J Studios/DigitalVision through Getty Pictures

Introduction

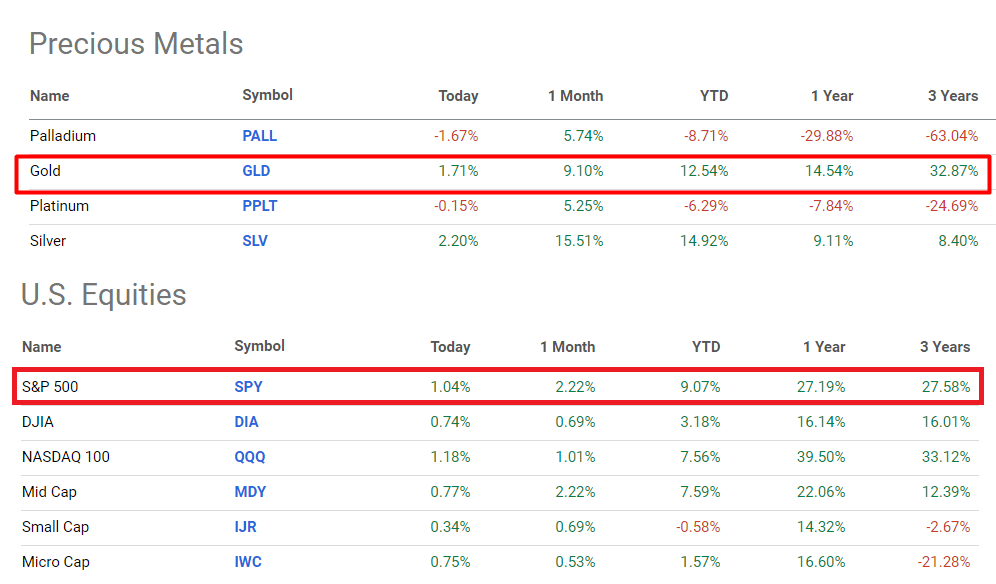

current market tendencies, it’s straightforward to miss the truth that the value of gold has instantly shot up after a few years of stagnation and has outperformed the majority of different property over the previous few months:

Searching for Alpha, writer’s notes

There is perhaps numerous arguments why the gold goes up a lot:

- expectations of elevated authorities spending, exemplified by the Biden administration’s proposed $7.3 trillion budget for fiscal 2025;

- a better willingness from central banks to tolerate larger inflation;

- favorable monetary circumstances (peaking Fed’s tightening).

Regardless of the purpose, the gold worth might rise additional to $2,600 per ounce if long-term actual rates of interest proceed to weaken, write the analysts at Jefferies of their newest observe (proprietary supply). However additionally they add that there are issues concerning the working outlook for gold miners, together with doubts about mission spending, operational execution, and geopolitical dangers. Furthermore, some buyers are skeptical about multi-year firm steerage and concern upcoming Q1 2024 outcomes. With this in thoughts, I made a decision to check out Newmont Company (NYSE:NEM) – the biggest gold mining firm on this planet – and attempt to assess the inventory’s development prospects.

Newmont’s Latest Financials And Prospects

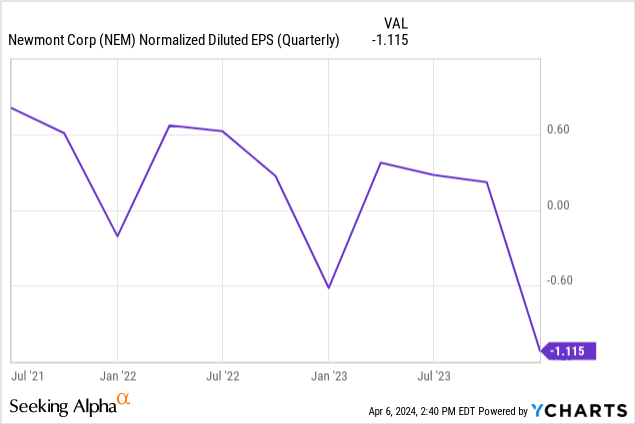

The corporate reported for its Q4 FY2023 on February 22, 2024, beating the consensus estimates each when it comes to income and EPS figures, displaying a YoY development of 23% in gross sales. Regardless of that top-line growth, Newmont remained vigilant about managing bills: Its adjusted EBITDA amounted to ~$1.4 billion whereas the margin barely narrowed to 34.9%. Therefore we see the deterioration when it comes to absolute EPS quantity:

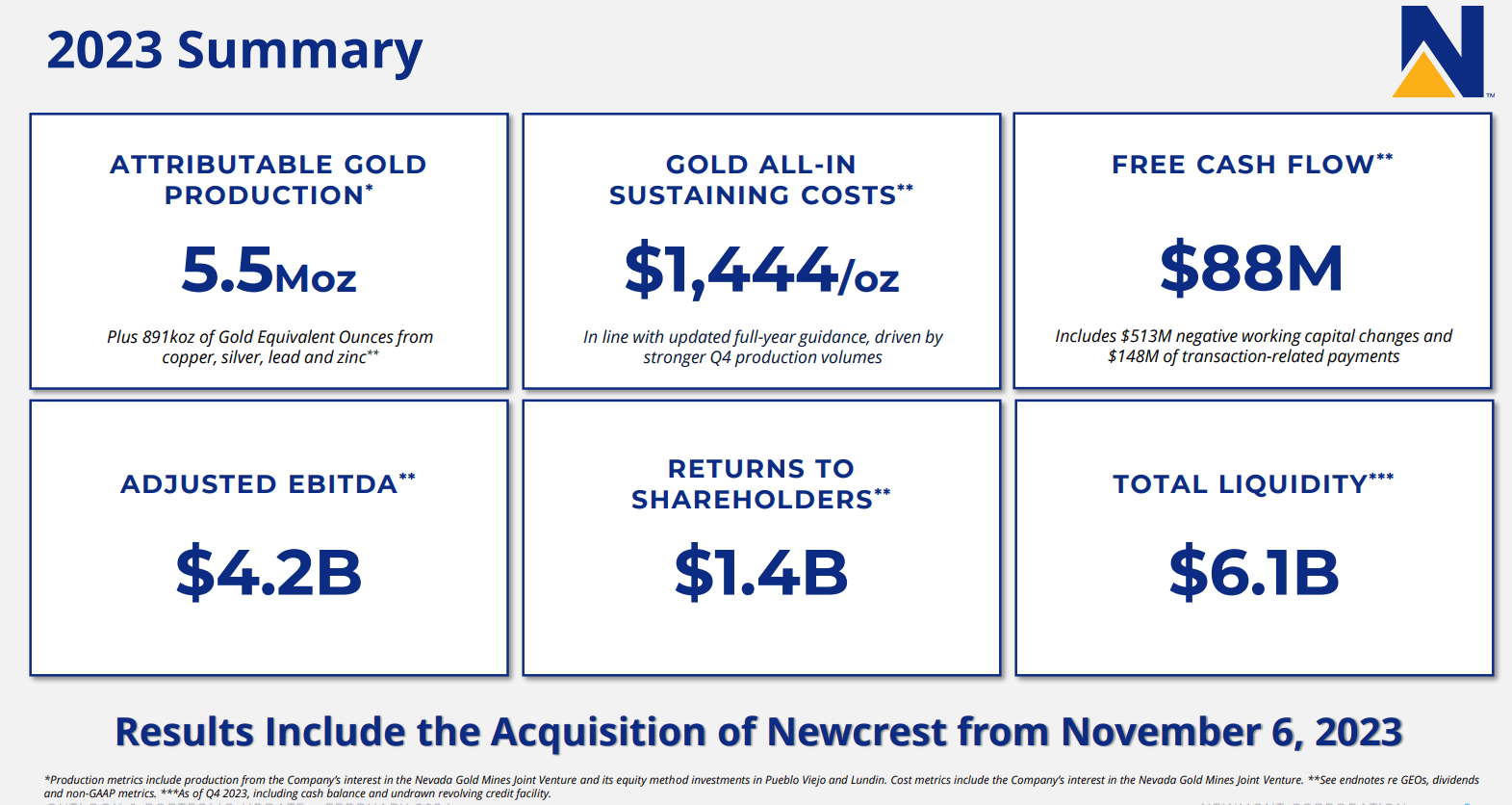

The monetary outcomes for the complete yr 2023 are fairly easy and are clearly offered to buyers in the latest IR presentation:

NEM’s IR supplies

Since NEM’s income is nearly 90% depending on promoting gold, its monetary outcomes are intently linked to tendencies in gold manufacturing and pricing. For example: according to the press release, This autumn’s income development was primarily fueled by a 7% enhance in gold manufacturing, totaling 1.74 million ounces, and in addition the uptick within the common realized gold worth reaching $2,004 per ounce (+14% YoY).

