JHVEPhoto/iStock Editorial through Getty Photos

Overview

In an atmosphere of rising prices throughout the board, individuals are in search of methods to save cash any means that they will. Meals continues to be an space the place a big portion of Individuals proceed to really feel the affect of the value will increase. Wendy’s (NASDAQ:WEN) and different quick meals locations alike was once the place that individuals went to eat out for a comparatively reasonably priced worth. Whereas that also appears to be true, gross sales quantity within the restaurant sector is decreasing. This has been a troublesome atmosphere for enterprise to thrive between the upper rates of interest, tightening shopper spend, and rising inflation.

Produce Blue Ebook

Wendy’s caught my consideration as a result of the value has come down from its typical vary between $20 and $22 per share. The value lower has precipitated the dividend yield to spike and now sits at a traditionally excessive 5.3% yield. For reference, the common dividend yield during the last four-year interval was solely 2.5%. Wendy’s is not actually know to be an amazing selection for dividend progress buyers due to the dearth of constant long-term progress and the excessive payout ratio. I really like accumulating earnings from these ‘on daily basis’ kind of enterprise that we see on a regular basis. This precipitated me to take a dive into WEN to analysis whether or not or not this might make for a pretty entry level regardless of the macro challenges.

There are at present over 7,240 Wendy’s areas working inside the US. Of this quantity, 5,627 are operated by franchisees. The corporate does have worldwide publicity, with areas working in 32 overseas nations. To conceptualize the dimensions of operations, McDonald’s (MCD) has over 13,540 areas within the US alone compared. The corporate acknowledges three totally different segments as a part of its operations:

- Wendy’s US – focuses on the operations and franchising of eating places and pulls income from gross sales at firm operated eating places, royalties, and franchise charges.

- Wendy’s Worldwide – focuses on operations and franchises which might be outdoors the US.

- World Actual Property & Growth – contains actual property exercise inside firm owned websites and websites leased from third events.

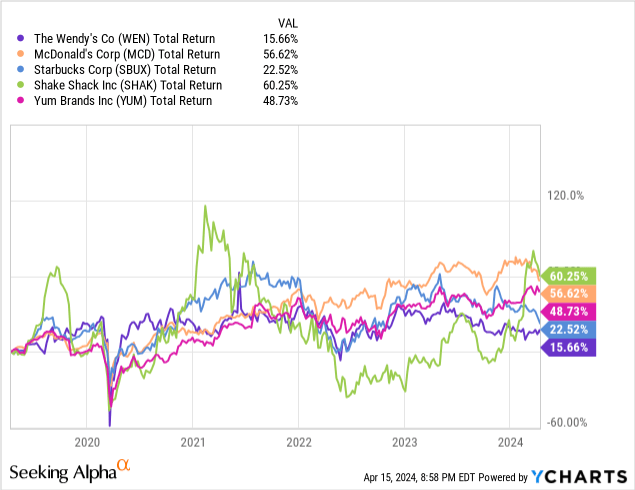

If we evaluate the whole return metric of WEN towards some related friends, we are able to see the underwhelming efficiency. WEN has definitely did not seize the identical upside as some friends, however the worth vary of WEN has managed to remain fairly predictable by staying in a fairly shut vary across the $20 per share mark.

Financials

Over the newest Q4 earnings report, WEN reported progress in complete income, working revenue, and free money circulate. The entire income progress was as a consequence of larger gross sales at firm operated eating places, will increase in franchise royalty, and better gross sales quantity as a consequence of elevated spend on promoting. WEN did effectively managing issues for the reason that pandemic by benefiting from margins and effectively managing money.

For instance, there was a lower usually and administrative bills as a consequence of a lower in worker compensation and headcount. In addition they managed to extend working revenue margins by eliminating promoting spend in the direction of breakfast gadgets. Because of this environment friendly administration, free money circulate elevated.

