Bet_Noire

Axsome Therapeutics, Inc. (NASDAQ:AXSM) develops novel treatments for central nervous system [CNS] conditions. The company has two commercial products: Auvelity, which was launched in 2022 for major depressive disorders, and Sunosi launched in the same year for sleep disorders linked to narcolepsy and obstructive sleep apnea.

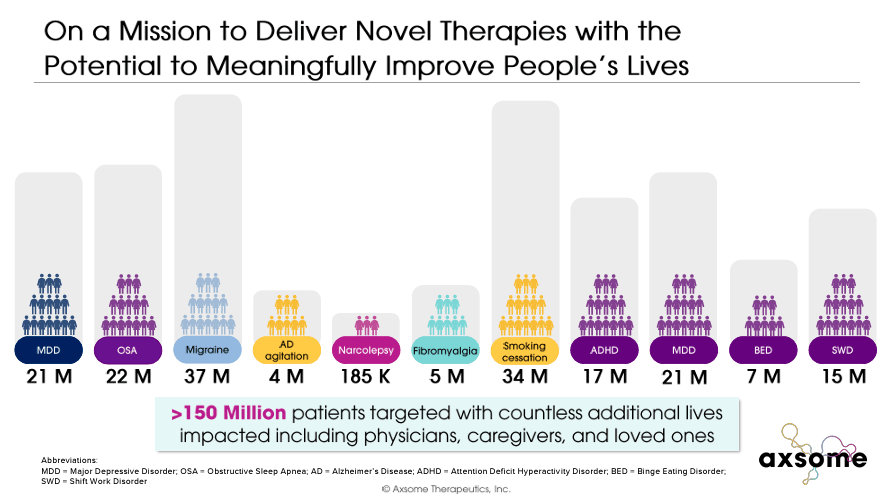

AXSM is also developing a diverse portfolio with late-stage candidates targeting illnesses such as Alzheimer’s disease agitation, smoking cessation, migraine, narcolepsy, fibromyalgia, binge eating disorder, attention-deficit/hyperactivity disorder [ADHD], and shift work disorder. This diverse portfolio addresses the medical needs of more than 150 million people suffering from these psychiatric and neurologic conditions. I believe AXSM is a good buy at these prices, as its revenue potential and likelihood of achieving it outweigh the typical biotech risks.

Billions in Peak Sales: Business Overview

Axsome Therapeutics is a biopharmaceutical company founded in 2012. It is headquartered in New York City and focuses on developing treatments for central nervous system [CNS] disorders. Its main value driver is Auvelity, approved in 2022 for major depressive disorder [MDD]. Executives forecast peak sales of $1 to $3 billion for this particular drug. Additionally, AXSM is commercializing Sunosi and developing other drug candidates that could become significant value drivers, but they are mostly stock catalysts until they receive FDA approval.

Source: Corporate Presentation, February 2024.

The company offers two commercial products: Auvelity and Sunosi. Auvelity was launched in 2022. It is a combination of dextromethorphan and bupropion to address multiple pathways to treat MDD, aiming to provide benefits over traditional antidepressants that usually target only the serotonin system. Auvelity targets the glutamatergic and the catecholaminergic systems with dextromethorphan to reduce depressive symptoms, regulating glutamate levels that influence mood and emotional responses, and bupropion, improving the neurotransmission of norepinephrine and dopamine to sustain its effect.

On the other hand, AXSM’s Sunosi (solriamfetol) was also launched in 2022. It is indicated for excessive daytime sleepiness [EDS] linked to narcolepsy and obstructive sleep apnea. Solriamfetol inhibits dopamine and norepinephrine reuptake to regulate the sleep-wake states by increasing the accessibility of these neurotransmitters in the brain.

Source: Corporate Presentation, February 2024.