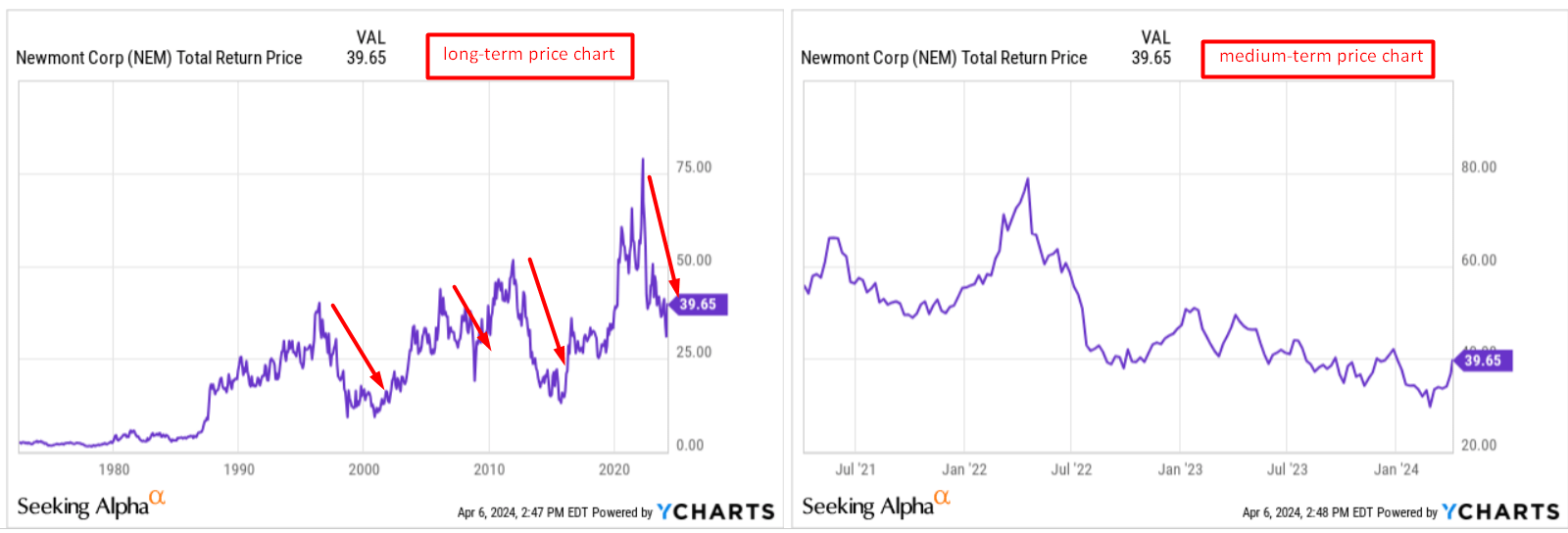

Gold stays a safe-haven asset, now buying and selling above $2,000 per ounce resulting from ongoing geopolitical tensions (Israel-Palestine, Russia-Ukraine, and so on.) and prospectively decrease U.S. rates of interest – logically, this can be a very optimistic signal for NEM. However the inventory worth reacts nearly by no means to this catalyst, if we don’t look simply on the short-term time frames (1 week – 3 months) however on the medium and long-term worth charts. From a cyclical perspective, NEM is at its native lows, as in earlier many years:

YCharts, writer’s notes

I consider that if gold costs keep above $2,000 per ounce for a while (proper now it’s heading to $2,350), Newmont ought to see higher margins as soon as operational circumstances normalize and the corporate’s enterprise improvement initiatives unfold. As a part of administration’s technique, in keeping with the latest earnings call, NEM desires to divest 6 non-core property, concentrating extra efforts on maximizing returns from its Tier 1 copper and gold tasks.

