IGphotography

I’ve all the time given traders and publication subscribers time to get in earlier than I do. I by no means needed to already be there with out having first given a “heads-up” on the place I’m heading with my very own cash. Equally, I had given a warning on larger danger for Medical Properties Belief (MPW) and am unsure about Hess Midstream (HESM) with the newest information (the acquisition of Hess (HES) by Chevron (CVX)). Since I’m a retiree, I’m adjusting my private danger and shifting in direction of W. P. Carey (NYSE:WPC) an organization that’s prone to recuperate again to the nice previous days. Danger takers might both need all three or stay with each Hess Midstream and Medical Properties Belief.

W. P. Carey Scenario

W.P. Carey was a “SWAN or Sleep well at night stock”. For my part it nonetheless is. However then once more, I have a portfolio stuffed with “disappointments” which have come again from the frustration to return to market favor.

W. P. Carey was lengthy held in very excessive regard by quite a lot of revenue traders. Nevertheless, each nice firm eventually will get to “the end of the road” as a result of any firm can solely develop a lot or predictably produce an revenue stream that grows for a sure size of time.

For me, the truth that Carey did this for thus lengthy earlier than the frustration implies that administration is probably going to return to its profitable methods. But when it ever will get priced to perfection sooner or later, then I’ll possible shrink my place understanding that sooner or later there’s prone to be one other disappointment for traders. Nothing lasts eternally.

However within the meantime:

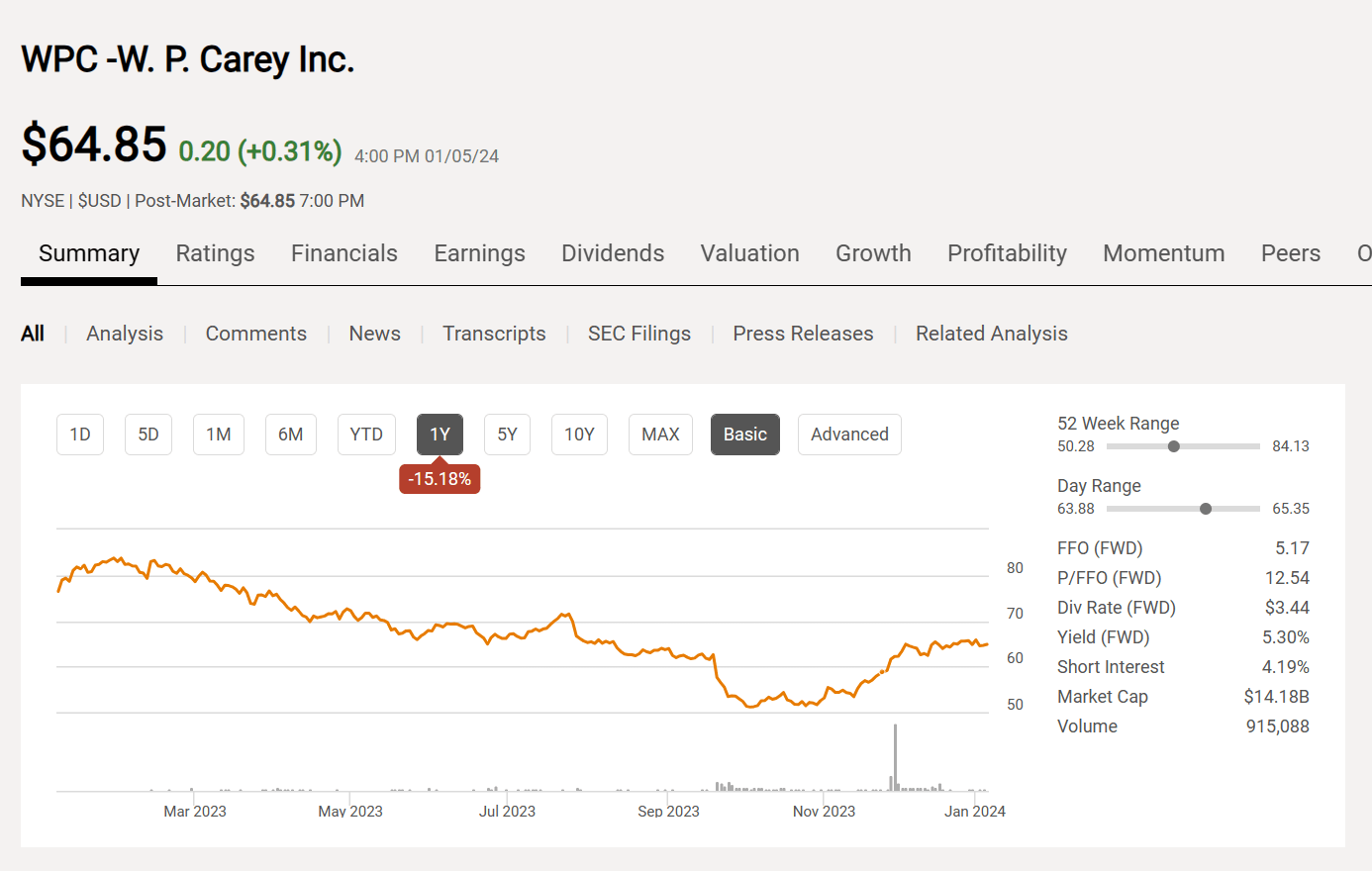

W. P. Carey Frequent Inventory Worth Historical past And Key Valuation Measures (Looking for Alpha Web site January 7, 2024)

The inventory value has clearly rebounded from the announcement concerning the spinoff and the dividend reduce. In late September 2023, administration introduced a plan to spin off what would now be thought of noncore properties. The important thing for traders is that on the similar time administration strongly implied a dividend reduce of an unspecified quantity was on the way in which.

Readers can see the market response above. The inventory was already beneath strain from rising rates of interest. It then headed decrease on the announcement from the $80 vary proven on the chart to just about $50.

But as I noted back then, administration is prone to attempt its greatest to return to the earlier dividend ranges. Whereas that will take a while, a inventory value within the $50’s mixed with a future yield based mostly upon that value is a significantly better proposition than it was with the long run yield based mostly on the earlier inventory value that was far larger. In truth, I could by no means promote even when there’s a hiccup based mostly upon a far larger stage sooner or later.

This administration remains to be dedicated to development. The portfolio remains to be regarded by many as high notch. The one factor that occurred was the spinoff adopted by a decrease dividend. Be aware that the decrease dividend and the decrease inventory value mix for a 5% yield. This can be a higher yield than was the case in latest historical past earlier than all of the rate of interest rises by the Federal Reserve.