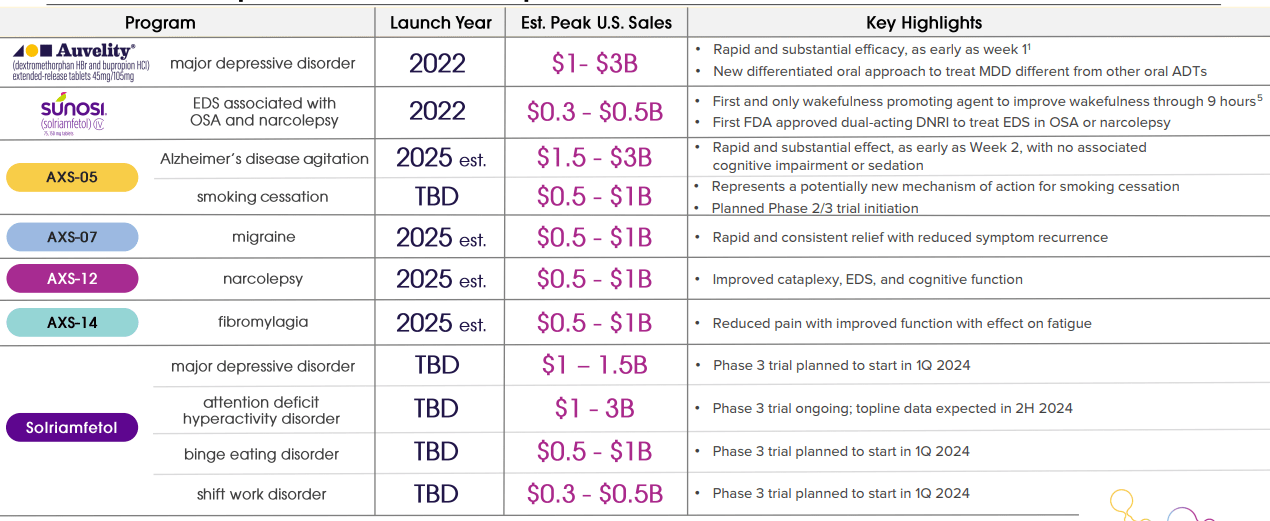

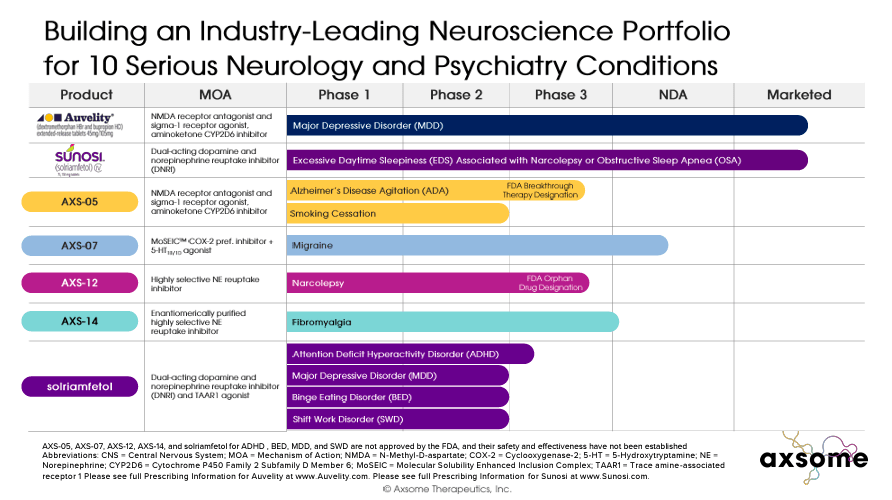

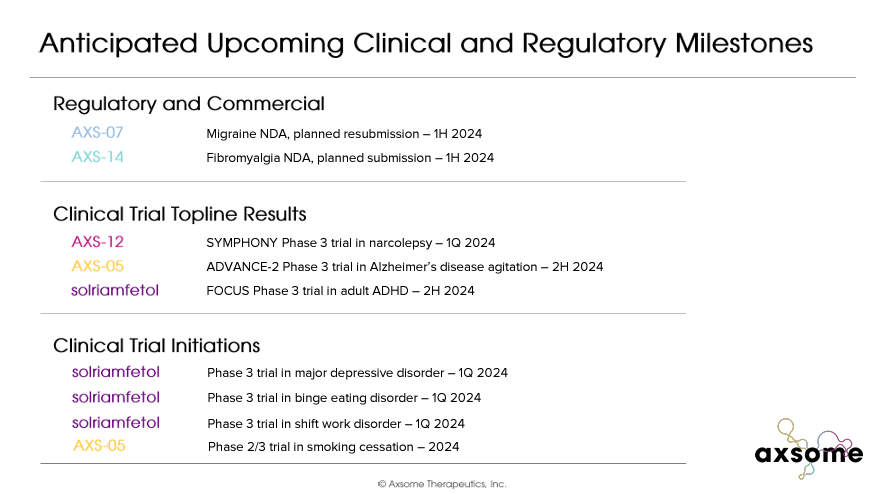

Aside from Auvelity and Sunosi, the company’s pipeline includes five late-stage drug candidates. 1) AXS-05 for Alzheimer’s disease agitation, which is in phase 3 clinical trials with a breakthrough therapy designation by the FDA. AXS-05 is being developed in phase 2 for smoking cessation, which could be a promising value driver in the future as well. 2) AXS-07 is indicated for migraine treatment, and AXSM plans to file in 2H2024 for another new drug application [NDA] approval phase for previous commercialization.

