Victor Golmer/iStock Editorial through Getty Pictures

Introduction

Shopper staples shares are most valued by traders for his or her low volatility and their dependable (however often reasonably sluggish) development and returns. The Swiss big Nestlé S.A. (OTCPK:NSRGY, OTCPK:NSRGF) suits this sample very effectively, no less than on the floor. It’s a big firm (market capitalization of CHF 250 billion or $278 billion) with a really lengthy historical past and operations world wide. It owns a lot of leading brands in chocolate, confectionery, cereals, frozen meals, dairy merchandise, ice cream, and pet care. Additionally value mentioning is its 20.1% stake in French private care firm L’Oréal S.A. (OTCPK:LRLCY, OTCPK:LRLCF, see my in-depth review), which is at the moment value round CHF 44 billion, or $49 billion.

Nevertheless, regardless of the corporate’s undoubtedly sturdy portfolio, its inventory is at the moment performing very poorly. NSRGY shares have fallen by greater than 25% from their all-time excessive on the finish of 2021. Trying on the efficiency on the SIX Swiss Alternate in its residence foreign money – the Swiss franc – the inventory is down roughly 26% from its all-time excessive. In keeping with Seeking Alpha’s valuation dashboard, Nestlé inventory is at the moment buying and selling at a ahead price-to-earnings ratio of 18, which compares extraordinarily favorably to the long-term common of over 23. The present dividend yield of three.16% can be effectively above the long-term common of two.51%.

The valuation clearly seems compelling, however does that make NSRGF inventory a great funding? I do not assume so. On this article, I’ll share the the explanation why I do not need to add the inventory to my portfolio and why I’m even inclined to say that Nestlé inventory will not be investable.

No Free Money Circulate Progress For At Least A Decade

My common readers know the worth I place on free money movement, or FCF. For my part, an organization that doesn’t have a dependable and rising free money movement will not be value investing in. In spite of everything, free money movement is the prerequisite for sustainable shareholder returns, similar to dividends and share buybacks.

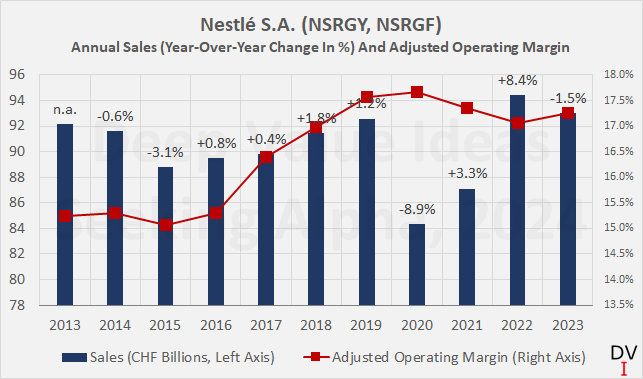

Usually, corporations develop their free money movement by growing their gross sales and sustaining a strong money movement conversion (working revenue after tax is essentially transformed into free money movement). Nevertheless, in Nestlé’s case, gross sales have stagnated during the last decade: in 2013, the corporate generated round CHF 92.2 billion, and the recently reported figure for 2023 was solely marginally larger – CHF 93.0 billion (Determine 1, blue bars).

However what feels like a serious problem shouldn’t be over-interpreted. Nestlé is what may be known as a “portfolio management” firm. It acquires manufacturers that administration sees as promising (by way of development prospects and profitability) and divests manufacturers that aren’t performing effectively. That is mirrored on the one hand within the related money flows from investing actions within the firm’s money movement statements, but additionally within the margin growth (Determine 2, crimson line). Over the past eleven years, Nestlé’s working margin (primarily based on underlying, or adjusted working revenue) has elevated by round 200 foundation factors.

