UPCOMING

EVENTS:

- Monday: New Zealand Services PMI.

- Tuesday: Eurozone ZEW, Canada CPI, US Retail Sales, US

Industrial Production and Capacity Utilization, US NAHB Housing Market

Index. - Wednesday: UK CPI, US Housing Starts and Building Permits,

BoC Summary of Deliberations, FOMC Policy Decision. - Thursday: New Zealand Q2 GDP, Australia Labour Market

report, BoE Policy Decision, US Jobless Claims. - Friday: Japan CPI, PBoC LPR, BoJ Policy Decision, UK

Retail Sales, Canada Retail Sales.

Tuesday

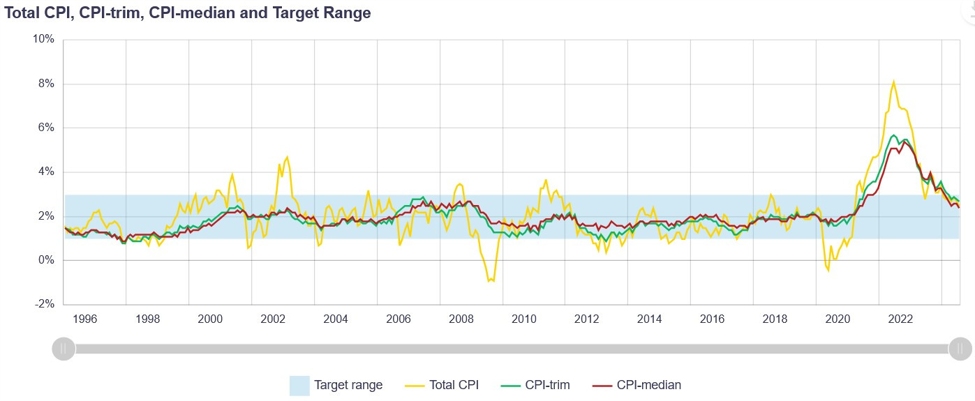

The Canadian CPI

Y/Y is expected at 2.1% vs. 2.5% prior, while the M/M measure is seen at 0.0%

vs. 0.4% prior. As always, focus will be on the underlying inflation measures.

The Trimmed Mean CPI Y/Y is expected at 2.5% vs. 2.7% prior and the Median CPI

Y/Y is seen at 2.3% vs. 2.4% prior.

The BoC is

expected to cut rates by 25 bps at both the last two meetings left for this

year, but there’s also a chance that the central bank delivers bigger rate cuts

if growth and inflation were weaker than projected as Governor Macklem mentioned last week.

Canada Inflation Measures

The US Retail

Sales M/M is expected at 0.2% vs. 1.0% prior, while the Ex-Autos M/M measure is

seen at 0.3% vs. 0.4% prior. The focus will be on the Control Group figure

which is expected at 0.2% vs. 0.3% prior.

Consumer spending

has been stable which is something you would expect given the positive real

wage growth and resilient labour market. We’ve also been seeing a steady pickup

in the UMich Consumer

Sentiment which suggests

that consumers’ financial situation is stable/improving.

US Retail Sales YoY

Wednesday

The UK CPI Y/Y is

expected at 2.2% vs. 2.2% prior, while the M/M measure is seen at 0.3% vs.

-0.2% prior. The Core CPI Y/Y is expected at 3.5% vs. 3.3% prior, while the M/M

figure is seen at 0.4% vs. 0.1% prior.

The market expects

the BoE to keep rates unchanged at the upcoming meeting and then cut rates by

25 bps in November and December.

UK Core CPI YoY

The consensus

among economists sees the Fed cutting rates by 25 bps. The market pricing

though is evenly split between a 25 and 50 bps cut. Some people say that

starting with a standard 25 bps would be better because the economy is still

fine, and 50 bps might be seen as panicky.

Central banking is

also about risk management though. The market pricing is giving the Fed a nice

opportunity to deliver a 50 bps “insurance cut” without surprising. Things

would have been much different if we had something like 30% probabilities for a

50 bps cut and 70% for a 25 bps one.

The Fed didn’t

have the chance to see the labour market report last July as the data was

released two days later. Maybe, if they had the data a week earlier, we might

have seen them cutting by 25 bps back then already and then continuing with 25

bps cuts for the subsequent meetings.

Fed Chair Powell

made it clear at the Jackson Hole Symposium that they will not tolerate more

labour market weakening and they will do everything they can to keep it strong.

Considering everything, starting with a 50 bps cut makes much more sense.

The Fed can then

show that it was just an insurance cut via its Summary of Economic Projections

and Powell can double down on that at the Press Conference. Speaking of the

SEP, the market is expecting the Fed to deliver at least 100 bps of easing by

year-end. The Fed can cut by 50 bps and then project two more 25 bps cuts by

year-end.

Further out, the

market expects the Fed to deliver 150 bps of easing in 2025 which seems too

aggressive at the moment. To sum up, I personally expect the Fed to cut rates

by 50 bps, but in the end what’s important is that the Fed is finally starting

to ease its policy and the magnitude will be shaped by the data in the next

months.

Federal Reserve

Thursday

The Australian

Labour Market report is expected to show 30.0K jobs added in August vs. 58.2K

in July and the Unemployment Rate to remain unchanged at 4.2%. The market

expects the RBA to deliver the first rate cut in February 2025, but the

probabilities can be brought forward to December 2024 if the data

were to disappoint in the next months.

Australia Unemployment Rate

The BoE is

expected to keep rates unchanged at 5.00%. The expectations for such a move

have been shaped by relatively strong data with PMIs firmly in expansion,

inflation moderating at a slow pace and the unemployment rate ticking lower.

The market then expects the central bank to cut by 25 bps in November and

December.

Bank of England

The US Jobless

Claims continues to be one of the most important releases to follow every week

as it’s a timelier indicator on the state of the labour market.

Initial Claims

remain inside the 200K-260K range created since 2022, while Continuing Claims

have been on a sustained rise (although they’ve improved recently) showing that

layoffs are not accelerating and remain at low levels while hiring is more

subdued.

This week Initial

Claims are expected at 230K vs. 230K prior, while there’s no consensus for Continuing

Claims at the time of writing although the prior release showed an increase to

1850K.

US Jobless Claims

Friday

The Japanese Core

CPI Y/Y is expected at 2.8% vs. 2.7% prior. Inflation has been picking up

alongside wage growth which are two of the most important factors for the BoJ. Nonetheless,

the BoJ is expected to keep rates unchanged this time around and potentially

deliver another rate hike by the end of the year.

Japan Core CPI YoY

The BoJ is

expected to keep interest rates unchanged at 0.25%. The focus will be on the

Press Conference as the markets will be attentive to signals or hints on the

timing of the next rate hike.

Several BoJ

officials kept the rate hikes on the table as they want to normalise policy to

a more neutral stance. Markets instability has been a major concern for the central

bank, so they will likely wait for the Fed to be a bit more down the road in

its easing cycle before tightening policy further.

Bank of Japan

The PBoC is

expected to keep the 1 year and 5 year LPR rates unchanged at 3.35% and 3.85%

respectively. The Chinese economic data hasn’t been exactly good and

deflationary risks remain high. Chinese officials should really go harder on

monetary policy easing and bring real rates down from the current high levels.

People’s Bank of China