JHVEPhoto/iStock Editorial through Getty Pictures

Funding Thesis

Western Digital Corp. (NASDAQ:WDC) is scheduled to announce earnings later this month on the twenty fifth of April. In continuity with my current theme of home windows to play on the reminiscence restoration, I believe Western Digital must be on traders’ radar for 2024, extra significantly forward of their third quarter of FY24 incomes report, as I see a beat and raised steering forward for the corporate.

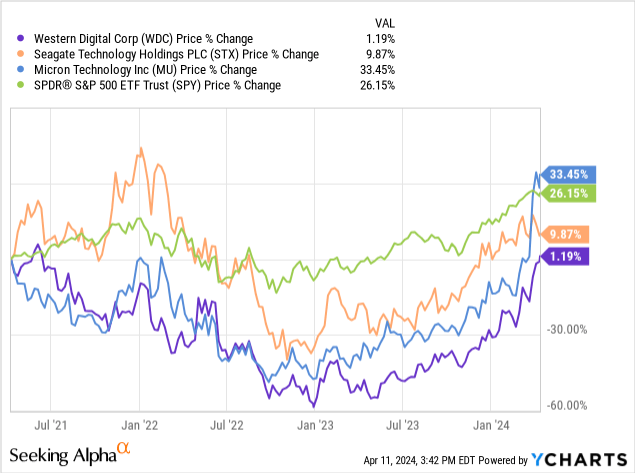

Western Digital is a semi participant with ~$24B market cap and consolidated place within the storage market; administration defines itself as “a leading developer, manufacturer, and provider of data storage devices based on both NAND flash and hard disk drive technologies.” I believe Western Digital’s portfolio throughout flash-based merchandise, or Flash, and onerous disk drives, or HDDs, makes it positioned to develop top-line with the present restoration underway within the reminiscence/storage market. To grasp why this 12 months’s restoration takes such a highlight in my protection, it have to be famous that final 12 months, we noticed a extreme downward cycle for your complete reminiscence and cupboard space, each by way of steep declines in pricing and unit volumes bought. Western Digital, Seagate (STX) (one other storage participant with extra concentrate on the HDD enterprise), and Micron (MU) felt the warmth early final 12 months, as proven within the graph beneath on the three-year chart for the shares towards the S&P 500.

YCharts

What’s completely different now could be that the market corrected, and it corrected deeply. Because of this clients labored by the built-up stock, and the post-correction setting benefited from AI-related momentum driving finish demand, which is sweet information for Western Digital. I believe the inventory ought to commerce increased post-earnings this quarter because the storage market recovers from its cyclical downturn final 12 months. I see extra upside to present consensus numbers for Western Digital’s top-line development and gross margins.

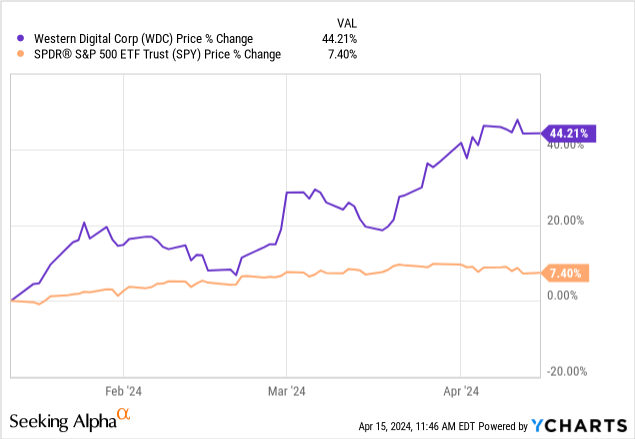

A number of this constructive outlook on the inventory has been acknowledged and factored into the inventory worth efficiency over the previous three months, as proven within the graph beneath. The inventory was additionally pushed increased after Micron reported in late March. So, I perceive why traders would possibly assume the rally is over, however I believe we nonetheless have some extra upside to go, primarily due to improved pricing dynamics that ought to assist better-than-expected income this quarter.

YCharts

Western Digital’s Worth Proposition

The corporate’s fundamental enterprise is break up fairly evenly between the Flash and HDD markets; the previous accounts for 56% of whole web income, whereas the latter accounts for 44%. Of their most up-to-date quarter, the second quarter of FY24, administration reported HDD gross sales up 14% sequentially and Flash gross sales up 7% sequentially; the robust quarter-over-quarter development, particularly for the HDD gross sales (which have been down sequentially 1 / 4 prior) comes from finish market power in cloud and higher common promoting worth or ASP after the downturn final 12 months. I believe Western Digital will keep this upward sequential pattern into the second half of its FY24 based mostly on two elements: higher pricing and demand dynamics and the corporate’s break up.