The third drug candidate is 3) AXS-12 for narcolepsy, and AXSM announced results from phase 3, where it met its primary endpoint. This means that AXS-12 is also well on track to obtain FDA approval. 4) AXS-14 for fibromyalgia is in phase 3, advancing to NDA after meeting the primary endpoint of its trials.

Lastly, 5) solriamfetol is in phase 3 for new indications like major depressive disorder [MDD], anticipating topline results in 2025. AXSM also expects to receive binge eating disorder [BED] topline results in 2025. As for attention-deficit/hyperactivity disorder [ADHD], the company expects topline results in 2H2024. Furthermore, solriamfetol is starting phase 3 in Q2 2024 for shift work disorder [SWD].

Source: Corporate Presentation, February 2024.

AXSM’s commercial products and drug candidates treat ten serious psychiatric and neurologic diseases, which impact approximately 150 million patients in the US. Therefore, the market potential is considerable. In fact, AXSM noted that its portfolio could generate peak sales of up to $16.5 billion. Portfolio diversification also mitigates regulatory risks because if one drug candidate fails to receive approval, the company will still have other drugs in the pipeline.

Promising Trials Plus Launches in 2025

In the latest earnings call, AXSM presented the progress of AXS-07 and AXS-14, which are approaching NDA submissions. The company also noted the ACCORD-2 study for the AXS-05 drug candidate prescribed for Alzheimer’s disease agitation. This trial is expected to be completed in 2H2024, with its launch planned for 2025. It’s worth mentioning that AXSM’s ACCORD-2 trial is not required for the FDA submission but is designed to add robustness to the study.

In the call, the executives explained that AXS-05 is positioned as a safer and potentially more effective drug for Alzheimer’s disease agitation than the FDA-approved brexpiprazole. Brexpiprazole, commercially known as Rexulti. Rexulti is an antipsychotic that stabilizes mood by regulating serotonin and dopamine receptors. The executives stated that the clinical trials’ results show that the AXS-05 dual action mechanism offers better symptomatic control with fewer collateral effects, implying that the company’s drug will have a competitive advantage upon approval.

This is key because Alzheimer’s disease agitation is present in more than 70% of AD patients, and it is related to accelerated cognitive decline and increased mortality risk. There were 6.7 million AD patients in 2023 in the US alone, so the market is also sizeable.

Source: Corporate Presentation, February 2024.

As I previously noted, in March 2024, AXSM announced positive topline results for AXS-12, a drug prescribed for narcolepsy. The drug achieved the primary endpoint by reducing the frequency of cataplexy episodes compared to placebo and the severity of excessive daytime sleepiness [EDS], showing good patient tolerance. The FDA has designated AXS-12 as an orphan drug, and executives believe they can initiate its launch year by 2025. If there are no unforeseen delays, AXSM also thinks they could launch AXS-07 and AXS-14 in 2025 for migraine and fibromyalgia.

Room to Grow: Valuation Analysis

However, as you might expect, this is a very intense research effort. So, it’s not surprising that the company stated that developing several clinical trials and preparing NDA submissions have increased research and development expenses from $17.8 million in Q1 2023 to $36.8 million in Q1 2024. Yet, since the company’s balance sheet holds roughly $331.4 million in cash and equivalents, then I’d argue that it can afford this expedited research pace. In fact, given that its portfolio seems relatively close to obtaining more FDA approvals, I believe this is a good strategy. After all, the sooner it obtains the FDA greenlight for more drug candidates, the sooner it can start recouping its investment and generating additional revenue verticals.

Also, even though the company has roughly $178.7 million in total debt, its quarterly interest expenses are just about $1.1 million, which is relatively manageable. Overall, I estimate the company’s latest quarterly cash burn at roughly $53.6 million. I obtained this figure by adding its latest quarterly CFOs and Net CAPEX. If we annualize that cash burn estimate, it implies that AXSM burns $214.4 million annually. Compared to its current cash balances, it’d suggest that AXSM has a 1.5-year cash runway. However, it’s worth noting that AXSM’s revenues are also ramping up quickly, which might extend this cash runway.

Source: Seeking Alpha.

