Justin Sullivan

Introduction

The healthcare sector is at all times attention-grabbing, particularly when there’s some uncertainty concerning non-public consumption. With increased rates of interest than a decade in the past, consumption could develop slower. Healthcare merchandise are one factor that individuals are likely to hold spending on. Subsequently, healthcare spending tends to get pleasure from a extra secure progress path than discretionary spending.

In my dividend progress portfolio, I personal a number of healthcare corporations. Some are prescription drugs, and others produce medical units. One firm that has been on my watchlist for a number of years is Gilead Sciences (NASDAQ:GILD). The corporate is a diversified pharmaceutical firm with a rising document of dividend will increase. It could be a sexy addition to my portfolio if it has sufficient progress alternatives.

Searching for Alpha’s firm overview reveals that:

Gilead Sciences discovers, develops, and commercializes medicines for unmet medical wants in the US, Europe, and internationally. The corporate gives merchandise for the remedy of HIV/AIDS, an injection for intravenous use, for the remedy of coronavirus illness 2019, and for the remedy of viral hepatitis. It additionally presents merchandise for the remedy of oncology, an oral formulation for treating pulmonary arterial hypertension, and a liposomal formulation for treating extreme invasive fungal infections.

Fundamentals

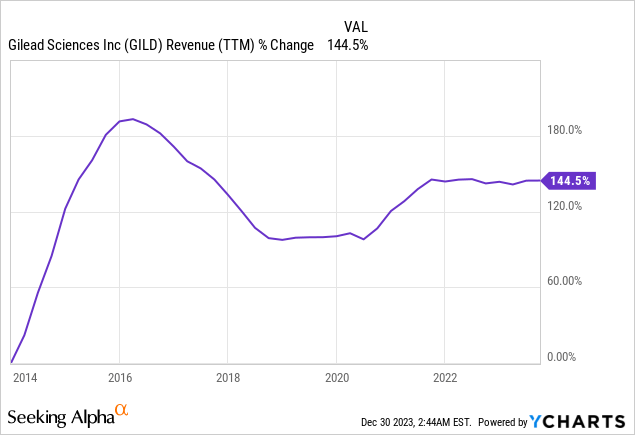

The revenues of Gilead Sciences have elevated by 145% over the past decade. The income progress might be attributed to natural and inorganic progress attributable to acquisitions. These acquisitions embrace Kite Pharma for cell remedy, Immunomedics for oncology, Forty Seven Inc. for immuno-oncology, and MYR GmbH for hepatitis delta virus, diversifying its choices and addressing unmet medical wants. Whereas the determine seems spectacular, the corporate has seen stagnated gross sales for many of the final decade, implying that it struggles to develop. Sooner or later, as seen on Searching for Alpha, the analyst consensus expects Gilead Sciences to continue to grow gross sales at an annual charge of ~2% within the medium time period.

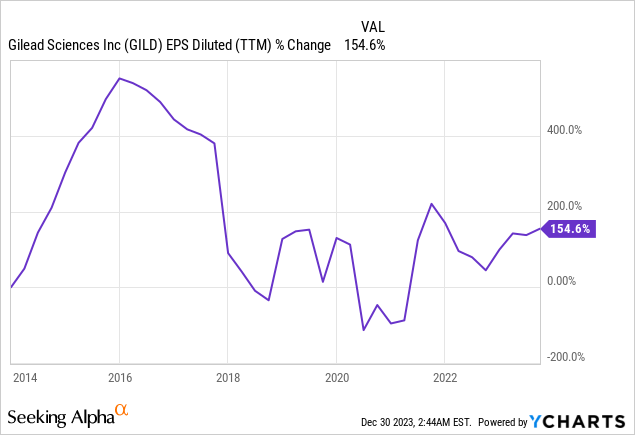

The EPS (earnings per share) has elevated by 154% over the identical interval. Throughout that decade, the corporate maintained a 40% working margin, however with the stagnating gross sales, even the aggressive buybacks weren’t sufficient to help progress. With excessive margins and vital share buybacks not sufficient to extend EPS, the corporate should improve gross sales to realize EPS progress. Sooner or later, as seen on Searching for Alpha, the analyst consensus expects Gilead Sciences to continue to grow EPS at an annual charge of ~5% within the medium time period.

