JHVEPhoto

Funding Thesis

Westinghouse Air Brake Applied sciences’ (NYSE:WAB) development ought to profit from the robust underlying demand, wholesome backlog ranges, and the latest $2bn plus MOU with Kazakhstan’s nationwide railway firm. Furthermore, the continued want of consumers for extra dependable, productive, and environment friendly locomotives and megatrends like urbanization and decarbonization ought to drive the longer-term demand. Additional, the margin outlook is sweet, and it ought to profit from quantity leverage and the continued enlargement of Integration 2.0, a cost-saving initiative. The valuation can also be affordable. So, I’ve a purchase ranking on this inventory.

Income Evaluation and Outlook

The corporate has seen robust income development in latest quarters, pushed by robust world demand and wholesome backlog ranges.

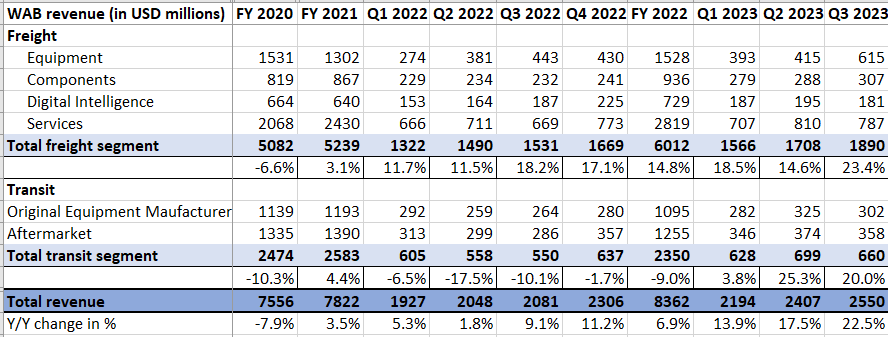

WAB Historic Revenues (Firm Information, GS Analytics Analysis)

The corporate’s income for the third quarter grew 22.5% Y/Y to $2.55 billion, pushed by robust development throughout each the Freight and Transit segments. The Freight section gross sales have been the strongest because the COVID-19 pandemic, because the section income noticed a Y/Y development of 23.4% to $1.89 billion, primarily pushed by the section’s Tools enterprise, which expanded 38.8% as in comparison with the prior-year quarter because of increased locomotive gross sales and elevated demand for the mining merchandise throughout the quarter. Different companies of the Freight section, akin to Parts and Providers, additionally contributed considerably to the corporate’s income development, as increased North American OE railcar construct and share achieve in freight automotive merchandise benefitted the Parts gross sales. Larger modernization deliveries and elevated half gross sales benefitted the Providers enterprise of the Freight section, whereas the Digital Intelligence aspect was down 3.2% Y/Y because of softness within the signaling enterprise.

