jurgenfr

This was a troublesome 12 months for hashish shares! Whereas some have rallied, most have declined. Shares which have appeared low cost have gotten cheaper. One which I actually like, Organigram (NASDAQ:OGI), was down so much in 2023, however it has rallied since I final wrote about it in October. I known as it a great stock for value investors, and it stays so regardless of rallying 14% since then. Right now, I clarify why I nonetheless just like the inventory a lot.

This fall Outcomes

Organigram’s fiscal 12 months ending date has modified from August to September, and the This fall that it reported in December was a four-month quarter in a thirteen-month 12 months. The corporate reported This fall on December nineteenth, and the income of C$46.0 million was effectively forward of the consensus. Adjusted EBITDA, although, was weaker than anticipated at -C$2.4 million.

The 13-month fiscal 12 months had internet income of C$161.6 million, which rose 11% from FY22. Adjusted EBITDA for the fiscal 12 months improved from C$3.5 million to C$6 million. Money movement from operations was -C$17 million in This fall and -C$38.8 million for the whole fiscal 12 months, barely worse than in FY22. The stability sheet remained very sturdy, with money and short-term investments of C$33.9 million. Tangible e-book worth ended the fiscal 12 months at C$261 million (C$3.13 per share).

The Outlook

The outlook fell after the This fall report. For FY24, 7 analysts, in response to Sentieo, predict income of C$165 million with adjusted EBITDA of C$6 million. The income estimate is barely greater than after I wrote in regards to the firm in October, whereas the adjusted EBITDA was then anticipated to be C$13 million. For FY25, 5 analysts anticipate income will enhance to C$187 million with adjusted EBITDA of C$14 million. In October, 3 analysts have been on the lookout for income of C$198 million with adjusted EBITDA of C$22 million. Whereas the projections are decrease, the corporate continues to be rising.

A Bigger Funding by BAT

I discussed within the final article that British American Tobacco (BTI), which owns nearly 20% of the corporate, may presumably purchase the remainder of the corporate. BTI fell wanting this, however it’s within the technique of paying a excessive worth for a bigger stake. This was first introduced on November sixth, only a few weeks after I shared that article.

BTI shall be shopping for C$124.6 million at C$3.22, which is an 87% premium to the present worth of C$1.72. The cash shall be invested in three tranches between January and August. Organigram shareholders have a gathering scheduled for January 18th to approve the transaction, which is able to give BTI about 45% possession.

Nearly all of the BTI funding will fund the Jupiter Strategic Funding Pool that may assist speed up OGI’s development. C$41.5 million of the funding shall be for basic company functions.

Whereas this looks as if an incredible transfer for the corporate to promote inventory to a powerful accomplice at an enormous premium, the transfer left the corporate as an impartial one. It might have labored out higher had BTI purchased the whole firm!

Valuation

In my October piece, I shared a goal a 12 months out of $2.75, which was so much greater than the worth then. I additionally famous that the price-to-tangible e-book worth was approach too low at simply 0.45X. By this metric, the inventory has gotten just a little costlier, buying and selling now at 0.55X as a result of greater worth and the decrease tangible e-book worth. I feel that that is approach too low. I feel that BTI did too! BTI is shopping for in at a slight premium to tangible e-book worth.

Adjusting my outlook for the decrease anticipated leads to FY25, I’m lowering my goal considerably. I used to be utilizing a better adjusted EBITDA than the analyst forecast (a 15% margin), and the present projection is simply 7.2% margin. My goal is predicated upon 12X projected adjusted EBITDA for the enterprise worth, and I’m utilizing a barely greater adjusted EBITDA for 2025 of C$18.7 million, a ten% margin. This works out to C$2.65 or US$2.00, which is 53% greater.

