aluxum

While I have written a lot about high-yield investing covering many value plays, I have not elaborated so much on the portfolio construction, my investing objectives, and strategy.

So, the goal of this article is to elaborate on 3 specific aspects that characterize my overall investment allocation process, where, hopefully, some of this will seem interesting and beneficial in the context of your investment approach:

- What are the objectives?

- What asset classes fulfill these objectives?

- What is the key risk?

Let’s now dissect each of these themes separately.

1. The objectives

The overarching objective is to retire early (in ~ 10 years) before the official State pension kicks in without sacrificing the living standards and without being forced to tap into portfolio holdings to fund the retirement.

While I live in a European country and have an official job, where consistent contributions to a defined benefit plan are made, I leave the potential income streams from this component out of the “retirement” equation. In other words, I consider this a favorable optionality that could at some point in time complement the income streams coming from my core retirement portfolio.

It is also critical to have the retirement income correlated to the inflation dynamics so that the living standards can be maintained over the long run. Otherwise, income growth is welcomed but not as important as having maximum yield stability and predictability.

All in all, it boils down to determining monthly (or yearly) living expenses and building up the asset base that produces distributions, which would be sufficient to cover the cost base, while leaving some explicit and implicit margin of safety. With the explicit margin of safety, I mean having higher cash inflows than outflows (living expense), whereas the implicit component refers to the following aspects that should be embedded in the retirement portfolio:

- Dividends or distributions are backed by durable businesses.

- Conservative cash payout ratio, which leaves some capital for growth and adds an additional layer of safety when it comes to dividend stability.

- Robust capital structures.

-

- Income can grow over time and/or at least move in line with the inflation dynamics.

These aforementioned aspects provide a nice segway to the next section of specific asset classes that meet the necessary criteria and thus form a lion’s share of my retirement portfolio.

2. The asset classes

There are three distinct asset classes, which go hand in hand with the overall objective function of capturing defensive, gradually growing and material income streams.

#1 Equity REITs

Equity REITs offer a great mix of return factors, which fit nicely into dividend or income investing strategies. The equity REITs collectively explain roughly 40% of my retirement portfolio.

Just as in any sector or asset class, there are good and bad picks out there. For example, investing in office space, healthcare segment and companies with abnormal leverage profiles or those that do not have an investment grade credit rating can really introduce an excessive risk in the portfolio, where some dividend cuts could likely materialize.

For sound and defensive income investing, investors have to be very selective with REITs. There are three important levers to comply with if the objective is to tick all of the boxes on the implicit margin of safety components that were outlined above.

First, the top line has to be based on long-term lease agreements, which embody periodic escalators. On top of this, the underlying tenant profile has to be diversified and financially sound to avoid the consequences of potential bankruptcies such as we have seen in the retail space.

Second, the capital structure has to be very robust that is underpinned by an investment-grade credit rating. The REIT business is all about capturing positive spreads between the cost of capital and property yields. The presence of an investment grade credit allows for a more attractive spread capture and/or does not force the Management boards to go far in the risk curve by sourcing speculative investment projects just to secure an accretive spread.

Third, the AFFO payout has to be supportive of continued growth in a sustainable manner, whereas the REIT can avoid financing organic growth or M&A just through the expansion of leverage. Having a part of AFFO retained at the REIT level acts also as a dividend protection mechanism since in the case of any decline in the cash generation, the REIT would not automatically fall into a territory in which it has to fund the current dividends from debt or asset sales (i.e., making the dividend cut less likely).

REITs such as Realty Income Corporation (NYSE:O) (see my article here), STAG Industrial, Inc. (NYSE:STAG) (see my article here), and EPR Properties (NYSE:EPR) (see my article here) are great examples that match the necessary criteria.

#2 BDCs

BDCs are another interesting asset class that aligns well with the dividend/income investing strategies. Yet, as opposed to equity REITs, on average, the BDCs are more risky as their inherent nature revolves around sourcing cheap capital and investing in companies that typically struggle to access favorable financing terms from traditional banks. So, defensive and retirement-focused investors have to be extra careful when selecting the right names for stable income investing.

The reason why BDCs are great in this context is because their strategy is to primarily focus on producing stable income streams while keeping price appreciation as a secondary objective. Plus, the yields they offer are commonly higher than what could be obtained from well-known dividend stocks or even below investment grade fixed income alternatives.

When cherry-picking BDCs that possess the right characteristics for accommodating attractive dividends in a sustainable fashion, these are the key financial elements that the BDCs have to possess:

- Investing strategy that is bound only by already cash flowing, well-established and durable businesses (i.e., no investments in VC-type business or CLO structures).

- Majority of the portfolio investments concentrated in senior secured first lien assets.

- High margin of safety when it comes to covering the base dividend with the adjusted net investment income generation.

- Balance leverage profile, where there is no meaningful reliance on fixed rate financing, which has been assumed at below market level rates and now has to be rolled over at much higher interest rates.

The BDCs that really have managed to structure their operations in a defensive fashion and thus can safely service the current (and high yielding dividends) are not that easy to find. Yet, these are the ones, which, in my opinion, carry a huge margin of safety when it comes to distributing stable and predictable income: Ares Capital (NASDAQ:ARCC) (see my article here), Gladstone Capital (NASDAQ:GLAD) (see my article here), and PennantPark Floating Rate Capital (NYSE:PFLT) (see my article here).