Western Digital Corp. 10-Q

Let’s dive into the primary motive: higher pricing and demand dynamics. Since Micron stories its earnings outcomes for the three months prior so early within the quarter, I like to make use of it as a ahead indicator to gauge the well being of the demand setting. And, it is no secret that Micron got here out of the quarter with flying colours, with gross sales up within the excessive double digits quarter-over-quarter by 18%. In late December, Gartner reported the next relating to the comeback from final 12 months’s steep downturn: “The worldwide memory market is forecast to record a 38.8% decline in 2023 and will rebound in 2024 by growing 66.3%.” For my part, this extends very visibly to the storage market. HDD market TAM is expanding because of the demand for “high-capacity portable and desktop hard disk drives.” The uptick for each HDD and Flash demand can also be supported by the heightened want for chips that assist AI workloads, which once more is sweet information for Western Digital as a result of AI is among the exceptions to the difficult demand setting for the semi business in 1H24.

Western Digital’s finish market publicity additionally makes it higher positioned to leverage this elevated demand for HDD and Flash; the corporate has three fundamental finish markets: Cloud, Consumer, and Shopper. The majority of income comes from Consumer, however I believe the Cloud finish market will make a comeback in 2HFY24. Western Digital’s 10-Q filing notes that “Cloud represents a large and growing end market comprised primarily of products for public or private cloud environments and enterprise customers, which we believe we are uniquely positioned to address as the only provider of both Flash and HDD.” This conjures up, in my view, confidence within the firm’s future development because the AI whole addressable market expands.

Western Digital Corp. 10-Q

Now, we flip to the second motive I see extra upside: the break up. The corporate announced in late October that it will be separating its HDD and Flash companies; in response to the press launch, “Our HDD and Flash businesses are both well positioned to capitalize on the data storage industry’s significant market dynamics, and as separate companies, each will have the strategic focus and resources to pursue opportunities in their respective markets.” Additionally value mentioning is the extra worth this unlocks for Western Digital shareholders, enabling them to achieve on the upside on two fronts. I believe this was a really calculated and intelligent transfer from administration to spice up confidence within the inventory and each HDD and Flash portfolios. Now, the corporate is on observe for the break up to occur within the second half of 2024. I believe many of the preliminary upside from the break up has been factored into the inventory, however I nonetheless see extra upside in 2H24 upon its completion.

Engaging Valuation

Western Digital may be very engaging at its present valuation, in my view, based mostly on the relative methodology of valuing shares in my protection universe. Western Digital trades at a Value/Earnings ratio of 27.8, decrease than the peer group common ratio of 30.86, in response to information from Refinitiv proven within the desk beneath. I believe traders have a window of alternative for Western Digital forward of earnings, as I imagine the inventory will commerce increased within the second quarter of CY2024.

Picture created by The Techie with information from Refinitiv

What Might Go Improper?

For my part, Western Digital is vulnerable to reporting a wider adjusted loss this 12 months as a result of structural adjustments underway in its plan to separate the enterprise. I proceed to imagine the HDD and Flash demand is wholesome however assume there could possibly be a brief bump within the highway; Reuters reported in late January that the corporate “posted a wider second-quarter loss… due to the impact of structure changes the company implemented in its flash and HDD businesses.” I believe loads of the optimism concerning the break up has already been priced into the inventory, and so I believe there’s a barely increased danger within the present quarter that traders could possibly be stunned by the working bills. I do not assume this can be a motive to draw back from the inventory, nevertheless, as Western Digital’s Flash and HDD segments proceed to learn from the end-demand restoration impressed by the AI increase.

What’s Subsequent?

For my part, Western Digital must be on traders’ watchlist for 2024. I believe the inventory is mostly missed by retail traders and search to reverse that. Administration is now guiding for the March quarter gross sales to develop 6% to 12% sequentially to $3.2-$3.4B, simply beating consensus expectations of $3.09B. To high it off, administration additionally expects sequential development in HDD enterprise, supported by each higher pricing and unit gross sales. Flash gross sales, then again, are anticipated to say no sequentially by way of bit shipments, however I believe that drop might be offset by a greater common promoting worth. All in all, I believe Western Digital’s execs outweigh its cons for 2024. I believe traders ought to preserve a watch out particularly for the improved common promoting worth within the present quarter, which is my indicator for the well being of the cupboard space restoration in 2024.