sturti

Eli Lilly and Firm (LLY) needs to acquire POINT Biopharma International Inc. (NASDAQ:PNT). It has an excellent tender provide for $12.5/share. When Lilly made the tender provide, it got here at a 87% premium to the market worth. The pharma has extended the tender a number of instances, with out getting many takers. In the meantime, PNT is buying and selling round $12.45. That is inside $0.05 of the take-out worth, whereas the tender might wrap-up by 22 December or get prolonged as soon as extra.

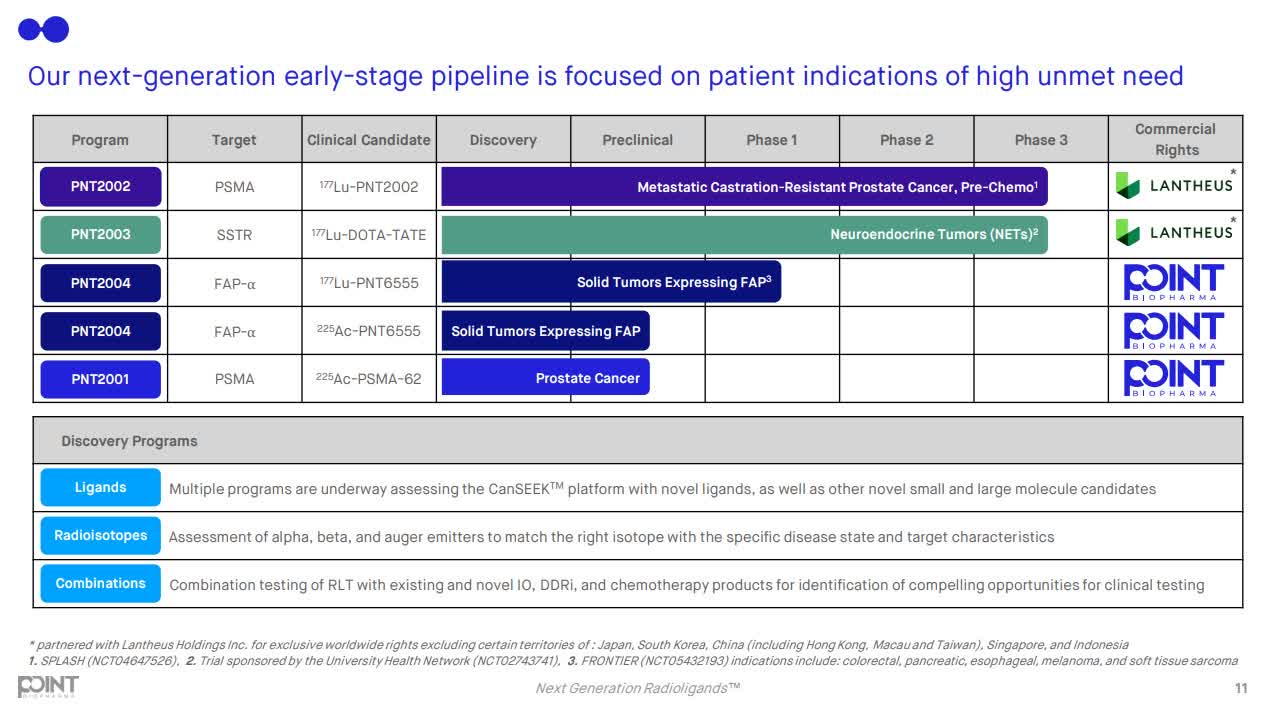

PNT reported key trial results (a section 3 prime line readout) for its most vital asset PNT2002 this month! The corporate solely has one different phase 3 asset.

pipeline level biopharma (Level Biopharma)

Most of its $1.3 billion market cap hinges on these stage 3 property, though the corporate does have a strong $300 million+ in cash. PNT is a radiopharmaceutical firm, and my impression is that that is at the moment a desirable niche in early-stage biotech.

From the best way the deal is structured, the truth that due diligence has been carried out, the Lantheus commercialization is in place, and the awkward timing of the tender provide, I get the impression Lilly is shopping for this for infrastructure/platform worth. This readout is probably going not key to the customer.

Eli-Lilly initially screwed itself a bit bit right here as a result of if this end result will get reported and it’s horrible, it stays on the hook for the tender at $12.50. In the meantime, a constructive end result might have drawn in different bidders and pressure it to up its provide. The market seems to take the superficially profitable readout as disappointing. Shareholders kind of have a put right here (at Lilly’s expense) and solely upside. On condition that key trial readouts might have led to explosive outcomes, this was a beautiful present. The market had been profiting from this by bidding up the share worth. Now, mega-upside is off the desk, and actuality units in that Lilly can stroll in some unspecified time in the future and the put is eliminated. Lilly solely has one necessary extension remaining (I estimate that it will final till the top of the 12 months), after which they will stroll away.