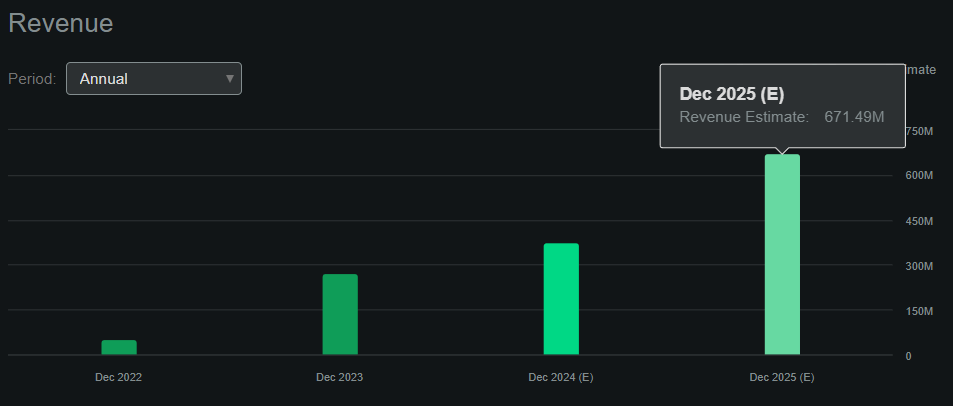

According to Seeking Alpha’s dashboard on AXSM, the company is expected to generate $671.5 million in revenues by 2025, up from $376.2 million in 2024. This would be a YoY revenue increase of 78.5%, and remember that by 2025, AXSM plans to launch several drug candidates. So, I imagine that beyond 2025, the company’s revenues will only continue compounding.

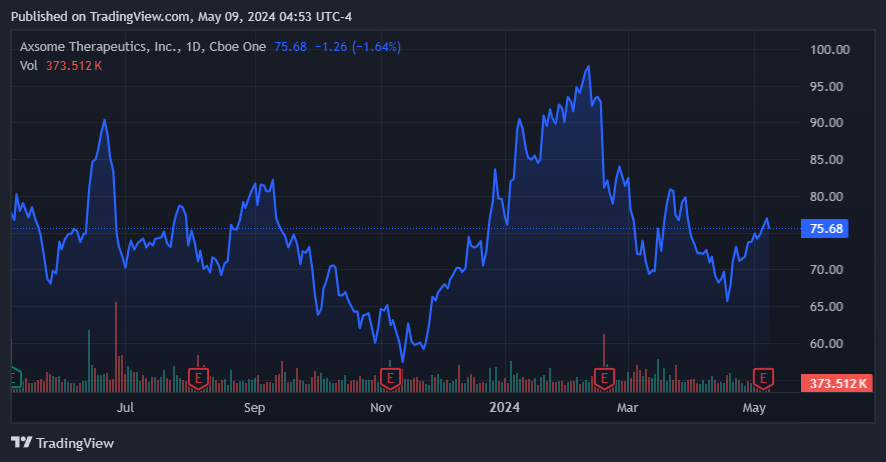

AXSM currently trades at a $3.7 billion market cap, implying a forward P/S ratio of about 5.5. This is slightly higher than the sector median forward P/S multiple of 3.6, but it’s well justified since AXSM appears to be firing on all cylinders for the foreseeable future. Moreover, when we consider that AXSM’s potential peak sales could be $16.5 billion, its current price tag appears cheap by comparison. So, I think AXSM has a strong IP portfolio with a proven track record of obtaining FDA approvals and trades at a reasonable valuation. Hence, I rate AXSM a “buy” as its investment proposition is quite compelling for long-term investors.

Investment Caveats: Risk Analysis

Naturally, the main risks are related to its ongoing clinical trials. If the market is disappointed by the upcoming trial results or the FDA pushes back on them, then it’s likely the stock will decline. This would be reasonable as the stock does seem to trade at somewhat of a premium relative to peers. Moreover, AXSM’s current cash runway of just 1.5 years can be potentially concerning. If its sales on Auvelity and Sunosi don’t continue growing, then shareholders might face dilution risks.

Source: TradingView.

Lastly, while I noted that there’s a potential $16.5 billion in peak sales for AXSM’s drug portfolio, the reality is that market acceptance is not guaranteed either. Moreover, execution risks related to ramping up commercialization efforts have their own risks and challenges, which we can’t discount. But, despite all of these risks, I believe AXSM presents a significant upside at this juncture that far offsets these risks.

Promising Investment: Conclusion

Overall, AXSM’s diversified IP portfolio is promising across all its drug candidates. They are relatively close to obtaining FDA approvals, assuming no setbacks in the regulatory process or clinical trials. AXSM’s IP could generate up to $16.5 billion in sales, which seems like a good opportunity for investors compared to its current market cap of roughly $3.7 billion. However, there are still risks in the picture, but as long as AXSM continues to ramp up its sales of Auvelity and Sunosi, such risks appear manageable. Thus, I rate AXSM a “buy” for investors who understand the inherent biotech risks.