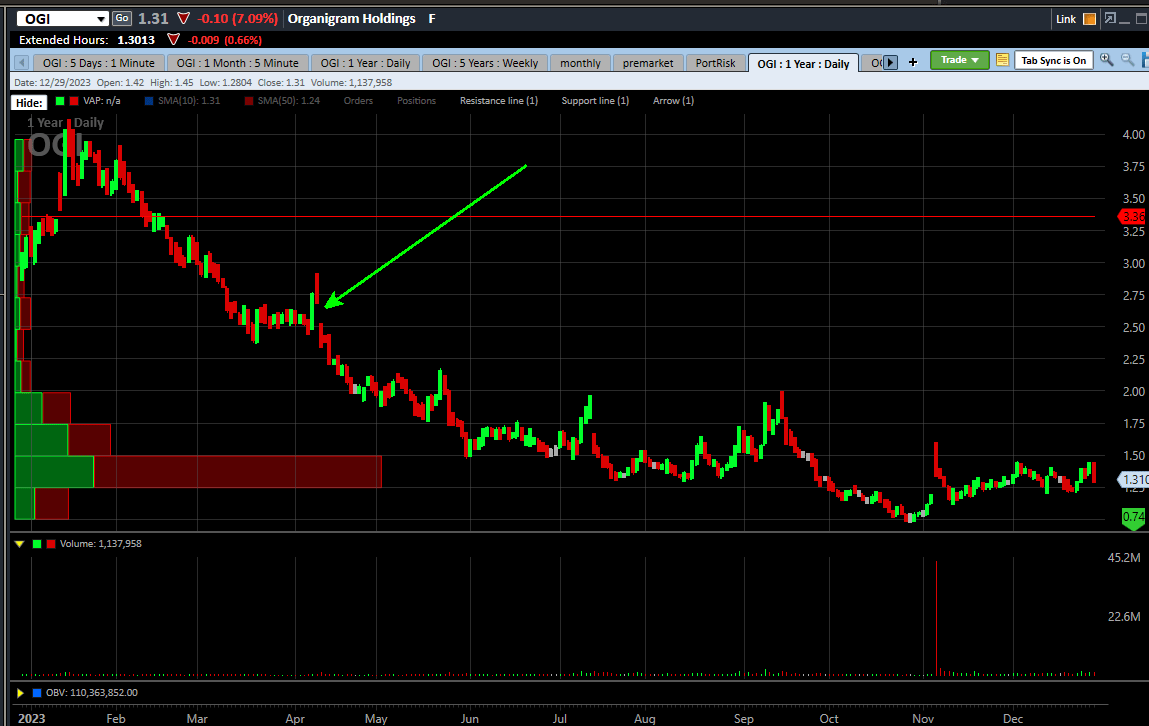

The Chart

OGI dropped 59.1% in 2023, which was much more than the NCV World Hashish Inventory fell. It gapped up on the BTI funding announcement, however it shortly pulled again. That certain was a number of quantity that day!

Charles Schwab

I might anticipate that the inventory has bottomed just under $1. It did commerce a really very long time in the past at a lower cost than the latest low. To me, this seems like a bottoming inventory. That open hole is above my one-year goal, however I feel that it is very potential the inventory may fill it.

Dangers

I view this inventory as much less dangerous than most hashish shares given its very sturdy stability sheet and market place, however, as I discussed within the final article, there are a number of dangers. The corporate could not ever adapt to have the ability to enter the American hashish market effectively. The markets that it operates in are primarily Canada, but additionally Israel, Australia and shortly Germany and the UK. Canada has been and will stay a really difficult market. Lastly, whereas it is good to see a number of money and no debt, the corporate may spend it poorly on acquisitions.

Conclusion

I like Organigram so much. The place is about 20% of my mannequin portfolio Beat the World Hashish Inventory Index, which was down a bit lower than the index in 2023. It is my largest place, however I’ve a number of others which might be massive too. I like that BTI is shopping for extra at an enormous premium and may proceed to be a superb accomplice. The inventory could be very low cost close to 55% of tangible e-book worth and will do very effectively sooner or later.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.