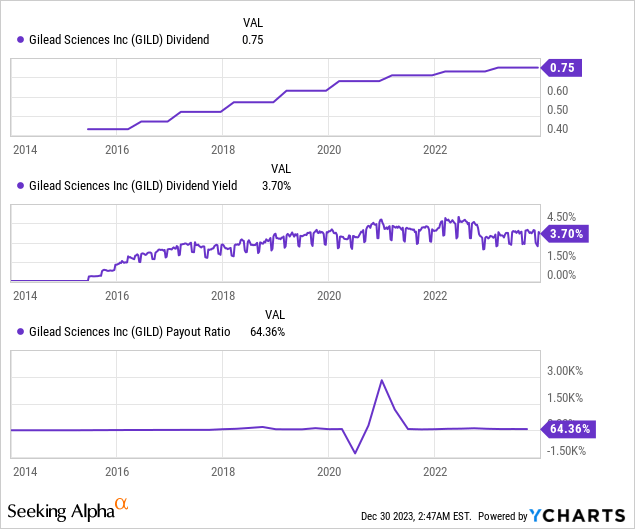

The corporate is a comparatively new dividend-paying firm. It has been paying a dividend since 2015 and has grown yearly. Whereas the dividend progress streak might not be very lengthy, it has some promising elements. The present yield is 3.7%, a comparatively excessive dividend yield for a healthcare firm. Furthermore, the dividend is probably going secure, with the payout ratio at 64% utilizing GAAP EPS and 45% utilizing non-GAAP EPS. That leaves the corporate with sufficient room to spend money on future progress prospects whereas rising the dividend in step with the EPS progress.

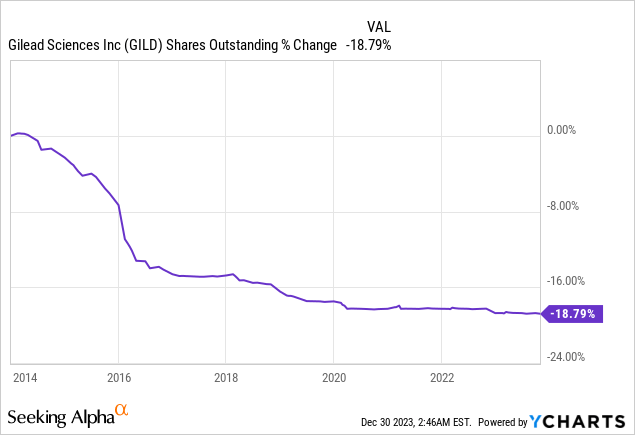

Along with dividends, the corporate returns capital to shareholders by way of buybacks. During the last decade, the corporate has been shopping for again its shares aggressively. These share repurchase packages decreased the variety of excellent shares by virtually 20% within the earlier decade. Buybacks help EPS progress as they decrease the share rely, permitting corporations to realize a better EPS with the identical web earnings. Buybacks are extremely efficient when the share value is low, however shouldn’t be used as a substitute of strategic investments.

Valuation

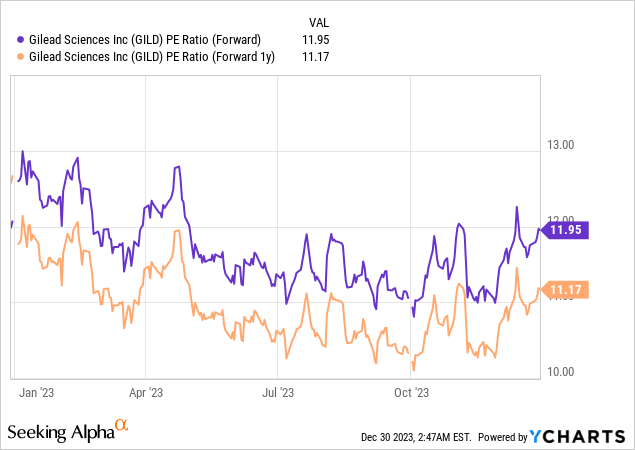

The corporate’s P/E (value to earnings) ratio stands at 11.95 when utilizing the 2023 EPS estimates and 11.17 when utilizing the 2024 EPS estimates. The present P/E ratio aligns with the valuation we have now seen over the past decade. Whereas the valuation appears engaging, traders ought to keep in mind the stagnation that the corporate has been coping with. If it manages to search out its progress path, the valuation is engaging. Till then, I consider it’s a truthful valuation.