NEM’s IR supplies

Along with the synergy results of the Newcrest Mining acquisition, the CEO mentioned they plan to ship ~$500 million in annual price and productiveness enhancements by FY2025 – it is like saving nearly a complete quarter of at the moment’s working prices.

Newmont can be focusing on a $1/sh. annual base dividend and introduced a brand new $1 billion share buyback program – all of which provides as much as a dividend yield of ~2.52% and a buyback yield of ~2.18%, for a complete shareholder return of simply over 4.7%. Not dangerous, for my part.

Full-year 2024 Newmont expects to extend gold manufacturing to six.9 million ounces whereas aiming to handle prices successfully, as talked about above, forecasting a median gold worth of $1,900 per ounce for the yr. As you possibly can see, it is a lot decrease than what the gold worth has proven in current weeks. I assume that the administration staff needed to hedge their bets as a result of in keeping with the 10-Okay, the typical gold worth for FY2023 was $1,941 per ounce. However, to me, it is clear that the market is providing Newmont an opportunity for a lot stronger development than what administration initially foresaw, and even in comparison with what Wall Avenue predicted only a month in the past.

Given the top-notch high quality of the corporate’s portfolio and its international significance within the gold mining trade, I anticipate that the actions deliberate by administration to chop working prices and give attention to the core Tier 1 property will doubtless result in a major uptick in income, EBITDA, and web revenue in 2024-2025. However the inventory’s prospects also needs to rely upon the valuation. Let’s take a better look there.

Newmont Inventory’s Valuation Evaluation

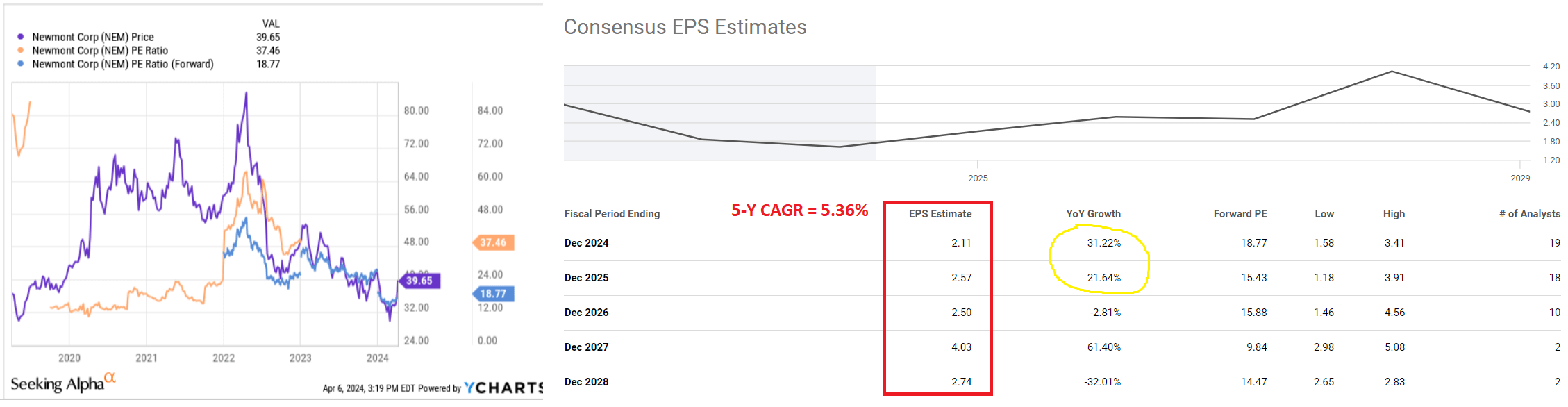

Initially, I thought-about assessing Newmont shares utilizing the normal DCF valuation mannequin, however I shortly realized that trying to foretell the value of gold 5-6 years ahead is kind of a dangerous endeavor. As a substitute, I discover it wiser to focus on the present or next-year valuation multiples and a reduction (or a premium) the market is pricing in proper now – particularly contemplating the current dynamics in gold costs and their anticipated trajectory.