The corporate took this $12.50 deal as an alternative of a lot riskier offers with very heavy units of contingencies from one other bidder. That bidder put forth two proposals that had been each very sophisticated and conditional (which was the explanation the corporate did not settle for them). From the 14D-9:

…On September 27, 2023, Firm B despatched POINT two various revised proposals to amass the entire excellent Shares of POINT (the “September 27 Proposals”). The primary proposal didn’t embrace the SPLASH Learn-Out Situation, and was for an mixture of as much as $20.00 per Share in money, inventory and contingent worth rights, payable as follows: (1) $8.50 per Share in money and inventory payable at closing; (2) if the outcomes of the top-line main evaluation of the SPLASH Scientific Trial happy a proposed “base” case of detailed pre-defined standards, an extra $4.50 per Share in money and inventory payable at closing and a contingent worth proper of $3.00 per Share in money or inventory payable upon regulatory approval; (3) if the outcomes of the top-line main evaluation of the SPLASH Scientific Trial happy a proposed “upside” case of detailed pre-defined standards, an extra $7.50 per Share in money and inventory payable at closing; and (4) two $2.00 per Share contingent worth rights tied to internet gross sales, payable in money or inventory, at Firm B’s election (the “First September 27 Proposal”).

and

…The second proposal included the SPLASH Learn-Out Situation, and was for an mixture of as much as $20.00 per Share in money, inventory and contingent worth rights, payable as follows: (1) $13.00 per Share in money and inventory payable at closing, offered POINT met the SPLASH Learn-Out Situation; (2) if the outcomes of the top-line main evaluation of the SPLASH Scientific Trial happy a proposed “upside” case of detailed pre-defined standards, an extra $3.00 per Share in money and inventory payable at closing; and (3) two $2.00 per Share contingent worth rights tied to internet gross sales, payable in money or inventory at Firm B’s election (the “Second September 27 Proposal”). The September 27 Proposals would lead to POINT’s stockholders proudly owning an mixture of between roughly 6.3% and roughly 12.3% of Firm B. The September 27 Proposals additionally indicated that Firm B would add one POINT director of Firm B’s selecting to the Firm B Board of Administrators. The September 27 Proposals indicated that the proposed transaction wouldn’t require Firm B’s stockholders’ approval or be contingent on Firm B’s skill to acquire financing. The September 27 Proposals didn’t request exclusivity.

Unusually, the second of those proposals began at $13 per share in money and inventory. After that, it says loads of different stuff that is supposed so as to add as much as one other $7 of worth. I get that $13 in money and inventory is not the identical factor as $12.50 in money. And, after all, there may be already the read-out situation proper there, however $20 is nearly 60% greater than $12.50. It’s a large distinction. The corporate has loads of money, so there isn’t any imminent financing want…. Why take the $12.50 proper forward of the readout?

Moreover, the corporate has already bought the licensing rights to its two most superior property to Lantheus Holdings (LNTH). I am scratching my head why the 2nd bidder can be tying all these situations to the PNT 2002 and 2003 readout. I would not be shocked if that bidder really was Lantheus.

But when any bidder tied sufficient situations to the readout of PNT 2002, it’s getting a wonderful deal, as a result of Lantheus is paying as much as $1.8 billion in regulatory and gross sales milestones associated to PNT 2002 and PNT 2003. The corporate additionally nonetheless has a royalty reduce. Bear in mind, one other $300 million of money can be on the steadiness sheet. Should you put sufficient situations in place, you may nearly purchase the corporate with Lantheus’ cash. Maybe that is what Lantheus was desirous about doing right here.

One analyst noticed a 60% chance of constructive outcomes from the December readout. That turned out appropriate. That very same analyst noticed the inventory getting despatched to the mid-20s on the readout as a result of PNT nonetheless has a 25% royalty charge on gross sales. In that sense, this has been a disappointment. Nonetheless, a share of the $1.8 billion milestone, in addition to royalty income, is now one step nearer.

It’s a unusual and complicated scenario. On the finish of the day, the widespread does seem like a pretty danger/reward even with little or no upside. As we’re getting very near the top of December, Eli-Lilly will quickly have the choice of strolling from the tender. If Eli-Lilly walks, that is a catastrophe. As that risk nears, the place of traders turns into way more not sure. LLY is not prone to say something to mitigate considerations, as a result of it is that uncertainty that might make its tender work.

May that 2nd bidder come again now that theoretically constructive outcomes are out? What are the percentages we’ll see a slight bump out of LLY? What are the percentages, that shareholders are nonetheless going to carry out after the disappointing readout? I feel it is rather unlikely shareholders will nonetheless maintain out. I feel they will tender en masse. I do not assume the percentages are excessive that the 2nd bidder is coming again.

Nevertheless, at $12.45 the corporate might be a purchase and a minimum of a maintain. The POINT Biopharma International Inc. upside is nearly 0.40%. Doubtlessly, that is generated inside 1-2 weeks. The percentages of a bump or a 2nd bidder re-emerging have decreased vastly, however they are not zero.