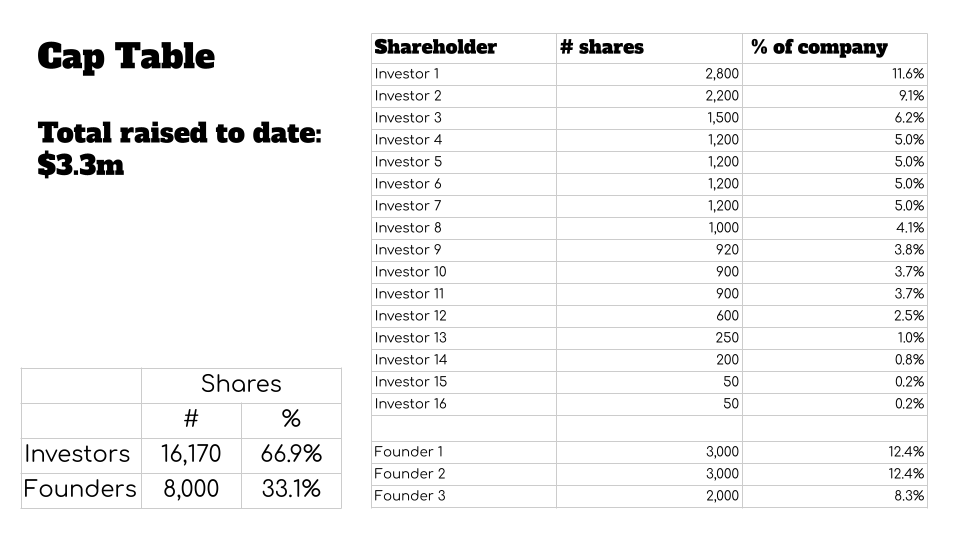

The CEO of a Norwegian {hardware} startup shared a pitch deck with me that had an uncommon slide: It included the corporate’s capitalization desk — the breakdown of who owns what a part of the corporate. Usually, cap tables are shared within the diligence part of investing.

Taking a more in-depth have a look at the desk, one thing considerably amiss:

This cover desk is a reproduced, correct illustration of the cap desk that was within the deck. It’s been simplified and redacted to take away the names of the buyers. Picture Credit: Haje Kamps/TechCrunch

The issue right here is that the corporate has given up greater than two-thirds of its fairness to lift $3.3 million. With the corporate beginning a $5 million fundraising spherical, that represents a severe hurdle.

TechCrunch spoke to quite a lot of Silicon Valley buyers, posing the hypothetical of whether or not they would put money into a founder who offered a cap desk with related dynamics because the one proven above. What we realized is that the cap desk because it stands right this moment basically makes the corporate uninvestable, however that there’s nonetheless hope.

Why is that this such an enormous drawback?

In much less refined startup ecosystems, buyers could be tempted to make short-sighted selections, reminiscent of making an attempt to take as a lot as 30% of a company’s equity in a comparatively small funding spherical. If you happen to’re not aware of how startups work in the long term, that may look like a smart purpose: Isn’t it an investor’s job to get as a lot as they’ll for the cash they invested? Maybe, sure, however hidden inside that dynamic is a de facto poison capsule that may restrict how massive a startup can presumably get. Sooner or later, an organization’s founders have so little fairness left, that the associated fee/profit evaluation of the grueling death-march that’s operating a startup begins shifting in opposition to them persevering with to present it their all

“This cap table has one giant red flag: The investor base owns twice as much as the three founders combined do,” stated Leslie Feinzaig, normal associate at Graham & Walker. “I want founders to have a lot of skin in the game. The best founders have a very high earning potential — I want it to be unquestionably worth their time to keep going for many years after my investment in them … I want the incentives to be completely aligned from the get go.”

Feinzaig stated that this firm, because it stands, is “essentially uninvestable,” until a brand new lead is available in and fixes the cap desk. After all, that, in itself, is a high-risk transfer that’s going to take numerous time, power, cash and legal professionals.

“Fixing the cap table would mean cramming down existing investors and returning ownership to the founders,” Fainzaig stated. “That is an aggressive move, and not many new investors are going to be willing to go to those lengths. If this is the next OpenAI, they have a fair shot at finding a lead who will help clean this up. But at the seed stage, it is brutally hard to stand out so clearly, let alone in the current VC market.”

With unmotivated founders, the corporate would probably exit ahead of it may need in any other case. For these of us who reside and breathe venture capital business models, that’s a foul signal: It results in mediocre outcomes for startup founders, which limits the quantity of angel investing they may be capable of do, taking the entry-level funding out of the startup ecosystem.

Such an early exit would additionally restrict potential upsides for the VCs. An organization that exits later at a far greater valuation will increase the possibility of an enormous, 100x fund-returning consequence from a single funding. That, in flip, signifies that the restricted companions (i.e. the parents who put money into VC companies) see diminished returns. Over time, the LPs will get tired of that; the entire level of VC as an asset class is extremely excessive danger, for the potential of ludicrously good returns. When the LPs go elsewhere for his or her high-risk investments, your entire startup ecosystem collapses because of lack of funds.

There’s a potential resolution

“We definitely want to try and keep seed and Series A cap tables looking ‘normal,’” Hunter Stroll, normal associate at Homebrew, instructed TechCrunch. “Typically investors own a minority of the company in total, the founders still have healthy ownership, which they’re vesting into, and the company/team/pool has the rest of the common [stock].”