Determine 1: Nestlé S.A. (NSRGY, NSRGF): Annual gross sales and adjusted working margin (personal work, primarily based on firm filings)

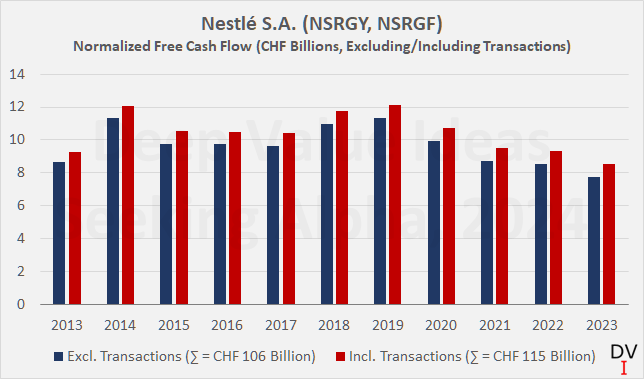

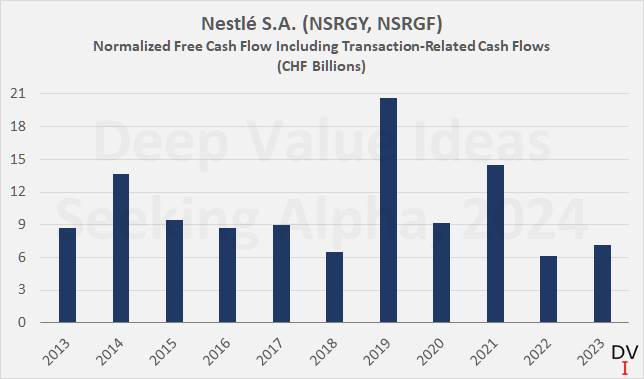

The revenue margin growth is unquestionably a optimistic signal, however I’m at all times a bit of cautious when utilizing adjusted figures in my analyses. free money movement – after adjusting the numbers for working capital actions utilizing a three-year rolling common and subtracting stock-based compensation – the scenario could be very completely different. Nestlé’s free money movement has been flat for no less than a decade. Determine 2 reveals normalized free money movement (nFCF) excluding (blue bars) and together with acquisitions and divestitures in addition to money flows associated to investments in joint ventures (crimson bars). For my part, the latter is a extra reasonable illustration of Nestlé’s money technology potential, particularly as the corporate usually modifies its model portfolio.

Determine 2: Nestlé S.A. (NSRGY, NSRGF): Free money movement, adjusted for working capital actions and stock-based compensation, excluding and together with transaction-related money flows, the latter through the annual common (personal work, primarily based on firm filings)

Relying on whether or not acquisitions and divestitures are excluded or included, Nestlé generated CHF 106 billion or CHF 115 billion of free money movement since 2013, respectively. As a aspect notice, I’ve included the transaction-related money flows by totaling all money flows since 2013 and including/subtracting the annual common to/from nFCF. On this manner, the money flows seem a lot smoother and are simpler to interpret. For causes of transparency, nevertheless, the annual nFCF together with the precise transaction-related money flows are proven in Determine 3. The extraordinarily excessive free money movement in 2019 and 2021 is especially noteworthy: in 2019, Nestlé sold its Skin Health business for CHF 10.2 billion, and in 2021 it reduced its stake in L’Oréal by 22.26 million shares for CHF 9.3 billion.

Determine 3: Nestlé S.A. (NSRGY, NSRGF): Free money movement, adjusted for working capital actions and stock-based compensation together with precise transaction-related money flows (personal work, primarily based on firm filings)

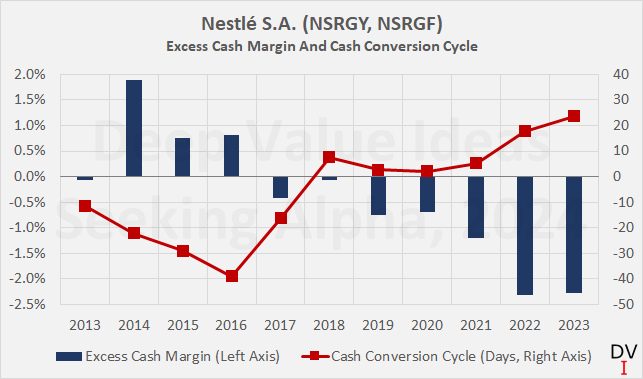

Returning to nFCF together with transaction-related money flows through the annual common, I calculated a variant of the surplus money margin (ECM, blue bars in Determine 4). The ECM is a straight-forward measure of money movement conversion, which I’ve defined intimately in another article. For a mature firm like Nestlé, a roughly flat ECM must be anticipated. Nevertheless, its ECM has been declining since 2014, which signifies that money flows should not preserving tempo with earnings.