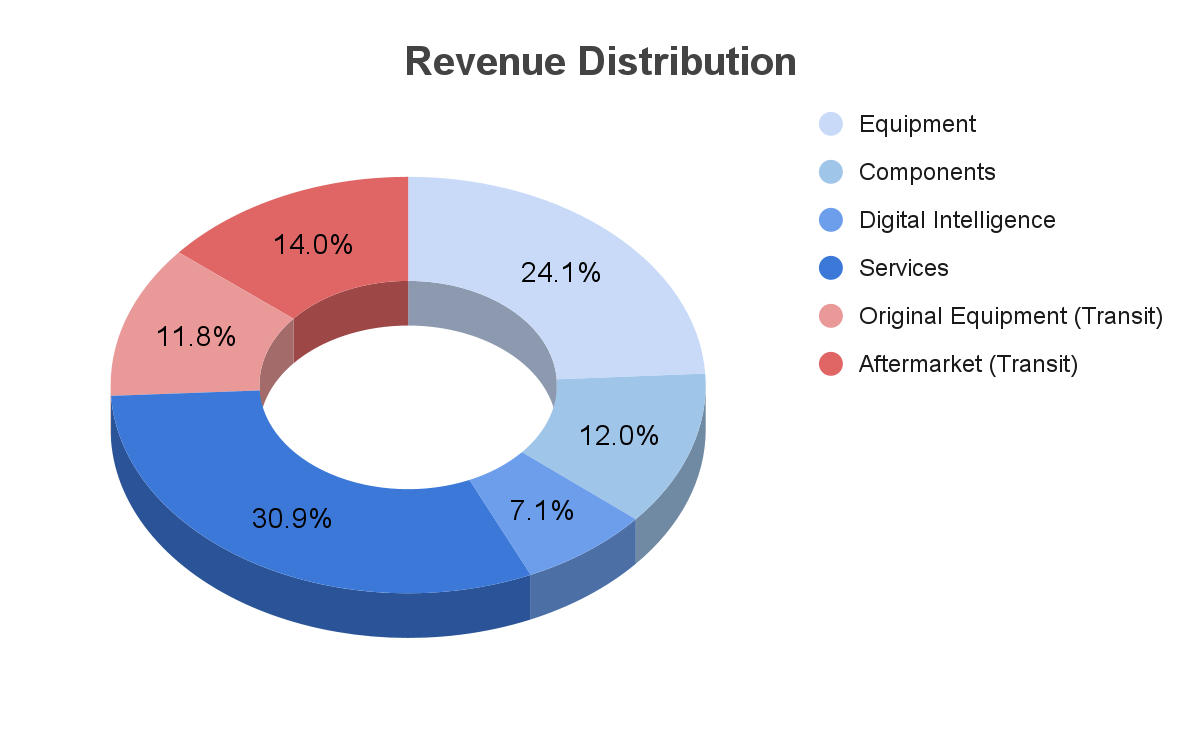

WAB Income Distribution by Product Kind (Firm Information, GS Analytics Analysis)

The Transit section, alternatively, benefitted from robust development in each its OE and Aftermarket companies as in comparison with the prior-year quarter, pushed by the execution of a rising backlog, easing provide chain disruption and simpler comps, leading to a Y/Y development of 20% to $660 million within the section’s income throughout the third quarter of 2023.

Wanting ahead, I’m optimistic in regards to the firm’s income development prospects.

The corporate’s 12-month backlog on the finish of final quarter was $7,091 mn or up 13.1% Y/Y. This offers good visibility on the corporate’s income development getting into 2024. As well as, the corporate has signed a strategic MOU with KTZ, the nationwide railway firm in Kazakhstan for orders over $2 bn, together with supply of locomotives in 2024. This order shouldn’t be but included within the backlog and may add to the energy of already stable backlog ranges. The demand outlook in Kazakhstan is anticipated to stay robust within the coming years because the railway freight visitors from China to Europe, which was earlier transferred by the Russian route, is getting diverted to Kazakhstan post-Russian sanctions.

Along with wholesome backlog ranges, the corporate also needs to profit from the upcoming rate of interest cycle reversal, which ought to catalyze financial restoration and freight volumes. Elevated freight volumes lead to extra upkeep necessities, serving to the corporate’s aftermarket enterprise, whereas decrease rates of interest additionally enhance return on funding on new locomotives and locomotive modernization, growing their demand.

The corporate can also be well-placed to profit from megatrends like urbanization and decarbonization that are driving the necessity for reliability, productiveness, security, gas effectivity, and decrease emissions. Rail transportation is extra environment friendly than highway transportation and may see elevated investments within the coming years each on the Transit and Freight aspect. As well as, the brand new locomotives are far more highly effective, have increased gas effectivity, and lead to decrease emissions, which ought to drive substitute and modernization demand. So, I imagine the corporate is well-placed to see multiyear secular development globally.