I requested the CEO and founding father of the {hardware} firm in query how the corporate acquired itself into this mess. He requested to stay nameless in order to not endanger the corporate or go away his buyers in a foul spot. He explains that the staff had a bunch of large-company expertise however lacked expertise within the startup world. Which means they didn’t know the way a lot work it will take to get the product to market. Internally, he stated that the corporate accepted the phrases “just for this round,” and can pursue a better valuation for the subsequent spherical. After all, as the corporate saved operating into delays and points, the buyers ran a tough discount, and going through the selection of operating out of cash or taking a foul deal, the corporate determined to take the dangerous deal.

The CEO says the corporate is constructing an answer for an issue skilled by 1.7 billion folks, and that the corporate has a novel, patent-pending product that it has been efficiently testing for six months. On the face of it, it appears to be like like an organization with multi-billion-dollar potential.

The present plan is for the corporate to lift the present $5 million spherical, after which make an try at correcting its cap desk later. That’s a good suggestion in principle, however the startup has ambitions of elevating from worldwide buyers who’re going to have some opinions on the cap desk itself. And that will increase questions concerning the founders themselves.

Cleansing up a cap desk

“Situations like these which deserve ‘clean up’ certainly aren’t automatic ‘passes’ but they require the company and cap table to be comfortable with some restructuring in order to fix the incentive structure alongside the financing,” Stroll stated. “If we feel like it’s going to be near impossible to reconcile (even if we play the ‘bad guy’ on behalf of the founders), we’ll often advise the CEO to solve it before raising more capital.”

Mary Grove from Bread & Butter Ventures agrees that it’s a crimson flag if founders personal so little of their firm on the seed stage — and specifically that the buyers personal the opposite 66%, reasonably than among the fairness having gone to key hires.

“We’d want to understand the reasons behind why the company has taken such dilution this early. Is it because they are based in a geography with limited access to capital and some early investors — either not experienced with VC or bad actors — took advantage,” Grove instructed TechCrunch. “Or is there an underlying reason with the business that made it really hard to raise capital (take a look through revenue growth/churn, did the company make a major pivot that made it essentially start from scratch, was there some litigation or other challenge)? Depending on the reason, we could get behind finding a path forward if the business and team met our filter for investment and we believe it is the right partnership.”

Grove stated that Bread and Butter ventures likes to see the founders personal a mixed 50-75% at this stage of the corporate — the inverse of what we see in our above replica — citing that this ensures alignment of curiosity and that founders are given recognition and incentive to construct for the gap forward for a venture-backed firm. She means that her agency may need a time period sheet that features corrective measures.

“We would request that the founders receive additional option grants to bring their ownership up to the combined 50-75% prior to us leading or investing in the new round,” Grove says, however she factors out the problem on this: “This does mean existing investors on the cap table would also share in the overall dilution to make this reset happen, so if everyone is onboard with the plan, we’d hope to be all aligned on the path forward to support the founders and ensure they have ownership to execute their big vision and to take the company through to a big exit.”

Finally, the general danger image relies on the specifics of the corporate, and relies on how capital intensive the enterprise might be sooner or later. If yet another increase might get the corporate to cash-flow impartial, with wholesome natural development from there, that’s one factor. If this can be a sort of enterprise that may proceed to be capital-intensive and would require a number of rounds of great funding, that adjustments the chance profile additional.

Rewinding the alternatives

The CEO instructed me that the corporate’s first investor was a big impartial analysis group in Norway, which regularly spins out its personal corporations primarily based on know-how improvements it has developed. Within the case of this firm, nevertheless, it made an exterior funding at what the founder now describes as “below-market terms.” The CEO additionally talked about that current buyers on its board prompt elevating cash at low valuations. Immediately, he harbors regrets, understanding that the alternatives may put the corporate’s long-term success in jeopardy. He stated he suspected that VCs wouldn’t assume his firm was investable, and ensuring that this problem was entrance and heart for future buyers is why he put the cap desk as a slide within the slide deck within the first place.

The issue might not be remoted to this one founder. In lots of growing startup ecosystems — reminiscent of Norway’s — good recommendation could be laborious to come back by, and the “norms” are generally determined by individuals who don’t at all times perceive how the enterprise mannequin appears to be like elsewhere.

“I don’t want to alienate my investors; they do a lot of good things as well,” the CEO stated.

Stroll says that dangerous actors are, sadly, not as uncommon as he’d like, and that Homebrew typically come throughout conditions the place an incubator or accelerator owns 10% or extra on “exploitive terms,” or the place larger than 50% of the corporate already bought to buyers, or the place a big portion of the shares are allotted to totally vested founders who may now not be with the corporate.

The upshot may very well be if non-local buyers wish to put money into early-stage corporations in growing ecosystems, they’ve an unbelievable alternative: By providing extra affordable phrases to promising early-stage startups than the native buyers are prepared to present, they’ll choose one of the best investments and go away the native buyers to combat over the scraps. However the apparent draw back is that this is able to characterize an incredible monetary drain from the ecosystem: As a substitute of holding the cash within the nation, the wealth (and, probably, the expertise) goes abroad, which is exactly the sort of factor the native ecosystem is making an attempt to keep away from.

==

You probably have information ideas or data for Haje, you’ll be able to share it with him over email or Signal