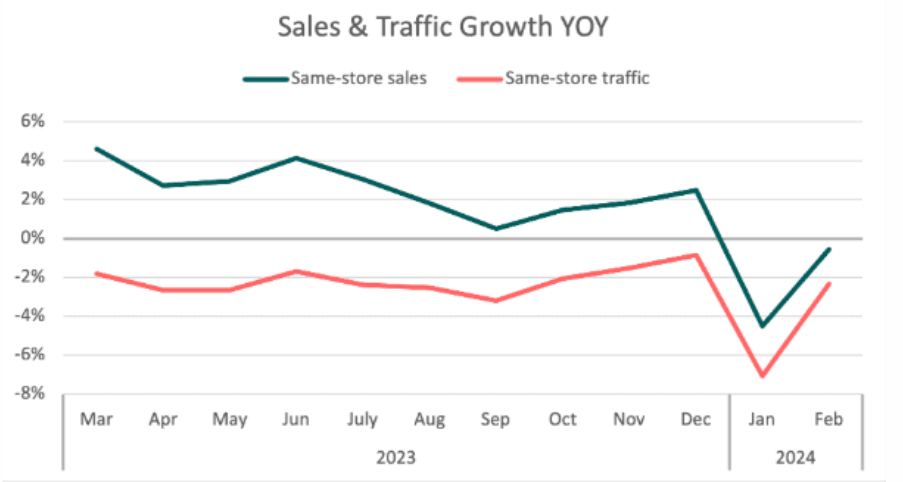

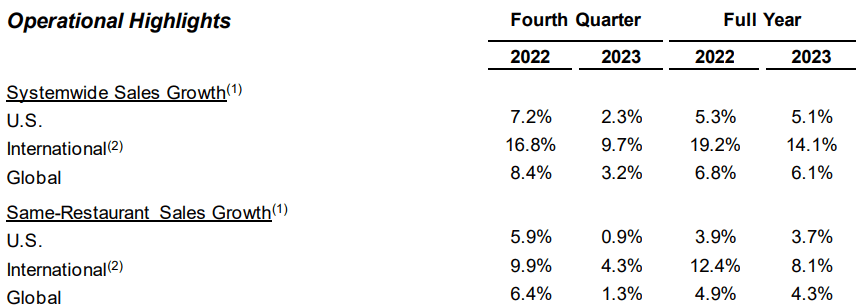

Moreover, systemwide gross sales progress confirmed decreases yr over yr for the US, worldwide, and world. Identical restaurant gross sales progress has additionally slowed down a bit, with the worldwide market seeing the largest affect. Whereas every of those segments did nonetheless present progress, the expansion is gradual. This may possible be attributed to the unfavorable market circumstances. The quick meals {industry} as an entire noticed a decreased degree of site visitors to their areas over the last quarter. For instance, site visitors to quick meals eating places has dipped 2.5% industry-wide. Wendy’s and different quick meals firms have offset this lowered gross sales quantity by growing costs.

WEN This fall Earnings

Nevertheless, I do suppose that administration has been utilizing this time of lowered quantity as effectively as attainable. As I beforehand talked about, they minimize down on bills from SG&A, however additionally they concurrently invested within the modernization and effectivity of the enterprise. The primary funding for this yr was $15M in the direction of the help of dividend progress by their cellular app. Increasing on this income follows the trail of extra widespread chains like MCD, that proceed to see bigger quantities of income originate from cellular orders. Wendy’s truly grew their digital gross sales from solely $250M in 2019, as much as nearly $2B in 2023.

You’ll be able to see how a few of WEN areas now have devoted spots for cellular order pickup. They’ve additionally dedicated $30M in the direction of the rollout of digital menu boards throughout firm operated areas throughout the US. Whereas these capital expenditures could not essentially develop the enterprise, they do make them extra trendy trying and might add to curbside enchantment to re-attract earlier clients.

When it comes to progress sources for his or her financials, they appear to be leaning on the breakfast section to drive extra income. The thought course of right here is that the breakfast section presents extra margin acceleration alternatives since they don’t have so as to add a considerable amount of further labor. Administration additionally plans to take a position $50M, cut up evenly between the US and Canada markets, to amplify progress of the section. We obtained additional affirmation of this on their last earnings call:

We anticipate our funding and plans will drive a 50% enhance in weekly U.S. breakfast gross sales per restaurant over the subsequent two years as we cost ahead on our journey in the direction of incomes our breakfast day half justifiable share of roughly $6,000 weekly per restaurant. We even have plans in place to double down on what makes Wendy’s model iconic. – Kirk Tanner, President and Chief Govt Officer