#3 Infrastructure

Infrastructure investing is an excellent way to complement the yield-seeking portfolio with income stability and growth over time. The core of investing in infrastructure is about capturing a risk and return factors that are somewhere between bonds and stocks.

Infrastructure assets generate cash flows that come from long-term agreements (just as in the case of REITs), where the pricing is already set, usually with periodic escalators and backed by strong tenants (or users of the asset). In addition to this, the underlying cash flows are not entirely fixed or just linked to CPI (or fixed bumps) as there is an opportunity for infrastructure funds to reinvest the undistributed AFFO into new assets and, more importantly, monetize part of the already de-risked and operational projects, thus unlocking value that could be invested into fresh projects.

The nature of infrastructure business is inherently less risky than, say, BDCs or equity REITs that operate in volatile segments such as malls, offices, and health care. However, when allocating in this space, it is still important to scope companies that have strong balance sheets, conservative AFFO payout profiles and that have the lion’s share of the cash flows based on predictable contracts such as PPAs (power purchase agreements), tariffs or PPPs (public-private partnerships).

In my portfolio, these three names constitute the largest chunk of infra exposure: Brookfield Renewable Partners L.P. Limited Partnership Units (NYSE:BEP) (see my article here), Brookfield Infrastructure Partners (NYSE:BIP)(TSX:BIP.UN:CA)(BIPC) (see my article here), Clearway Energy (NYSE:CWEN) (see my article here).

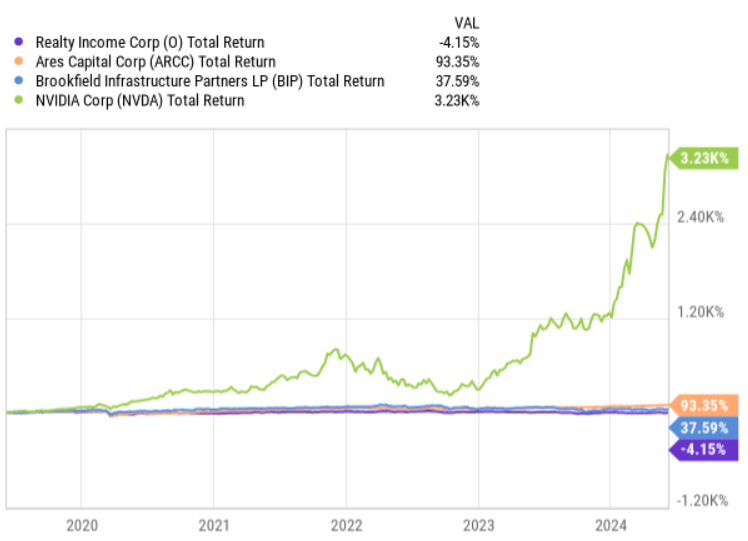

3. The key risk

The key risk in following such a retirement income-focused strategy is nicely captured in the chart below.

Ycharts

Investing in income-producing assets, and especially in those that already offer a meaningful yield from the start, per definition, means that the growth factor is underemphasized. This, in turn, leads to a potential opportunity cost, where in relative terms (i.e., compared to allocating in high-growth names) the total wealth created by a high and defensive dividend strategy is negative.

This kind of argumentation becomes even more relevant in the situations like I am in – early thirties with a long-time horizon ahead.

Here is the thing, why I have chosen to implement a boring and conservative investing strategy to meet my early retirement objectives.

First, I really do not care if some asset or another investing strategy outperforms my income producing portfolio. What matters for me is that the investments that I have made deliver stable and gradually growing current income streams, which allows me to reinvest more and more cash flows as the portfolio gets bigger, thereby minimizing the dependence on my external contributions to the portfolio in the process of achieving the necessary portfolio size for the retirement. Since the goal is to fund my living expenses purely from distributions and do so by a more or less concrete date, the volatility in the portfolio (or underlying companies) does not matter.

Second, to keep some upside optionality in my portfolio, I have specifically introduced a minor satellite bucket under my retirement portfolio, where I can be more offensive and slightly deviate from the core strategy. This bucket consumes 5 – 7% of my portfolio, which is sufficient to capture other risk and return factors, while not imposing too much of a drag (and unpredictability) on the core strategy

Third, the dividend investing just fits my emotional profile better, whereby collecting regular cash flows and seeing them compound as reinvestments, organic dividend hikes or additional contributions are made I increase my chances of actually sticking to this long-term strategy.

The bottom line

Investing in high and defensive yield-producing segments is a sound strategy to reach retirement objectives in a steady and predictable manner if the overall motivation is to cover living expenses with the dividend income without having to divest stakes from the base portfolio.

REITs, BDCs, and infrastructure are asset classes that can help accommodate this objective by producing durable and growing current income streams. Plus, timing-wise this is a very attractive moment when to buy these assets as the more restrictive interest rates have pushed the yields higher.

The key risk of going big on dividend or yield-focused stocks is the opportunity cost of not allocating to growth companies. To mitigate this, investors can introduce a separate bucket (albeit not too significant) in the core portfolios, where specific investments can be made in the growth and non-yielding segments.