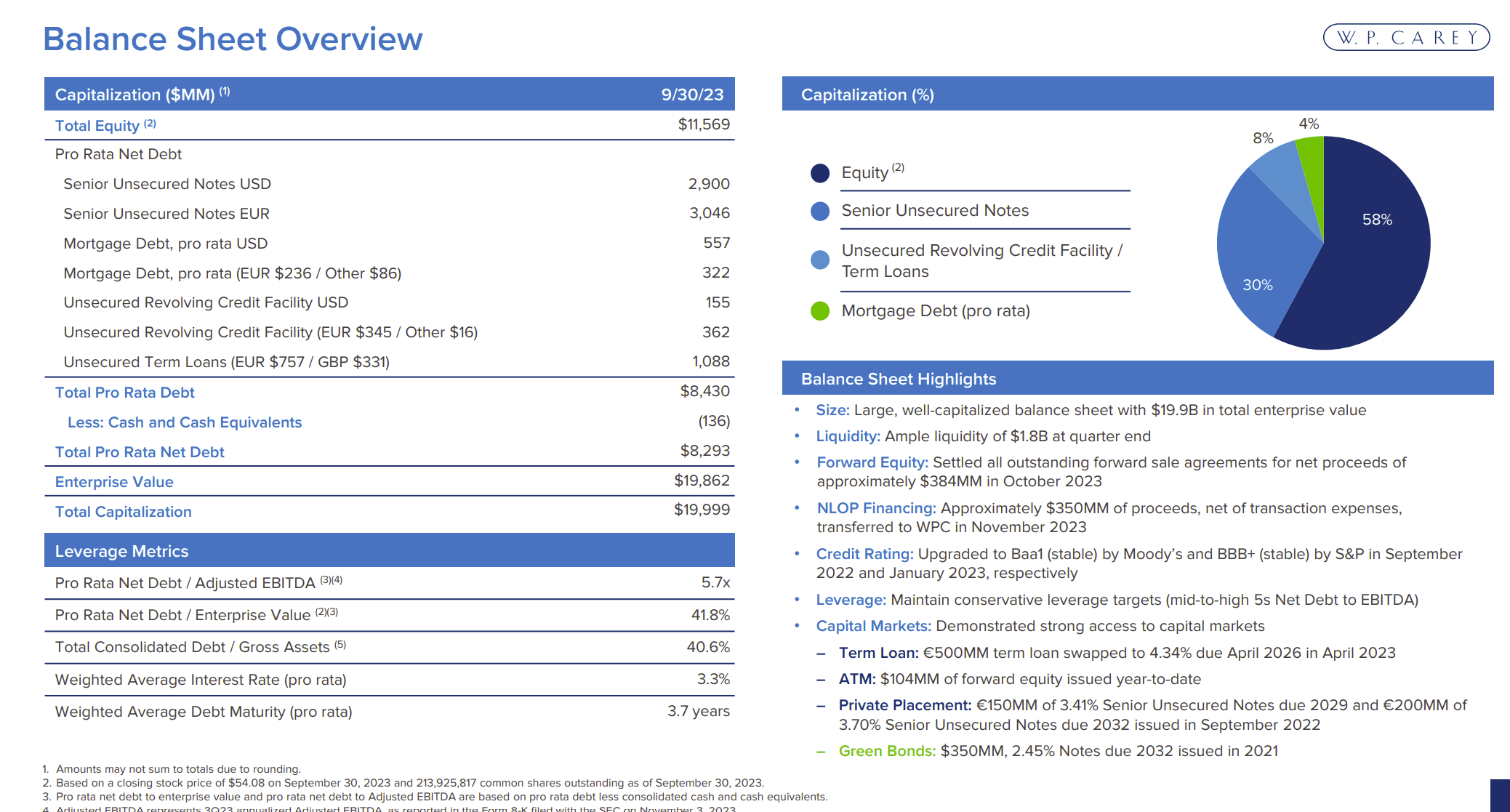

W.P. Carey Abstract Enterprise Statistics (W. P. Carey Investor Presentation Third Quarter 2023)

W. P. Carey is still funding grade. Administration has proven that they’ll deal with a bigger portfolio because the spinoff shrunk the core holdings. There’s each probability that administration will construct the enterprise again to the place it was and doubtless go for a bigger extra worthwhile enterprise sooner or later.

Mr. Market was anxious that rates of interest would by no means come down till the Federal Reserve introduced the inevitable. As I famous previously, inflation was beneath management. Any resurgence can be appropriately met. However there isn’t a signal of inflation issues (resurgence) on the horizon. Therefore the announcement about attainable price cuts has led to an industry-wide inventory value restoration.

This firm has lengthy been considered having a few of the higher measures in addition to a portfolio within the enterprise. It does have a debt to refinance. However any enterprise together with this one, will take care of inflation. Administration doesn’t simply “sit there and take it”. The restoration experience may very well be bumpy. However a restoration with a administration of this high quality is probably going.

Subsequently, I believe that the dividend shall be headed larger sooner fairly than later.