Dividend

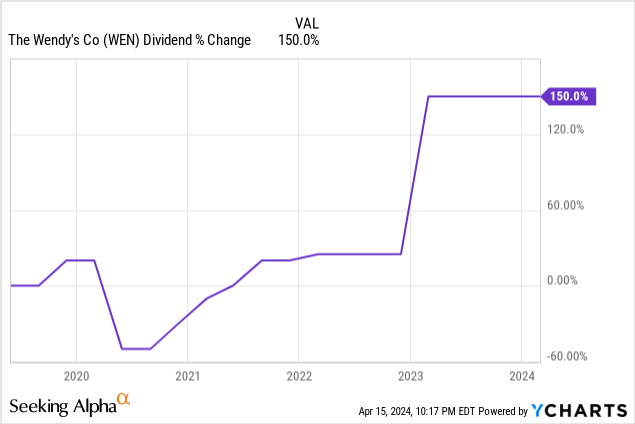

The dividend progress of Wendy’s has been a bit sporadic, beginning again from the pandemic in 2020 the place the dividend was minimize in an effort to protect money. Given the circumstances on the time, that is completely acceptable. Nevertheless, progress since then has been laborious to foretell. That is previous information, however I really feel the necessity to point out it because it is not on daily basis that you just see a elevate this massive. Wendy’s beforehand raised their dividend by 100% in January 2023.

As of the most recent declared quarterly dividend of $0.25 per share, the present dividend yield is now 5.3%. So, as you’ll be able to see, there was no elevate introduced up to now, which is a bit disappointing. On the earnings name, administration acknowledged that they anticipate a $1 dividend for the yr of 2024, so evidently they’re staying conservative with the expansion.

With the present macro challenges, it will likely be fascinating to see if WEN is ready to proceed rising the dividend with massive will increase after 2024 ends. We are able to see that the dividend has elevated by a complete of 150% during the last yr, even when taking the minimize of 2020 into consideration. The dividend has elevated at a CAGR (compound annual progress price) of 18.07% during the last decade. Nevertheless, trying on the dividend payout ratio of 103%, I don’t suppose this sort of progress is probably going.

I would wish to revisit, after the subsequent earnings report, see the progress on the lower of this payout ratio. Which means that WEN is dipping into its retained earnings to pay the dividend in the mean time. Whereas I do not anticipate this to proceed, there’s a danger right here if this goes on for a chronic time frame.

Administration did implement a share repurchase plan that also has funds for use in 2024. As of the final earnings report, there may be $310M remaining that shall be allotted in the direction of this repurchase settlement. Nevertheless, the authorization for these repurchases expires in February 2027. Due to this fact, we could also be ready for an prolonged time frame earlier than we see any of this plan initiated.

Valuation

When it comes to valuation, the value now appears to be buying and selling on the low finish of its current historic vary. We are actually nearing a 5-year low, and entry could seem enticing right here. For example, WEN present trades at a worth to earnings ratio of 19.18x. It is a extreme low cost from the 5-year common P/E ratio of 29.33x. As well as, the common Wall St. price target sits at $21 per share, which represents a possible upside of 12% from the present worth degree. The very best listed worth goal sits at $29 per share.

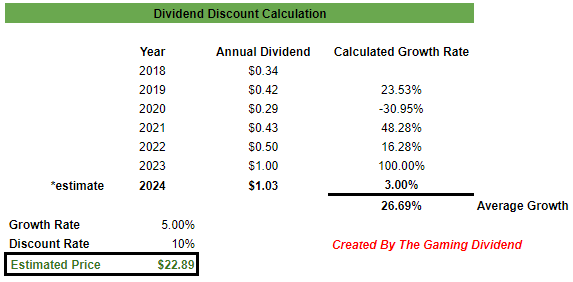

By operating a dividend low cost calculation, we are able to decide an estimated honest inventory worth to see if it aligns with the analyst’s worth targets. By first compiling all the annual dividend payout quantities, we are able to decide the common progress. We are able to see that the prior 100% elevate actually throws off the common progress quantity, although. Ahead EBITDA progress sits at 4.34% whereas the 5-year common EBITDA progress sits at 5.6%. Due to this fact, I’ve averaged these two collectively to get an anticipated progress price of 5%. This aligns with administration expectation in addition to since they venture a worldwide systemwide gross sales progress between 5% and 6%.

