Boy Wirat

By Brian Manby

Over the previous two years, rising rates of interest reversed a number of longstanding market relationships so considerably that they defy historic precedent.

Essentially the most damning proof is discovered within the fairness market, the place newly constructive correlations between inventory and bond returns get rid of the diversification profit that existed when the historic relationship was persistently destructive. The market commentary has rightfully targeted on this, because it newly challenges the conventions of portfolio development.

However different relationships have been upended as nicely.

Over the past 20 years, equities maintained steadily constructive correlations with modifications in U.S. Treasury yields, as regular financial progress propelled fairness markets increased and offered upward, but not prohibitive, stress on charges. This development was exacerbated by the very nature of a low-interest charge atmosphere since yield modifications from one interval to the subsequent contained an upward bias.

Although it fluctuated all through the financial cycle, the connection remained persistently constructive for each massive caps and small caps. The development was constant throughout all 9 U.S. fairness measurement and magnificence combos as nicely, with small caps and worth kinds sustaining barely stronger relationships than massive caps and progress.

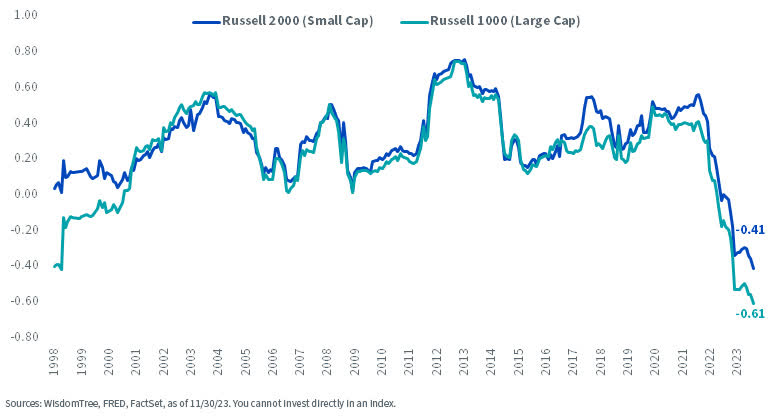

Median Rolling 36M Correlation of Russell U.S. Index Household vs. 10-12 months Treasury Yield (since 2005)

Nevertheless, after greater than 500 foundation factors of cumulative charge hikes over the previous two years, the connection started to interrupt down in late 2021. Two years later, large- and small-cap equities are actually deeply negatively correlated with modifications in rates of interest for the primary time in our 25-year knowledge historical past.

Rolling 36M Correlation: Massive Cap & Small Cap Returns vs. Modifications in 10-12 months U.S. Treasury Yield

Regardless of the shift, these correlations could recommend a near-term upside for equities within the prevailing rate of interest atmosphere.

Though charge hikes impeded danger sentiment and embedded most U.S. fairness indexes in destructive territory for the previous two years,1 an eventual financial coverage pivot could revitalize broader optimism. The Federal Reserve has insinuated that it plans to carry rates of interest regular over the close to time period and that its subsequent coverage charge resolution is could doubtless be a charge reduce versus one other hike, offered there are not any constructive financial surprises that disrupt the current development of softening knowledge.

Meaning markets are doubtless atop the rate of interest plateau and eagerly await the descent. As soon as the pivot to coverage easing commences, we predict a contemporary injection of danger urge for food might be swift and pronounced.

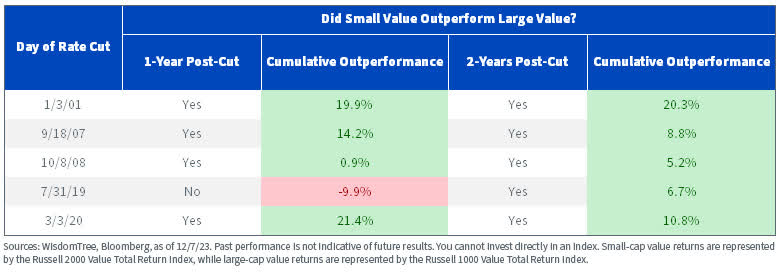

In that situation, we surmise that conventional risk-on darlings like small-cap equities could catch an overdue tailwind. Small-cap worth, particularly, has a powerful document of outperformance over large-cap worth as soon as the FOMC initially pivots to accommodative coverage.

Over the previous 20 years, the Fed reduce charges after extended durations of excessive, or regular, charges on 5 events. Through the one- and two-year durations following these reductions, small-cap worth outperformed large-cap worth in 9 of ten observations to a compelling extent.

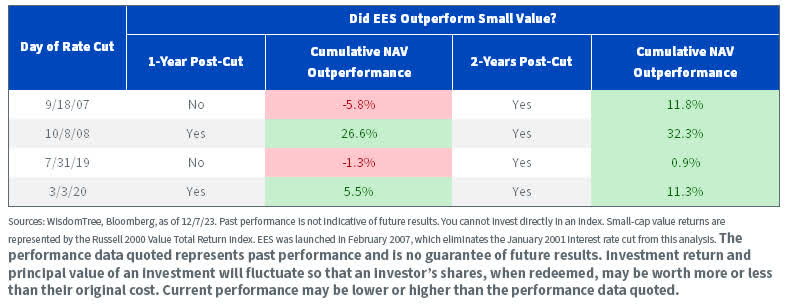

The WisdomTree U.S. SmallCap Fund (EES) recorded even higher success over the latter 4 cuts proven above, outperforming broad small-cap worth over the next one- and two-year durations in six of eight observations.

For the newest month-end efficiency, standardized efficiency, and 30-day standardized yield click on here.

Three of the 4 observations throughout the two-year subsequent returns additionally notched double-digit outperformance over broader small-cap worth.

It additionally trades at an analogous valuation to the broader market,2 which can create a beautiful entry level for potential allocations. It at present has 11.0 instances estimated price-to-earnings (excluding destructive earners) a number of versus 13.8 instances for the Russell 2000 and 11.4 instances for the Russell 2000 Worth.

General, we’re inspired by the historic observe document for small-cap worth within the coverage atmosphere instantly earlier than and after charge cuts and assume the WisdomTree U.S. SmallCap Fund could also be in an appropriate place to think about.

1 Supply: Bloomberg, as of 12/7/23, masking the interval 12/31/21-12/7/23.2 Sources: WisdomTree, FactSet, as of 12/7/23. You can’t make investments immediately in an index.

Vital Dangers Associated to this Article

There are dangers related to investing, together with the attainable lack of principal. Funds focusing their investments on sure sectors and/or smaller firms enhance their vulnerability to any single financial or regulatory improvement. This may occasionally lead to higher share worth volatility. Please learn the Fund’s prospectus for particular particulars relating to the Fund’s danger profile.

Brian Manby, CFA Affiliate, Funding Technique

Brian Manby joined WisdomTree in October 2018 as an Funding Technique Analyst. He’s liable for aiding within the creation and evaluation of WisdomTree’s mannequin portfolios, in addition to serving to assist the agency’s analysis efforts. Previous to becoming a member of WisdomTree, he labored for FactSet Analysis Methods, Inc. as a Senior Advisor, the place he assisted shoppers within the creation, upkeep, and assist of FactSet merchandise within the funding administration workflow. Brian acquired a B.A. as a twin main in Economics and Political Science from the College of Connecticut in 2016. He’s holder of the Chartered Monetary Analyst designation.

Editor’s Notice: The abstract bullets for this text have been chosen by In search of Alpha editors.