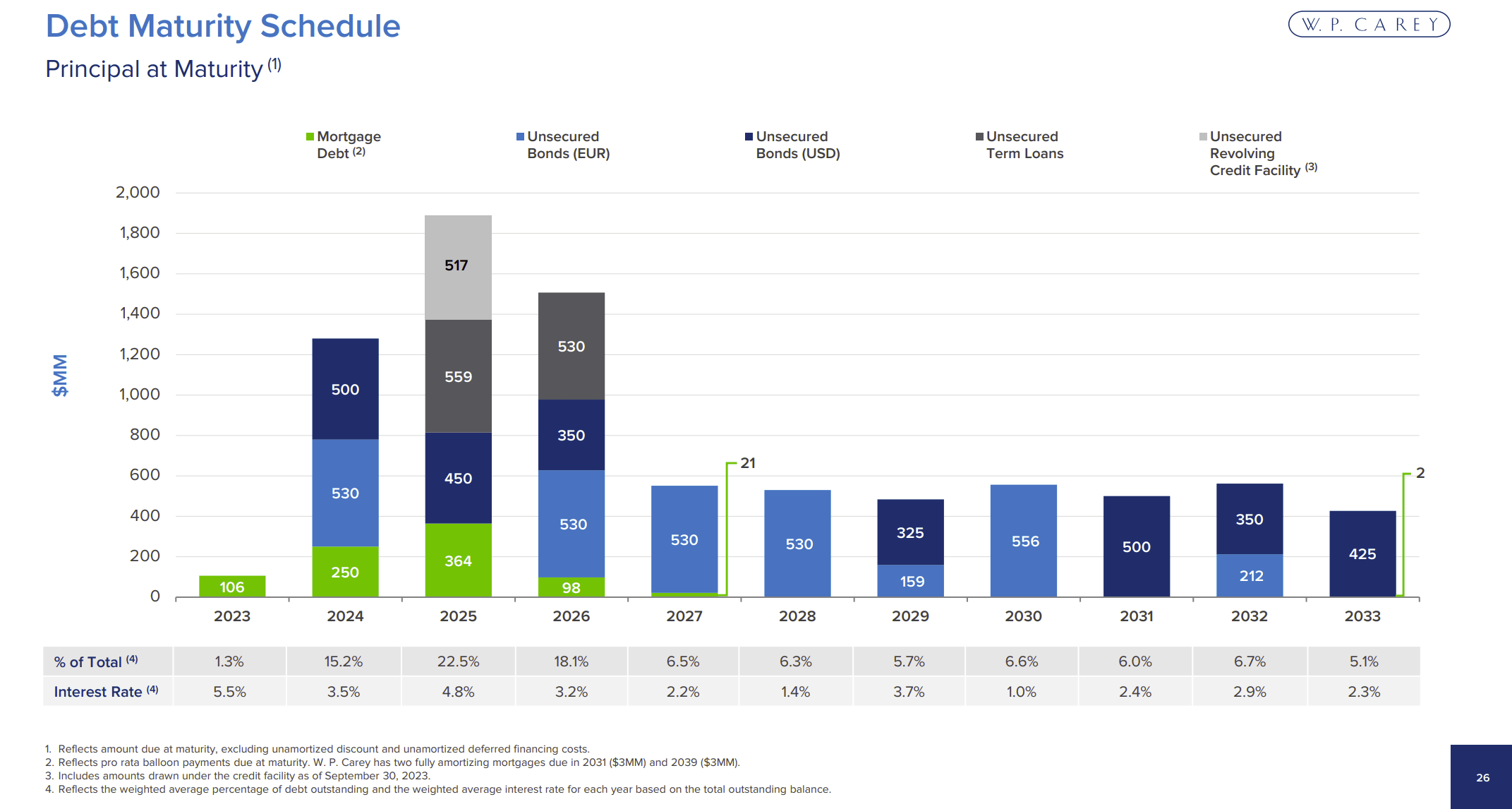

W. P. Carey Debt Due Schedule (W. P. Carey Company Presentation Third Quarter 2023)

Unexpectedly, the Federal Reserve announcement has made the debt due ((quickly)) schedule quite a bit much less regarding than it was. Now this might maintain again the inventory value restoration considerably relying on how this goes. Then once more, administration was going to have roughly $1 billion in money understanding that each one that debt was coming due.

Any offers that administration does will possible be carried out with rates of interest on the present ranges together with inflation protection. Managements like this one weren’t “born yesterday”. Subsequently, they cowl as many affordable contingencies as they’ll earlier than these points occur.

Moreover, there’s some anticipated turnover (lease renewals), some gross sales, and a few purchases. All that mixes to take the sting out of any refinances.

To summarize, the persevering with inventory value restoration (even when bumpy), far exceeds the return when this inventory was considered a “SWAN” inventory.

Hess Midstream

Hess Midstream has lengthy been a kind of firms that basically was not undervalued. However the funding did nicely anyway. Hess is funding grade and the midstream labored nicely with the mum or dad firm to provide above-average returns.

However now, Hess will be acquired by Chevron. The Bakken, the place the midstream operates is unlikely to be the precedence it was for Hess. Hess used the Bakken money movement to fund the Guyana Partnership with Exxon Mobil (XOM).

This uncertainty leads me to need to watch what occurs from the sidelines. Personally, I need to see how nicely the brand new mum or dad firm treats the midstream earlier than I decide to a long-term funding sooner or later. I’ve had various less-than-stellar experiences to need to be cautious concerning the coming merger.

Medical Properties Belief

The problem right here is that administration has issued an replace on the Steward scenario. This can be a material change in Steward’s rickety monetary situation to the purpose that now I’m prepared to ” call it a day” and transfer on. I nonetheless suspect that the corporate will recuperate from the present scenario. Nevertheless, I now suspect that the restoration will take for much longer than I initially anticipated.

I nonetheless assume that the corporate will survive the present announcement. Administration has an excellent file with “customers” that run into bother. Nevertheless, Steward is a major sufficient buyer to have an effect on outcomes for at the very least one other 12 months or two.

If Steward must be changed, that will be a giant job. The inventory value within the present setting would in all probability not go anyplace for at the very least a few years.

Like Hess Midstream, the danger for me, as somebody now retired, has reached previous my stage of consolation. Subsequently, I’m adjusting my portfolio to swimsuit my danger stage. Since I just like the possibilities of an organization recovering from present value ranges, risk-taking traders might nicely determine to both make investments or maintain their shares whereas following the corporate intently.

Abstract

I’m adjusting my investments to swimsuit my retired standing and my danger consolation ranges on the present time. W. P. Carey’s administration appeals to me as a really succesful administration that has had a foul 12 months. This usually occurs to any administration eventually. However good managements have quite a bit much less dangerous years (and people dangerous years change into much less vital as nicely) than mediocre or poor administration.

I believe that administration will once more purchase that SWAN label and the premium pricing that goes with it. I additionally assume that administration will get again on the expansion monitor.

Alternatively, it’s time for me to depart Hess Midstream and Medical Properties Belief for one thing I’m far more snug with. I’d not fault those that can tolerate the danger for holding on as each firms have carried out decently for shareholders previously and so they might but ship a greater future than I anticipate proper now.