Margin Evaluation and Outlook

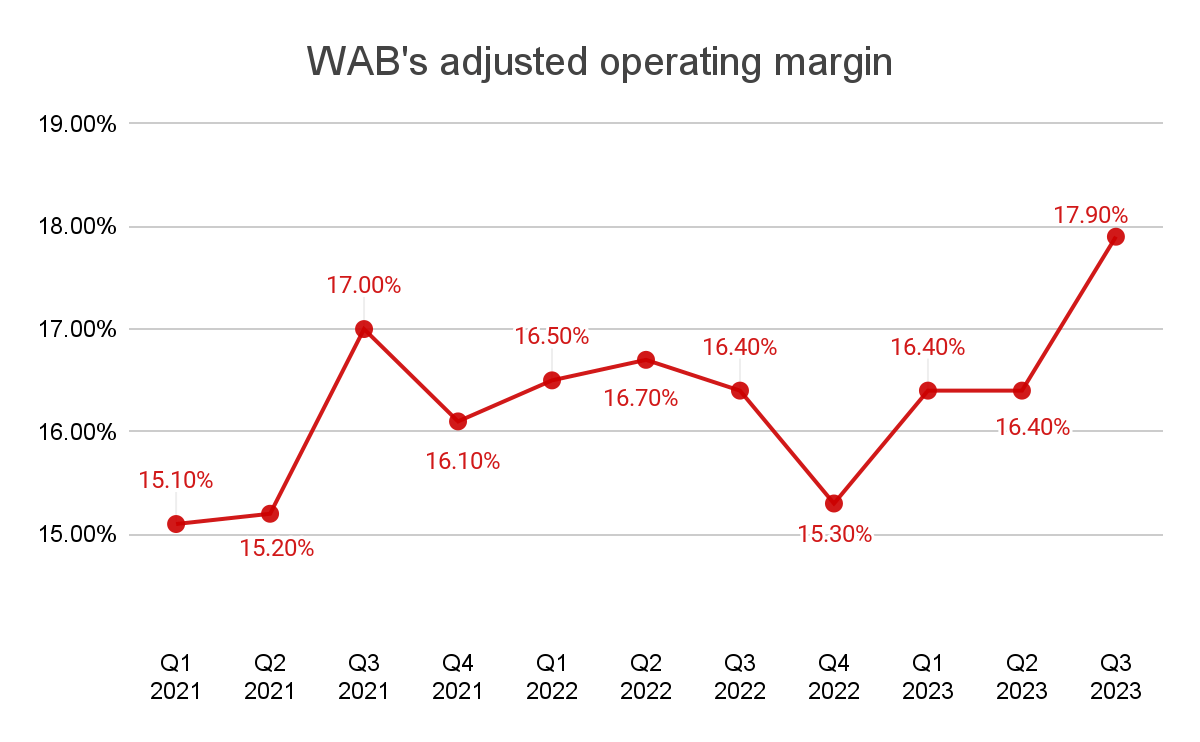

The corporate reported robust margin efficiency within the third quarter of 2023 with 150 bps Y/Y enlargement in general adjusted working margin to 17.9%. This enlargement was pushed primarily by increased volumes throughout the quarter throughout each segments, improved productiveness, and value administration, partially offset by manufacturing inefficiencies pushed by the strike at our Erie facility.

The Freight section posted an adjusted working margin of 21.2%, up 130 bps as in comparison with the prior yr’s quarter, benefiting from robust volumes and decrease SG&A as a proportion of gross sales. The margin within the Transit section improved by 150 bps Y/Y to 12.5%, pushed by robust gross sales quantity, favorable combine, and simpler comps because of cyber impression in Q3 2022.

WAB Adjusted Working Margin (Firm Information, GS Analytics Analysis)

Wanting ahead, I count on the corporate’s margins to profit from quantity leverage as the corporate is anticipated to submit good gross sales development in 2024 pushed by wholesome backlog ranges. Administration is anticipating incremental margins within the 25% to 30% vary.

The corporate can also be anticipated to profit from the continued enlargement of the Integration 2.0 initiative, a 3-year cost-saving plan that’s ramping up. It is a three-year plan began in 2022, with the corporate planning $135 mn to $165 mn funding over the three years to realize a run charge saving of $75 mn to $95 mn by 2025. Often, these plans are front-end loaded by way of funding profile, with financial savings realized towards the again because the cost-saving initiatives get executed. The corporate has already invested $100 mn out of the anticipated $135 mn to $165 mn spend, and as we transfer towards the again half of this cost-saving plan, the funding required ought to lower whereas the fee financial savings ought to ramp up, serving to margins.

Valuation and Conclusion

The corporate’s inventory is at present buying and selling at a P/E of 18.29x based mostly on FY24 consensus EPS estimates of $6.67 and a P/E of 16.50x based mostly on FY25 consensus EPS estimates of $7.40. Over the past 5 years, the corporate has traded at a mean ahead P/E of 18.35x.

WAB Consensus EPS Estimates (In search of Alpha)

The corporate’s near-term income outlook is favorable because of robust underlying demand for the corporate’s merchandise and options and energy within the 12-month backlog. On the similar time, the long-term additionally seems good as a result of firm’s giant put in base in addition to favorable megatrends. The margin outlook can also be optimistic as the corporate advantages from working leverage and its financial savings from price discount initiatives ramp up. The corporate’s EPS is anticipated to develop in double digits for the subsequent few years, and assuming the valuation a number of stays within the excessive teenagers, given good development prospects, I imagine the inventory can ship double-digit annual returns over the approaching years. Therefore, I’ve a purchase ranking on the inventory.

Dangers

Wabtec operates in a cyclical end-market the place railroad firms have deferred their capex in instances of slowdown. So, if my thesis about eventual financial restoration within the coming years because the rate of interest cycle reverses does not show right, the corporate’s enterprise may even see a cyclical slowdown.

The corporate’s shopper base is kind of concentrated, with its main prospects together with tier-1 railroads within the US and state-owned firms in nations like India and Kazakhstan. Any deterioration within the relationship with any key buyer might negatively impression its enterprise.