YCharts, Searching for Alpha, the writer’s notes

Wanting on the firm’s TTM price-to-earnings of round 37.5x, we see that subsequent yr, Newmont is predicted to commerce at nearly 19x. This a number of contraction is predicated on the consensus view that the EPS will develop at a CAGR of 5.36% over the subsequent 5 years, whereas the majority of this development goes to return in FY2024 and FY2025 (and in addition FY2027). Whereas the general EPS momentum might seem considerably unstable, the consensus for this yr and subsequent could also be near the reality as 19-18 analysts type the consensus.

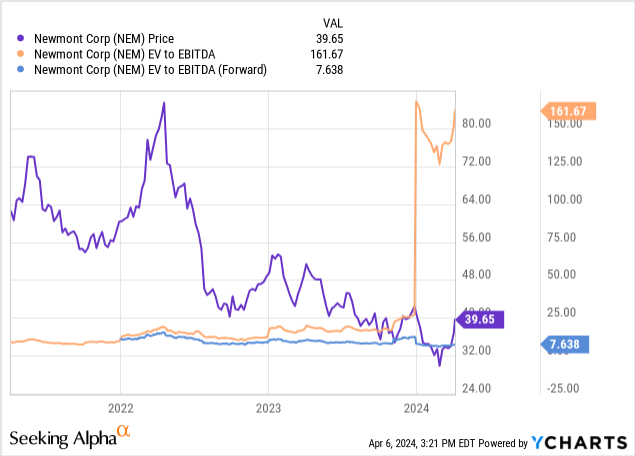

An identical image emerges based mostly on different multiples – under is the instance for TTM and FWD EV/EBITDA:

So, what does this imply for my part? In the long run, the corporate’s EPS ought to develop by over 5% yearly based mostly on the consensus information. Keep in mind, the administration plans to reward buyers via dividends and buybacks at ~4.7% in 2024. Wanting on the historic chart of the place the corporate’s P/E a number of sometimes resides, it appears to hit an area backside proper now (much like what we have seen in 2020 or 2021). Contemplating all this enter information, it seems to me that Newmont inventory is presently undervalued. I estimate a good a number of at ~25x by the tip of 2024, which leads me to consider that Newmont’s inventory might attain round $52.75 in a matter of months, assuming the present consensus of $2.11 in EPS for FY2024 holds true. This means a possible upside for NEM of ~33%, not factoring within the dividend and buyback yields (so the general investor return might surpass 35%). Nevertheless, this development potential will solely stay, in my view, if administration succeeds in turning its price administration plans into actuality and the gold worth has sufficient energy to remain above $2,000 per ounce. Right here lies the danger, amongst many others.

The place Can I Be Fallacious?

One threat to my conclusions is tied to the value of gold – it is evident from the chart under that the present worth is kind of overheated (check out the RSI indicator). We could also be on the verge of a correction, and the period of this correction stays unsure.

Supply: Refinitiv [shared by the TME newsletter]![Source: Refinitiv [shared by the TME newsletter]](https://static.seekingalpha.com/uploads/2024/4/6/49513514-17124326129178503_origin.png)

Moreover, whereas the market has been factoring in fewer charge cuts this yr, as I discussed in my recent macro article, any shift in expectations concerning charge cuts might probably impression the motion of gold.

One other important threat lies in administration’s capability to successfully steer the present state of affairs in a optimistic route. By this, I imply specifically the plan to cut back working prices, which is to be applied by 2025. If Newmont’s margins do not enhance as I anticipate at the moment, there’s a risk that the inventory worth will stagnate and even fall additional.

Abstract Thesis

Regardless of the myriad dangers surrounding Newmont at the moment, I firmly consider that the corporate has nice prospects and its inventory is just too undervalued to disregard. All of us perceive that Newmont Company embodies a cyclical narrative. I feel that at the moment, numerous macro, trade, and idiosyncratic elements counsel that the cycle for Newmont is as soon as once more turning bullish. Contemplating that the corporate’s shares are buying and selling at solely 15-18 instances forwarding web earnings, I consider we are able to deem them as cheap. Anticipating development in web earnings over the subsequent couple of years, I assign a “Buy” score at the moment.

Thanks for studying!