UPCOMING EVENTS:

- Monday: New

Zealand Services PMI. - Tuesday: Japan

PPI, UK Labour Market Report, Eurozone ZEW, US NFIB Small Business

Optimism Index, US PPI, Fed Chair Powell speech. - Wednesday:

Australia Wage Price Index, Eurozone Industrial Production, US CPI, US

Retail Sales, US NAHB Housing Market Index, PBoC MLF. - Thursday: Japan

GDP, Australia Labour Market Report, US Housing Starts and Building

Permits, US Jobless Claims, US Industrial Production. - Friday: New

Zealand PPI, China Industrial Production and Retail Sales, Fed’s Waller

speech.

Tuesday

The UK Unemployment Rate is expected to

tick higher to 4.3% vs. 4.2% prior with Average Hourly Earnings (including

bonus) seen at 5.3% vs. 5.6% prior. Barring big surprises, this report is

unlikely to change much for the BoE as the central bank is more

focused on the two inflation reports ahead of the June meeting where it

could deliver the first rate cut. The market sees a 50/50 chance of a rate cut

in June at the moment.

UK Unemployment Rate

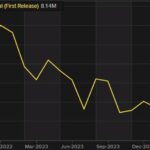

The US PPI M/M is expected at 0.2% vs.

0.2% prior, while the Core PPI M/M is seen at 0.2% vs. 0.2% prior. There’s a

risk of an upside surprise considering that both the prices paid components

in the ISM

PMIs jumped to cycle highs. The market will likely focus more on the US CPI

report coming out the following day, although a hot PPI might trigger some

defensive positioning into the CPI data.

US Core PPI YoY

Wednesday

The Australian Wage Price Index Q/Q is

expected at 1.0% vs. 0.9% prior. The Australian labour

market remains pretty tight with high wage growth and persistently high

inflation. Nonetheless, the RBA at the latest

policy decision refrained from turning overly hawkish as the central bank

continues to wait for more information. The market now sees the first rate cut

sometime in Q2 2025 with even some chances of a rate hike this year. High wage

growth without a looser labour market will likely make it hard for the RBA to

reach their target “within a reasonable timeframe”.

Australia Wage Price Index YoY

The US CPI Y/Y is expected at 3.4% vs. 3.5%

prior, while the M/M measure is seen at 0.3% vs. 0.4% prior. The Core CPI M/M

is expected at 0.3% vs. 0.4% prior. Given the market’s pricing and general fear

of persistently high inflation, a downside surprise will likely trigger a much

bigger reaction than an upside surprise. Fed

Chair Powell pushed back against rate hikes expectations as he stated that they

would need “persuasive” evidence that their policy isn’t restrictive

enough.

So, if inflation remains high but doesn’t

re-accelerate notably, they will just keep rates higher for longer. The market expects

almost two rate cuts (45 bps) by the end of the year which can easily go back

to one or even zero in case we get another hot inflation report. A soft report

might add one extra cut to the pricing but not much more as the Fed will want

to cut rates at a meeting containing the SEP (barring a quick deterioration in the labour market), which falls in September at the earliest.

US Core CPI YoY

The US Retail Sales M/M is expected at

0.4% vs. 0.7% prior, while the ex-Autos M/M figure is seen at 0.2% vs. 1.1%

prior. We got some soft consumer sentiment reports recently which might filter through

lower consumer spending. The retail sales data is notoriously volatile and

given that it will be released at the same time of the CPI report, the market

will likely ignore the release.

US Retail Sales YoY

The PBoC is expected to keep the MLF rate

unchanged at 2.50%. The data out of China has been mostly positive with

the latest inflation

rates slowly crawling out of deflation. Therefore, the central bank is

likely to keep the policy rates steady for the time being given the lack of

urgency.

PBoC

Thursday

The Australian Labour Market report is

expected to show 25.3K jobs added in April vs. -6.6k in March with the Unemployment

Rate ticking higher to 3.9% vs. 3.8% prior. The RBA is more focused on

inflation but if the tightness in the labour market continues, especially

with high wage growth, it will make it harder for the central bank to reach its

target “within a reasonable timeframe”.

Australia Unemployment Rate

The US Jobless Claims continue to be one

of the most important releases to follow every week as it’s a timelier

indicator on the state of the labour market. This is because disinflation to

the Fed’s target is more likely with a weakening labour market. A resilient

labour market though could make the achievement of the target more difficult.

Initial

Claims saw the first notable miss last week coming in at 231K vs. 215K

prior, which was the highest since August 2023. Of course, one miss doesn’t make

a trend, but it’s worth to keep an eye on this given the recent miss in the NFP

report and softer consumer sentiment data. This week Initial Claims are

expected at 220K vs. 231K prior, while there is no consensus at the time of

writing for Continuing Claims although the prior release showed an increase to

1785K vs. 1785K expected and 1768K prior.

US Jobless Claims