An essential cause for Nestlé’s more and more poor money movement conversion is the administration of working capital. The times gross sales excellent is comparatively lengthy at round 35 days, and the times payables excellent has even fallen from round 130 days in 2014 to lower than 110 days in 2023. Stock days has elevated considerably – from lower than 70 days to virtually 100 days in 2023. The mixture of those metrics – the money conversion cycle – confirms that Nestlé’s working capital administration has vital room for enchancment (crimson line in Determine 4).

Determine 4: Nestlé S.A. (NSRGY, NSRGF): Extra money margin, calculated through working earnings and free money movement, and money conversion cycle (personal work, primarily based on firm filings)

Taken collectively, it’s disappointing to see that Nestlé’s administration has apparently not been in a position to develop free money movement during the last eleven years, each when excluding and together with transaction-related money flows. To be truthful, and realizing how massive Nestlé is, it’s undoubtedly not simple to amass promising manufacturers at cheap valuations and execute divestitures of underperforming manufacturers at nonetheless engaging multiples. Sustaining extremely environment friendly working capital administration is after all equally tough for such a broadly diversified firm, however nonetheless disappointing from a shareholder’s perspective.

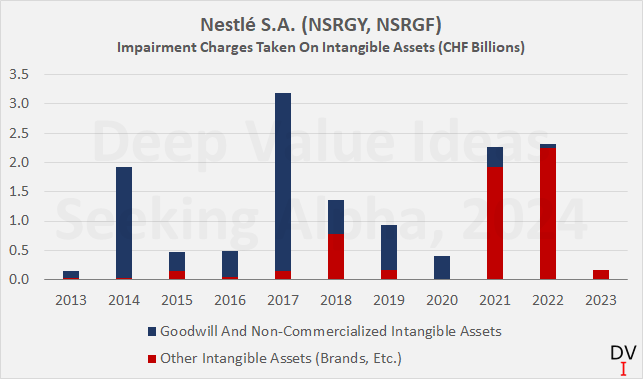

Lastly, it must also be famous that impairments on intangible belongings similar to goodwill and brand-related belongings are fairly excessive at Nestlé, suggesting that acquisitions are generally too costly and/or show to be much less worthwhile than initially anticipated. Determine 5 illustrates the impairment costs of intangible belongings since 2013 – during the last eleven years Nestlé has needed to acknowledge CHF 13.6 billion in write-offs.

Determine 5: Nestlé S.A. (NSRGY, NSRGF): Impairment costs taken on intangible belongings (personal work, primarily based on firm filings)

Irresponsible Steadiness Sheet Administration And Shareholder Returns

That Nestlé has not been in a position to develop its free money movement for no less than the final ten years and appears to generally tend to overpay for its acquisitions are main issues in themselves. However as a conservative and long-term oriented investor, I discover the truth that the standard of the balance sheet has deteriorated considerably over this era much more worrying.

