australia Q2 GDP, China Caixin Services PMI,

Eurozone PPI, BoC Policy Decision, US Job Openings, Fed Beige Book. - Thursday: Japan Average Cash Earnings, Swiss Unemployment

Rate, Eurozone Retail Sales, US ADP, US Jobless Claims, Canada Services

PMI, US ISM Services PMI. - Friday: Canada Labour Market report, US NFP.

Tuesday

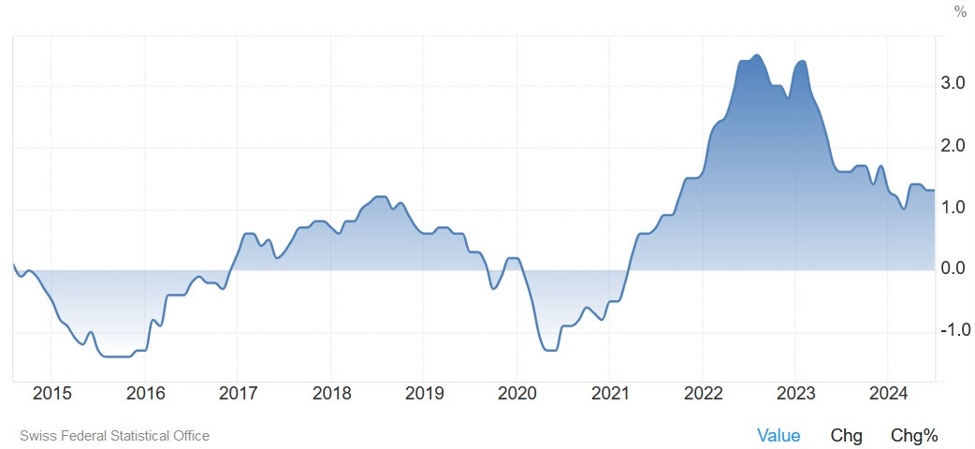

The Switzerland

CPI Y/Y is expected at 1.2% vs. 1.3% prior, while the M/M measure is seen at

0.1% vs. -0.2% prior. The market is expecting the SNB to deliver 52 bps of

easing by year end with a 67% probability of a 25 bps cut at the September

meeting (the remaining 33% is for a 50 bps cut).

SNB’s Jordan last week didn’t sound happy about the strong

appreciation in the Swiss Franc, so we might either see a 50 bps cut in

September or some intervention from the central bank to calm things down a bit.

Swiss CPI YoY

The US ISM

Manufacturing PMI is expected at 47.8 vs. 46.8 prior. As a reminder, the last month the ISM release was the catalyst that triggered a

huge selloff in risk assets as we got the “growth scare”.

The main

culprit might have been the employment sub-index falling to a new 4-year

low ahead of the NFP report which eventually triggered another wave of selling

as it came out weaker than expected across the board.

Later on, lots of

data in August showed that the weak data in July might have been negatively

affected by Hurricane Beryl, so that’s something that the market will look

at for confirmation.

The S&P Global Manufacturing PMI released two weeks ago wasn’t exactly comforting

though. The index saw the second consecutive contraction and the commentary

was pretty bleak.

The agency said “this

soft-landing scenario looks less convincing when you scratch beneath the

surface of the headline numbers. Growth has become increasingly dependent on

the service sector as manufacturing, which often leads the economic cycle, has

fallen into decline.”

“The manufacturing

sector’s forward-looking orders-to-inventory ratio has fallen to one of the

lowest levels since the global financial crisis. Employment fell in August,

dropping for the first time in three months”,

US ISM Manufacturing PMI

Wednesday

The BoC is

expected to cut rates by 25 bps bringing the policy rate to 4.25%. The recent CPI report showed some more easing in the underlying inflation

measures and the labour market data was pretty soft.

Overall, it

doesn’t look like the central bank will go for a 50 bps cut but it cannot be

completely ruled out. Including the September cut, the market expects a total

of 75 bps of easing by year end.

BoC

The US Job

Openings is expected at 8.100M vs. 8.184M prior. The last report saw a slight increase but the strong downtrend that

started in 2022 remains firmly in place. The quit, hiring and layoff rates

remain low as the labour market has been softening via less hiring rather than

more layoffs.

US Job Openings

Thursday

The Japanese

Average Cash Earnings Y/Y is expected at 3.1% vs. 4.5% prior. As a reminder,

the economic indicators the BoJ is focused on include wages, inflation,

services prices and GDP gap.

Moreover, Governor

Ueda kept the door open for rate hikes as he said that the recent market moves

wouldn’t change their stance if the price outlook was to be achieved and added

that Japan’s short-term interest rate was still very low, so if the economy were

to be in good shape, BoJ would move rates up to levels deemed neutral to the

economy.

Japan Average Cash Earnings YoY

The US Jobless

Claims continues to be one of the most important releases to follow every week

as it’s a timelier indicator on the state of the labour market.

Initial Claims

remain inside the 200K-260K range created since 2022, while Continuing Claims

have been on a sustained rise showing that layoffs are not accelerating and

remain at low levels while hiring is more subdued.

This week Initial

Claims are expected at 230K vs. 231K prior, while Continuing Claims are seen at

1865K vs. 1868K prior.

US Jobless Claims

The US ISM

Services PMI is expected at 51.1 vs. 51.4 prior. This survey hasn’t been giving

any clear signal lately as it’s just been ranging since 2022, and it’s been

pretty unreliable. The market might focus just on the employment sub-index

ahead of the US NFP report the following day.

The recent S&P Global Services PMI showed another uptick in the services sector as

growth in Q3 diverged again between Manufacturing and Services.

US ISM Services PMI

Friday

The Canadian

Labour Market report is expected to show 25.0K jobs added in August vs. -2.8K

in July and the Unemployment Rate to increase to 6.5% vs. 6.4% prior. It’s

unlikely that the market will care much about this report since we get the US

NFP released at the same time.

Canada Unemployment Rate

The US NFP is

expected to show 165K jobs added in August vs. 114K in July and the

Unemployment Rate to tick lower to 4.2% vs. 4.3% prior. The Average Hourly

Earnings Y/Y is expected at 3.7% vs. 3.6% prior, while the M/M figures is seen

at 0.3% vs. 0.2% prior.

The last month, the US labour market report came out weaker than

expected across the board and triggered another wave of selling in risk assets that

started with the ISM Manufacturing PMI the day earlier.

There’s been

lots of talk about the possible culprit for the weaker figures and it seems

like Hurricane Beryl affected the data.

The BLS said

Hurricane Beryl, which slammed Texas during the survey week of the July

employment report, had “no discernible effect” on the data.

The household

survey, however, showed 436,000 people reported that they could not report to

work because of bad weather last month, the highest on record for July. There

were 249,000 people on temporary layoff last month.

In fact, the

majority of the increase in the unemployment rate has been due to people on

temporary layoff. The market will want to see if July’s data was indeed

negatively affected by temporary factors.

As a reminder, the

Fed is very focused on the labour market now and this report will decide

whether they will cut by 25 bps or 50 bps at the upcoming meeting.

US Unemployment Rate