UPCOMING EVENTS:

- Tuesday: Japan

PPI, UK Labour Market report, US NFIB Small Enterprise Optimism Index, US

CPI. - Wednesday: UK GDP,

UK Industrial Manufacturing, Eurozone Industrial Manufacturing. - Thursday: US

PPI, US Retail Gross sales, US Jobless Claims, New Zealand Manufacturing PMI. - Friday: US

Industrial Manufacturing, US College of Michigan Client Sentiment

Survey, PBoC MLF.

Tuesday

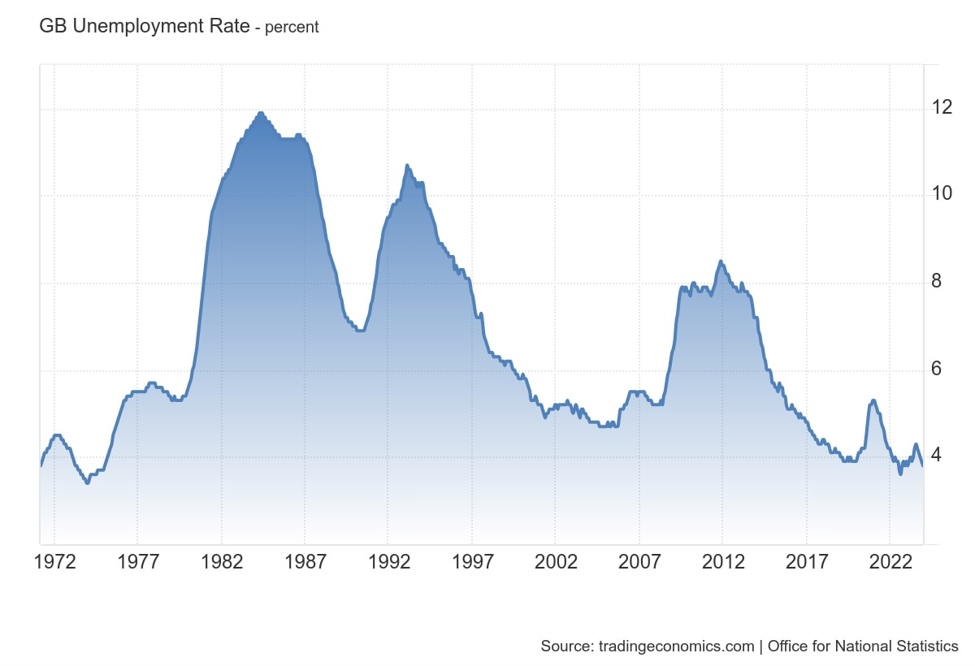

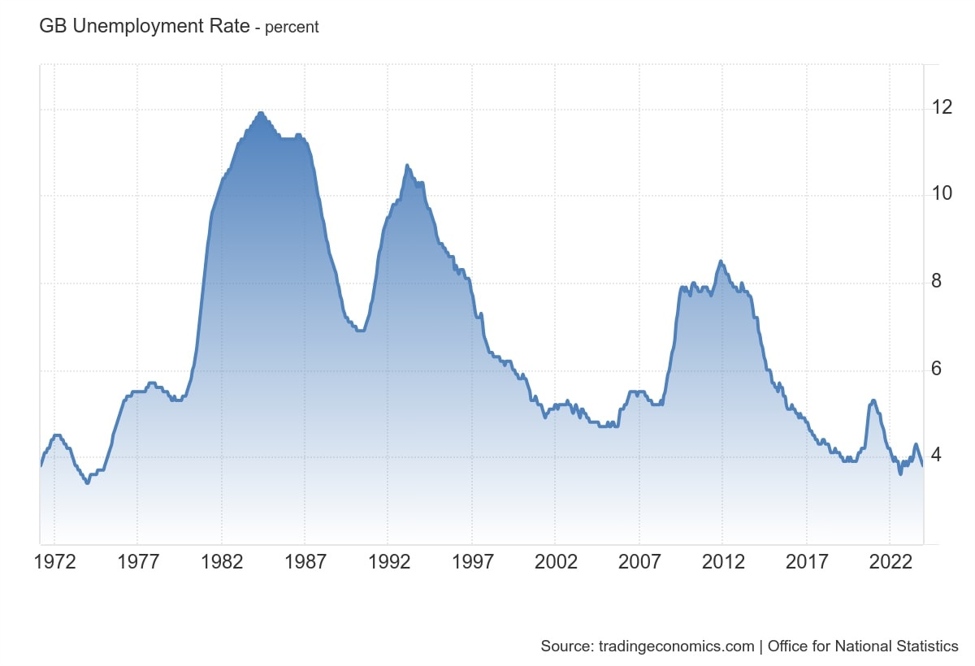

The UK Unemployment Price is anticipated to

stay unchanged at 3.8% vs. 3.8% prior.

The Common Earnings Ex-Bonus is anticipated to tick decrease to five.7% vs. 5.8% prior,

whereas the Common Earnings together with Bonus is seen at 6.2% vs. 6.2% prior. Weak

figures, particularly on the wage development half, ought to carry expectations for charge

cuts ahead, whereas robust knowledge won’t change a lot for now. The markets

count on the BoE to ship the primary charge minimize in August.

UK Unemployment Price

The US CPI Y/Y is anticipated at 3.1% vs.

3.1% prior,

whereas the M/M measure is seen at 0.4% vs. 0.3% prior. The Core CPI Y/Y is

anticipated at 3.7% vs. 3.9% prior, whereas the M/M determine is seen at 0.3% vs. 0.4%

prior. This report comes after a collection of weak US knowledge, particularly on the

labour market facet, so (for my part) this explicit launch is prone to be

light in case of a hawkish response to a beat. Conversely, if the information misses,

we must always see the market value again in a Could charge minimize.

US Core CPI YoY

Thursday

The US PPI Y/Y is anticipated at 1.2% vs.

0.9% prior,

whereas the M/M measure is seen at 0.3% vs. 0.3% prior. The Core PPI Y/Y is

anticipated at 2.0% vs. 2.0% prior, whereas the M/M determine is seen at 0.2% vs. 0.5%

prior. As talked about for the CPI report, the market would possibly look via a beat in

the information contemplating the weaker knowledge from the labour market and the ISM PMIs.

US Core PPI YoY

The US Retail Gross sales M/M is anticipated at

0.7% vs. -0.8% prior, whereas the Ex-Autos M/M measure is seen at 0.4% vs. -0.6%

prior. The last

report stunned to the draw back throughout the

board, though some weak spot was anticipated as a consequence of unfavourable climate circumstances.

One other weak report would add to dovish expectations.

US Retail Gross sales YoY

The US Jobless Claims proceed to be one

of a very powerful releases each week because it’s a timelier indicator on the

state of the labour market. Preliminary Claims carry on hovering round cycle lows,

whereas Persevering with Claims stay agency round cycle highs. This week the consensus

sees Preliminary Claims at 218K vs. 217K prior,

whereas there’s no consensus for Persevering with Claims on the time of writing

though the prior week noticed a rise to 1906K vs. 1889K prior.

US Jobless Claims

Friday

The PBoC is anticipated to maintain the MLF charge

unchanged at 2.50%. The central financial institution not too long ago delivered two greater than

anticipated cuts to its RRR

charge and the 5-year LPR

charge. This weekend the Chinese

Inflation knowledge beat expectations throughout the

board by a giant margin with the Headline Y/Y studying leaping to 1.0% and the

Core Y/Y measure to 1.2%. The PBoC won’t really feel the urgency to chop charges

additional in the meanwhile.

PBoC