Matthew Nichols

Introduction

As I recently initiated an extended place in sure problems with most well-liked shares of Wells Fargo (NYSE:WFC), I now must maintain observe of the banking large’s monetary outcomes to ensure the popular dividends are secure. As all most well-liked shares which were issued are non-cumulative in nature (which implies the financial institution can in idea skip a most well-liked dividend and doesn’t need to make up for it), I would like to look at these most well-liked shares extra carefully than others. Though all banks continued to make their most well-liked dividend funds even in the course of the COVID pandemic, I need to maintain shut tabs to make sure I can instantly act if issues would come up.

A have a look at the This autumn outcomes from the attitude of a most well-liked shareholder

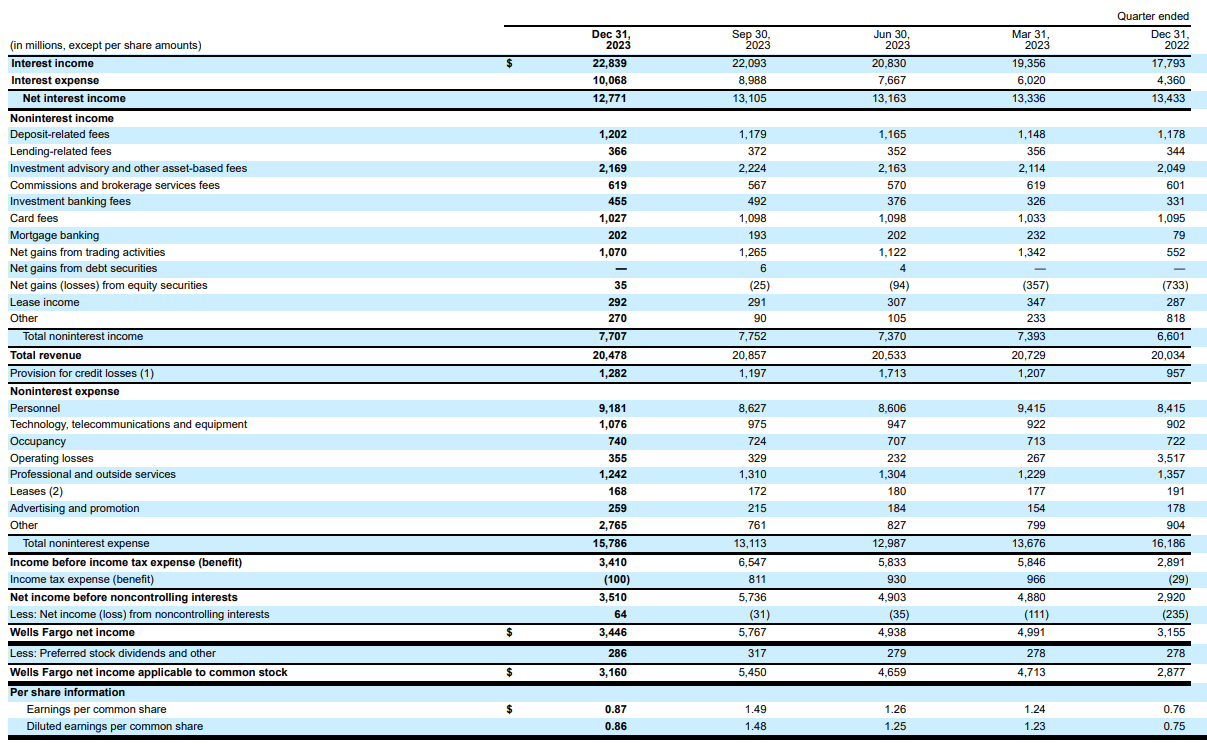

The headline results of the fourth quarter, as posted by the financial institution, was fairly disappointing. Wells Fargo announced an EPS of $0.86 in the course of the fourth quarter, whereas the full-year internet revenue was $4.83 per share. The wrongdoer have been some non-recurring items as a particular evaluation by the FDIC resulted in a $1.9B cost (representing an influence of $0.40 per share) whereas the financial institution additionally allotted $969M for future severance packages. Alternatively, there additionally was a non-recurring tax profit to the tune of $621M, which implies the online influence of the non-recurring objects was roughly $2.25B or $0.43/share. Excluding these This autumn components, the adjusted EPS throughout This autumn would have been $1.29 per share and the FY 2023 EPS would have exceeded $5.25 per share.

The financial institution reported a complete internet curiosity revenue of $12.8B which is barely decrease than the Q3 internet curiosity revenue because the curiosity bills elevated by in extra of 10% whereas the curiosity revenue elevated by just below $750M.

