da-kuk

Earlier than Celestica (NYSE:CLS) appeared because the third top-rated stock on the screener, the electronics manufacturing companies agency already gained greater than 140%. Markets priced in robust ends in Celestica’s inventory forward of its third quarter earnings report. Even after assembly expectations, the inventory initially dipped.

Readers is not going to know whether or not the rising inventory market or the conventional course issuer bid of as much as 11.76 million subordinate voting shares compelled the inventory to rise once more. What issues is that Celestica has a “Strong Buy” quant rating.

Celestica A Prime Rated Inventory

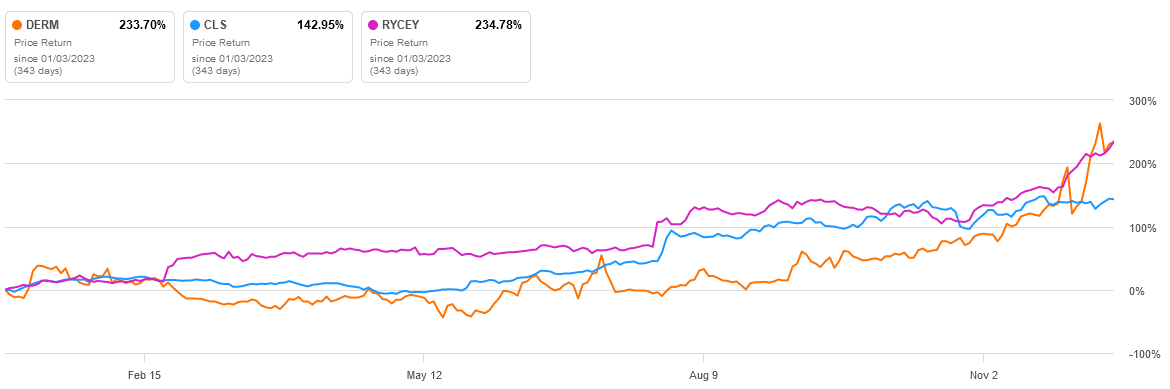

In line with Searching for Alpha’s Prime Rated Inventory screener, refreshed every day, Celestica is third. It scores a 4.98/5.00, matching Journey Medical (DERM) and Rolls-Royce Holdings (OTCPK:RYCEY). Nonetheless, the latter two have stronger SA Analyst and Wall Road Rankings, pushing DERM and RYCEY’s scores to first and second, respectively.

Searching for Alpha Premium

The Searching for Alpha screener for top-rated shares utilized the filters: Quant Rating of purchase to robust purchase, SA Analyst Rating of purchase to robust purchase, and Wall Street Analysts Ranking of purchase to robust purchase. The valuation, development, profitability, momentum, and EPS revisions filters are from A+ to B-.

12 months-to-date efficiency of those top-three shares:

Searching for Alpha

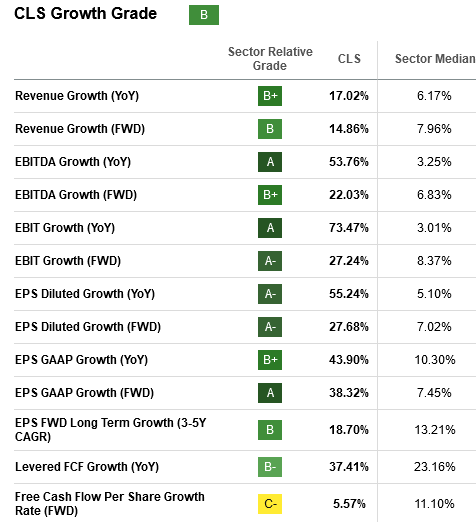

The inventory grades mirror Celestica’s robust Q3 outcomes. Income elevated in two segments. Return on invested capital increased to 21.5%, up from 19.2% final yr. Adjusted free money stream rose to $34.1 million, up from $7.4 million.

Celestica raised its non-IFRS adjusted FCF expectation to $150 million, up from $125 million. Within the quarter, the corporate didn’t purchase again any shares. As guided on the decision, the agency introduced the NCIB program on Dec. 12, 2023.

Peer Quant Grade Comparability

Celestica’s peers include Sanmina (SANM), Plexus (PLXS), Fabrinet (FN), and Common Show (OLED). Celestica has a purchase ranking or larger, as does Fabrinet.

Searching for Alpha

Celestica’s Notable Q3/2023 Highlights

Celestica posted Superior Expertise Options (“ATS”) income rising by 12% Y/Y. Administration expects This fall ATS income to develop within the low single-digit share vary year-over-year. It would profit from double-digit development in its industrial and A&D companies, offset by the continuing market softness in capital gear.