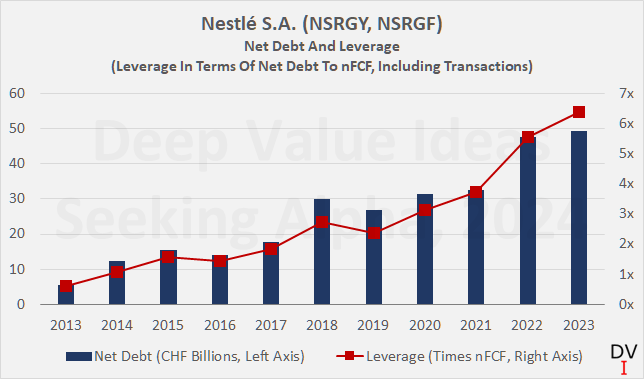

Determine 6 reveals Nestlé’s web debt since 2013 (blue bars, excluding working lease obligations) and the leverage ratio by way of web debt to normalized free money movement, together with transaction-related money flows as in Determine 3 (crimson line). Since 2013, web debt has risen from CHF 5.4 billion to virtually CHF 50 billion – a rise by greater than 9 occasions. In 2013, the leverage ratio was nonetheless extraordinarily comfy – as one would anticipate from a conservative and well-managed shopper items firm – and was effectively under one yr of normalized free money movement. By 2023, this ratio elevated to greater than six occasions free money movement.

Determine 6: Nestlé S.A. (NSRGY, NSRGF): Web debt, excluding working lease obligations, and leverage by way of web debt to normalized free money movement (personal work, primarily based on firm filings)

In fact, such a stage of leverage remains to be manageable for a shopper items firm attributable to its low cyclicality and pretty dependable money movement. Nevertheless, given the present rate of interest atmosphere, I think about the sharp improve in web debt in 2022 (+ CHF 15.0 billion) and 2023 (+ CHF 1.8 billion) not precisely prudent, additionally realizing that share repurchases over this era totaled CHF 15.9 billion. The sharp improve in debt can be mirrored in Nestlé’s gross curiosity expense, which has virtually doubled within the final three years (CHF 1.33 billion in 2023 in comparison with CHF 0.75 billion in 2021).

I used to be considerably stunned that the ranking company Moody’s maintained the secure outlook on Nestlé’s Aa2 issuer ranking in its last report in October 2022 – particularly in mild of the truth that the ranking was downgraded in 2019, partially in response to the introduced CHF 20 billion buyback program and consequently larger tolerance for leverage.

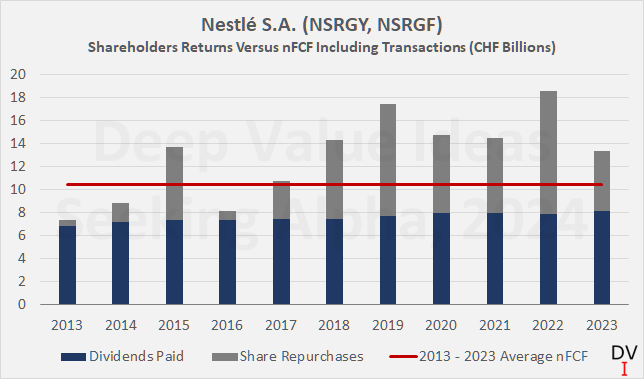

Talking of which, I personally assume Nestlé’s stance on money returns to shareholders will not be sustainable, even perhaps irresponsible. Since 2013, the corporate has paid CHF 79.6 billion in dividends, which in itself will not be an issue contemplating that free money movement together with the web impact from acquisitions and divestitures amounted to CHF 115 billion. Nevertheless, over the identical interval, shares had been repurchased for CHF 58.4 billion, that means that Nestlé has returned 24% (or CHF 27.1 billion) extra cash to shareholders than it has generated during the last eleven years (Determine 7).

Determine 7: Nestlé S.A. (NSRGY, NSRGF): Money returns to shareholders versus common annual normalized free money movement, together with transaction-related money flows (personal work, primarily based on firm filings)