Creator Created

I made up my mind an estimated honest inventory worth of $22.89 per share. Whereas this sits barely above the Wall St. common, it comes fairly near being aligned. This estimated honest worth worth of $22.89 represents a possible upside of twenty-two%. Once you mix this with the excessive dividend yield of 5.3%, there may be potential right here for a excessive degree of return. Even when the value by no means breaks the vary above $23 per share, entry right here would nonetheless set you up for a strong short-term return ought to market circumstances enhance for WEN.

The value recovering again to the upper finish of the vary may be very possible when you think about the corporate’s outlook for 2024. Adjusted EBITDA is predicted to land between $535M and $545M. Free money circulate is predicted to develop to a complete between $280M – $290M, which might be a sizeable bump from the present FCF degree of $274M. This extra money circulate may then be allotted for extra share repurchases and different capital expenditures to gasoline additional progress inside the enterprise.

Vulnerabilities

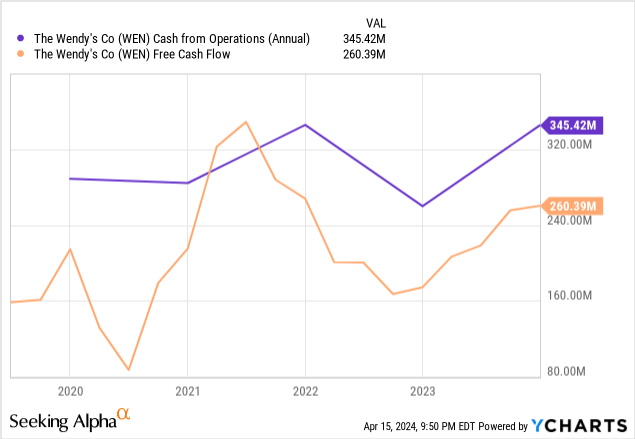

Wendy’s stays extremely weak to shopper spending throughout occasions of financial uncertainty. If the US had been to get plunged right into a recession, gross sales quantity throughout all areas will possible proceed to lower. It will in the end affect earnings and complete web earnings. Whereas WEN has $345M in money from operations obtainable, this complete could not go away the corporate with a ample degree of money to cowl bills.

The dividend payout ratio is already over 100% in the mean time, which can also be a purple flag. For comparability, MCD’s dividend payout ratio is 53%, Yum Manufacturers’ (YUM) payout ratio is 48%, and Starbucks’ (SBUX) payout ratio is 60%. Due to this fact, there’s a actual risk at this degree for the dividend to be minimize earlier than the top of 2024 if circumstances don’t enhance. It would not assist that WEN additionally has a excessive degree of debt. The final earnings report revealed that they’ve near $3B in long-term debt and an curiosity protection ratio of two.45x. The sector median curiosity protection ratio is about 7.11x. This leaves me to consider that the prior 100% dividend enhance was a bit too dramatic and can in the end result in a lower down the street to assist construct a greater money place.

As well as, WEN has not made any significant progress within the proportion of market share they’ve within the quick meals class. WEN at present has a market share percentage of two.18%. For reference, MCD has a market share proportion of 25% and SBUX has a market share of 36%. I don’t suppose WEN has made any impactful modifications to their menu gadgets or any high-profile partnerships to assist drive progress. Till they do, I keep cautious to decide to any kind of long-term place.

Takeaway

Wendy’s is at present buying and selling beneath its typical worth vary. Consequently, a dividend low cost calculation resulted in a good worth estimated of $22.89 per share. This is able to characterize a possible upside of twenty-two%. As well as, the excessive dividend yield of 5.3% makes entry right here very tempting. Nevertheless, WEN would not have a longtime long-term dividend observe file that instills confidence for a long-term dedication. As well as, the corporate has a excessive degree of debt and a comparatively low-interest protection ratio. The corporate is investing into the enterprise ventures that may assist modernize and cater to the digital income stream, however the enterprise lacks any impactful new additions or partnerships that may drive progress to the subsequent degree. Due to this fact, I price Wendy’s as a Maintain as I consider there could also be a short-term upside in worth motion, nevertheless financials go away a bit extra to be desired.