Wells Fargo Investor Relations

The financial institution additionally reported a secure non-interest revenue at $7.7B, whereas the whole quantity of non-interest bills elevated to virtually $16B (however this clearly contains the non-recurring objects I mentioned above). Wells Fargo additionally recorded about $1.28B in mortgage loss provisions and this resulted in a pre-tax revenue of $3.4B and a internet revenue of $3.5B because of the tax profit mentioned earlier on this article. After deducting the $64M in internet revenue attributable to non-controlling pursuits and the $286M in most well-liked dividend funds, the online revenue attributable to the widespread shareholders was $3.16B for a diluted EPS of $0.86 and a reported EPS of $0.87.

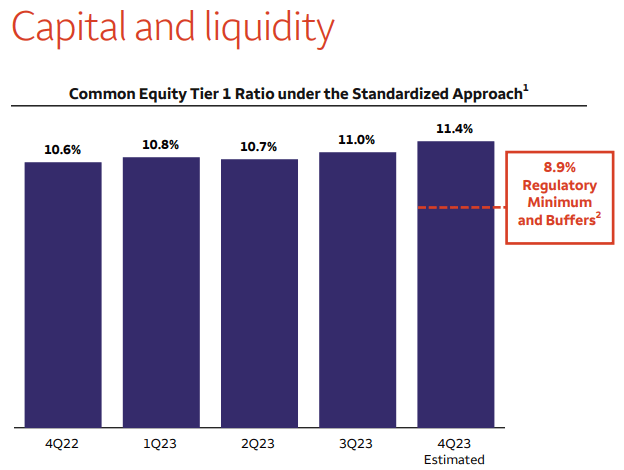

The This autumn outcomes instantly affirm that regardless of the non-recurring objects, the popular dividend continues to be very properly lined. Though the payout ratio elevated to eight.3% in This autumn in comparison with 5.5% and 5.6% in Q3 and Q2 2023 respectively, there’s little or no doubt the financial institution can proceed to pay the non-cumulative most well-liked dividends, even when/when it will get stricken by quarterly multi-billion greenback losses. And regardless of the adverse influence of the non-recurring objects within the fourth quarter of 2023, the capital ratios stay robust with an anticipated CET1 ratio of 11.4% as of the top of final 12 months.

Wells Fargo Investor Relations

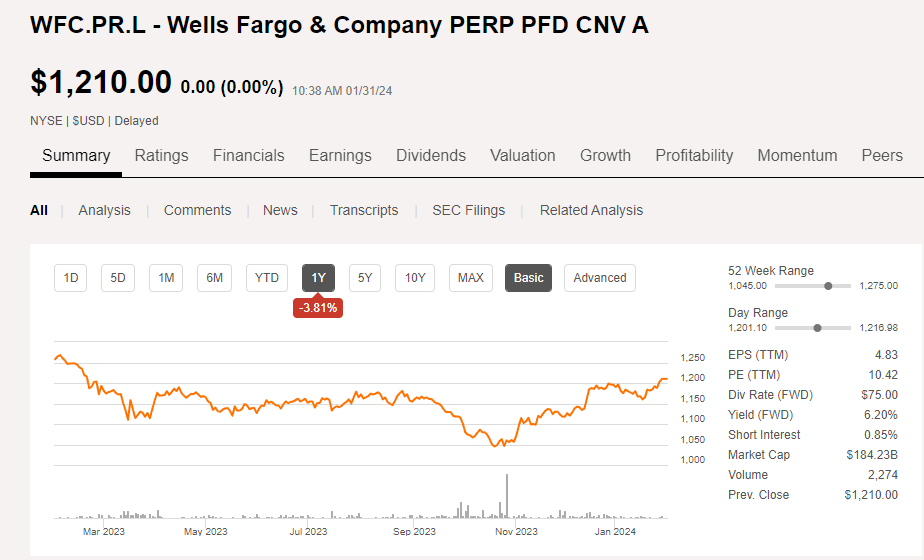

As I disclosed in a earlier article, I began to build up a place in the popular shares sequence L, buying and selling with (WFC.PR.L) as their ticker image. That sequence of most well-liked inventory was initially issued by Wachovia and can’t be known as by Wells Fargo. There’s a conversion function with a conversion value of $156.7, however this solely comes into play when Wells’ widespread shares are buying and selling properly north of $200, as per the phrases of the popular shares.

Searching for Alpha

I think about it to be fairly unlikely that can occur anytime quickly because it implies the share value must quadruple from the present ranges, so for all intents and functions we must always think about this sequence of most well-liked fairness to be a ‘busted’ most well-liked share and its share value will fluctuate primarily based available on the market rates of interest and the danger premium the market attaches to an funding in Wells Fargo.

Funding thesis

On the present share value of $1210, this sequence of most well-liked shares is providing a yield of roughly 6.2%. As market rates of interest are anticipated to proceed to lower, buyers may think about this sequence of most well-liked fairness to be an fascinating software to take a position on stated decreases. If the monetary markets can be high quality with a 5.5% yield on Wells Fargo’s most well-liked fairness, the share value will enhance to roughly $1360 and that will be a stage I’d think about promoting my place at. In the meantime, I wouldn’t thoughts to proceed so as to add to this sequence of most well-liked shares on weak point.