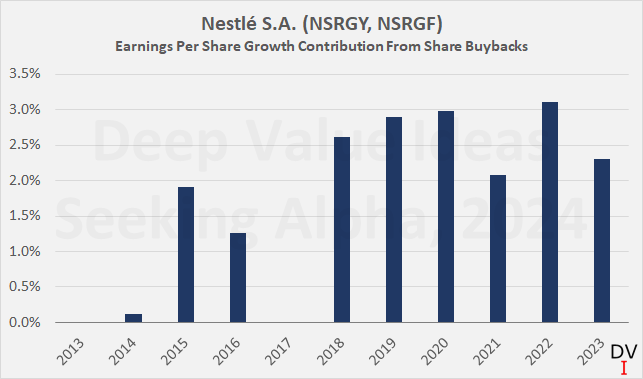

Based mostly on the variety of shares excellent, we will calculate the contribution of share buybacks to earnings per share (EPS, and all different per share metrics) development, as proven in Determine 8. Over the past eleven years, EPS development attributable to share buybacks – virtually half of which had been funded by debt – has averaged 1.9% per yr, and it’s discouraging to see that the contribution has clearly elevated because the late 2010s (2018-2023 common 2.7%). Adjusted EPS development averaged 5.3% within the interval 2018-2023.

Determine 8: Nestlé S.A. (NSRGY, NSRGF): Earnings per share development contribution from share buybacks (personal work, primarily based on firm filings)

A Excessive Valuation – Regardless of The Drop In Nestle Share Worth

It could possibly be argued that the numerous decline within the share value since 2021 is essentially because of the points described above. A price-to-earnings ratio of effectively under 20 is certainly comparatively low cost for a blue-chip shopper items firm with a world-class model portfolio.

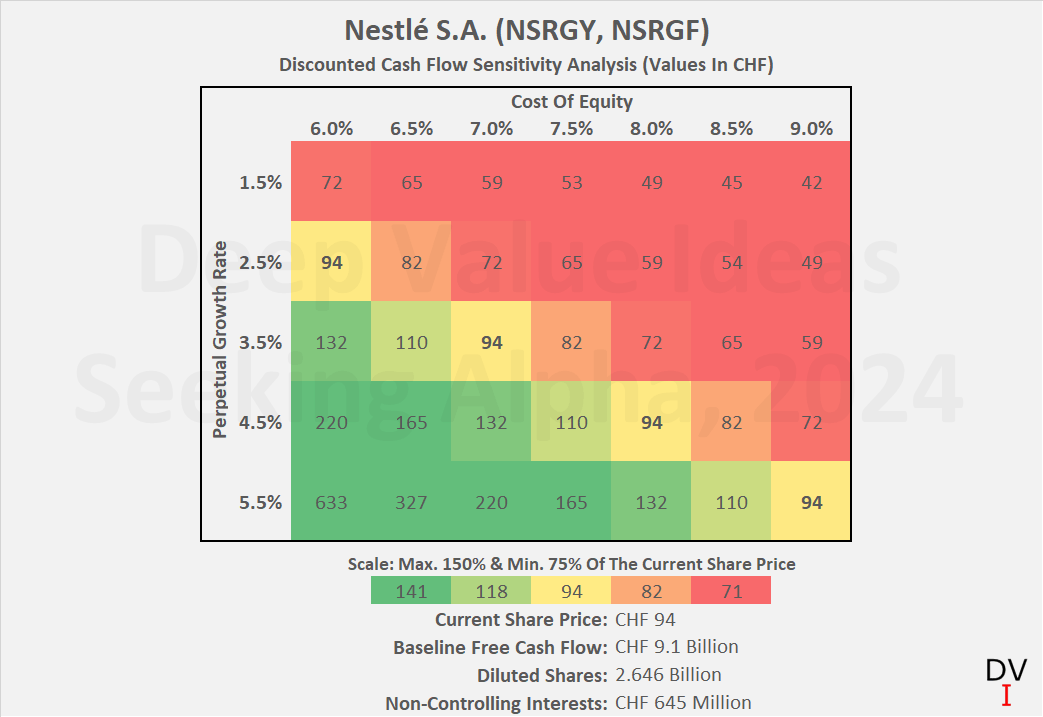

Nevertheless, it is very important remember that the abovementioned P/E ratio is predicated on Nestlé’s adjusted EPS. Given the numerous and recurring impairment costs, in addition to the more and more poor working capital administration and extra money margin, I consider it’s prudent to worth the inventory primarily based on a reduced money movement (DCF) evaluation – in spite of everything, it’s free money movement that’s the lifeblood of long-term shareholder returns.