The communications finish market will fall within the mid-teen share vary year-over-year. The weak point is according to telecom shares like Nokia (NOK), Cisco Techniques (CSCO), and Ciena (CIEN) underperforming within the final quarter whereas the expertise sector rose.

The Connectivity & Cloud Options (“CCS”) grew by 2%. Hyperscale is the fastest-growing side of the sector. Nonetheless, Celestica is relying on OEMs that promote into the hyperscaler. Markets are usually not involved that these companies are working via extra stock challenges. The business has expectations that development will return subsequent yr.

Steadiness Sheet Power

Until they’re posting robust income development, buyers are cautious of corporations with excessive debt. Celestica ended the quarter with ample money and gross debt to non-IFRS trailing 12-month adjusted EBITDA leveraged at 1.1 turns. That is down by 0.1 turns Q/Q and down 0.4 turns Y/Y.

Celestica Q3/2023 Presentation

Celestica has a great probability of constant its uptrend. Its internet debt will fall as income rises sequentially from $2.04 billion in Q3 to as much as $2.15 billion in This fall:

Celestica Q3/2023 Presentation

The adjusted earnings per share of as much as $0.71 is above the non-GAAP EPS of $0.65 posted within the third quarter.

Celestica advantages from the surge in demand for synthetic intelligence functions. Income grew from packages ramping up. As well as, proprietary compute from hyperscaler prospects supporting AI functions continued within the quarter.

Celestica’s enterprise finish market has robust momentum. Executives anticipate revenues will enhance within the excessive 20% vary year-on-year. It has tailwinds from demand power in proprietary compute packages from its hyperscaler prospects.

The corporate’s stock stability fell by $85 billion sequentially to $2.26 billion. Stock days internet of money deposit days fell from 85 to 72 year-over-year. Administration anticipates stock days will enhance over the approaching quarters. It is benefiting from materials lead occasions as they proceed to normalize.

All of those metrics point out robust buyer demand and rising momentum.

AI Tailwinds

Hyperscales are rising at almost 30% this yr for Celestica. Demand is so robust that the corporate elevated its materials availability via the tip of the yr. It expects to clear the fabric within the early a part of subsequent yr.

Prime prospects are drawing down Celestica’s stock associated to networking merchandise. Whereas demand for proprietary compute will increase, the corporate will begin ramping up its 800G packages within the second half of 2024.

Celestica scores a B on development. If ahead future money stream grows, Celestica’s total grade might transfer the inventory to the primary or second place of Searching for Alpha’s high rated shares.

Searching for Alpha

Celestica expanded its capability to satisfy AI-related server demand. It has 80,000 sq. toes in capability coming on-line in Q1/2024 in Southeast Asia. It is working with its prospects to increase capability in Thailand, including greater than 50,000 sq. toes. Once they’re on-line, each capability expansionary initiatives will assist AI development. Most significantly, Celestica and its prospects have funding pursuits. This decreases any aggressive menace or contract cancellation dangers.

Nonetheless, Celestica’s prospects depend on its experience in advanced, proprietary compute modules. For instance, they require water cooling. When prospects add new packages, they want Celestica to scale the answer reliably. Shareholders acknowledge that the income from current prospects is rising.

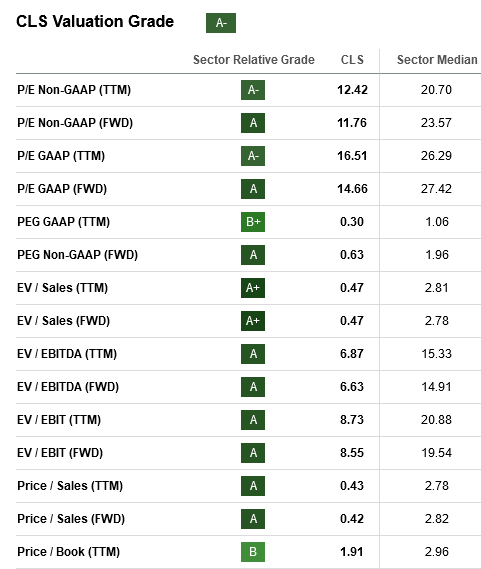

CLS inventory doesn’t commerce at a premium. When different AI shares are over-valued, CLS inventory might commerce even larger. The worth rating is A-. Solely the PEG GAAP and worth/guide have a grade just under that.

Searching for Alpha

Your Takeaway

Because of robust inventory grades, extra readers will uncover Celestica’s elementary power. The ATS and communications items posted wholesome development. The enterprise power continued within the third quarter and has the momentum to speed up all through the following 12 months.

AI is a tailwind. Not like shares that commerce on the AI momentum, Celestica is solidifying hyperscaler income development in partnership with its prospects. This could raise the inventory larger once more and earn it a high decide ranking for 2024.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please pay attention to the dangers related to these shares.