Nestlé’s three-year common nFCF, together with transaction-related money flows, is CHF 9.1 billion. For the DCF analyses, I’ve used low cost charges starting from 6.0% to 9.0%. For a well-established shopper items firm, a relatively low low cost fee is cheap, however I think about something under 7.0% to be too low an anticipated return. In keeping with Determine 9, Nestlé’s free money movement must develop by 3.5% each year in perpetuity for the inventory to be pretty valued at current. 3.5% does not sound like a lot development, however keep in mind the infamous sensitivity of DCF evaluation to the expansion fee and the importance of terminal worth (i.e., money flows far out sooner or later).

Determine 9: Nestlé S.A. (NSRGY, NSRGF): Discounted money movement sensitivity evaluation (personal work)

For my part, will probably be tough to realize such development, particularly given Nestlé’s already substantial measurement (solely acquisitions of enormous and due to this fact usually costly manufacturers transfer the needle) and closely leveraged stability sheet. If Nestlé’s free money movement continues to tread water and the corporate is unable to return to development (i.e., a perpetual development of 0.0%), the inventory could be value CHF 46 – or roughly half of its present value – at a value of fairness of seven.0%.

Conclusion: Why I Keep away from Nestlé Inventory Regardless of Its “Safe Haven” Standing And Seemingly Favorable Valuation

There is no such thing as a denying that Nestlé owns a lot of iconic and really well-known shopper items manufacturers. Its measurement, its model portfolio and its worldwide publicity – particularly in rising markets – qualify the corporate as a strong funding for reasonably risk-averse traders, no less than in idea. There are a number of facets which, in my view, make Nestlé shares uninvestable at current.

First, free money movement did not develop for no less than the final ten years, each when excluding and together with money flows associated to acquisitions, divestitures and three way partnership investments. To some extent, this is because of generally weaker than anticipated model efficiency, as evidenced by the numerous impairment costs on intangible belongings (Nestlé has written off CHF 13.6 billion since 2013). Nevertheless, the corporate’s working capital administration must also be highlighted on this context. The rise in days gross sales excellent and stock days, in addition to decline in days payables excellent can’t be solely attributed to the provision chain points following the pandemic.

Secondly, Nestlé’s stability sheet high quality has deteriorated considerably. Web debt has elevated greater than ninefold since 2013, when the leverage ratio was nonetheless very modest at 0.6 occasions normalized free money movement for the yr. In 2023, the leverage ratio was greater than six occasions nFCF. One can argue {that a} well-established and internationally diversified shopper items big can address such a leverage ratio, however I believe the historic improvement of web debt is unquestionably fairly telling.

Thirdly, shareholder returns (dividends and share buybacks) had been partly financed with debt. This in itself will not be a serious problem, however within the context of basically stagnant free money movement, I believe this coverage is sort of irresponsible. Whereas it is just a speculation, the truth that Nestlé’s administration has elevated its give attention to share buybacks in recent times could possibly be a sign that the dearth of inner development is no less than partially compensated with share buybacks – in spite of everything, share buybacks have contributed a median of two.7 share factors to earnings per share development since 2018.

As a worth investor, I naturally gravitate to shares which are “on sale” – which is unquestionably the case with Nestlé inventory, which is now down 25% from its all-time excessive. Admittedly, the continuing promoting stress has piqued my curiosity.

Nevertheless, I discover Nestlé S.A.’s mixture of basically flat free money movement, poor working capital administration, a extremely leveraged stability sheet, a administration group that appears vulnerable to overpaying for acquisitions and fascinating in (partially) debt-funded share buybacks, and a valuation that’s nonetheless fairly excessive from a DCF perspective, effectively, uninspiring. In consequence, I’m not occupied with including Nestlé to my fairness portfolio.

Thanks very a lot for studying my newest article. Whether or not you agree or disagree with my conclusions, I at all times welcome your opinion and suggestions within the feedback under. And if there’s something I ought to enhance or develop on in future articles, drop me a line as effectively. As at all times, please think about this text solely as a primary step in your due diligence.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.