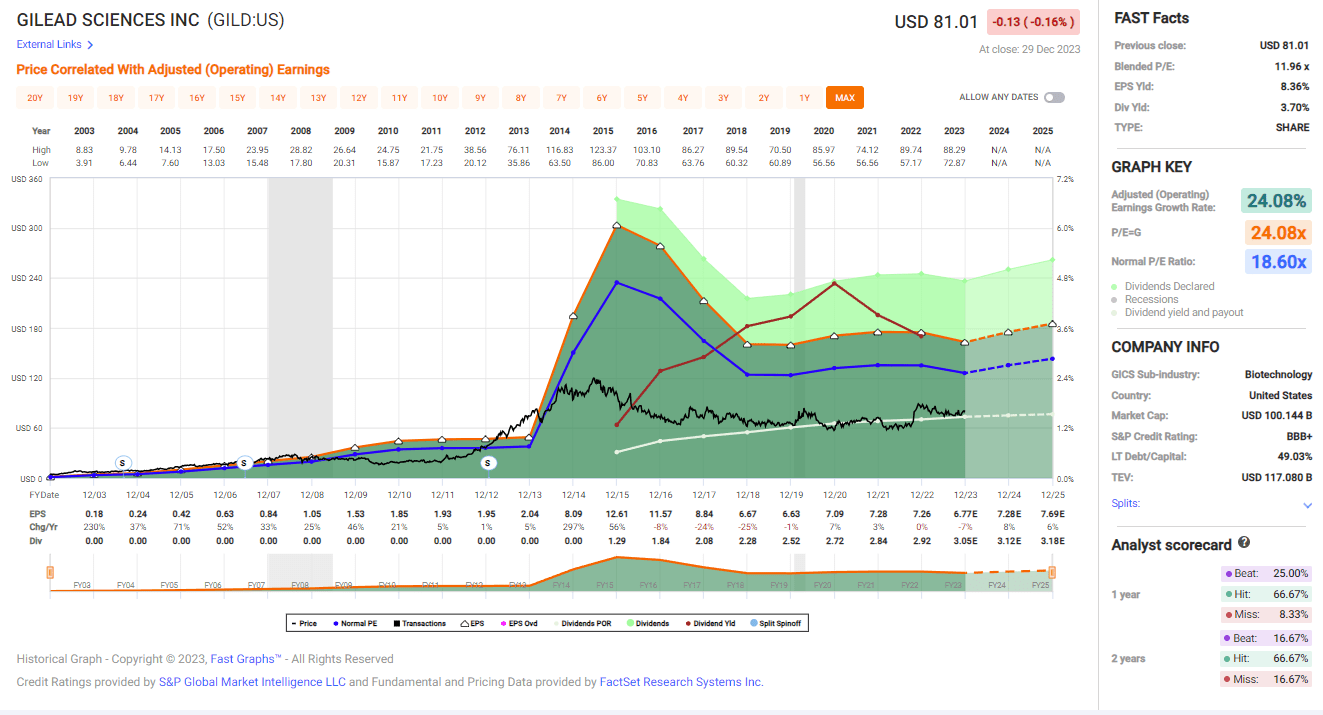

The graph under from Quick Graphs additionally reveals that the corporate is pretty valued. During the last 20 years, the typical P/E ratio of the corporate has been 18.6, a a lot increased P/E ratio in comparison with the present one. On the similar time, the typical progress charge was 24% yearly, a a lot increased progress charge than the forecasted 5%. Subsequently, it seems just like the share value is on the lookout for route. The corporate trades at a decrease valuation with a decrease progress charge, and I consider it’s pretty valued.

Quick Graphs

Alternatives

Probably the most distinguished progress alternative is the enlargement of the oncology portfolio. Gilead’s oncology phase continues to drive progress, with a 33% improve in gross sales within the third quarter, reaching an annualized income of over $3 billion. Trodelvy, the TROP2-directed ADC, demonstrated strong gross sales progress of 58% YoY, now reaching $283 million. The optimistic knowledge from Trodelvy’s Part 2 EDGE-Gastric trial and its potential in first-line metastatic higher GI cancers, as introduced within the ASCO plenary session, spotlight a promising enlargement alternative within the oncology market.

“With clear momentum and a solid infrastructure in place, in addition to our compelling clinical pipeline, we look forward to providing more patients with potentially new and effective options.”

(Daniel O’Day, Chairman and Chief Govt Officer, Q3 2023 Convention Name)

One other progress alternative is the corporate’s developments in its virology packages. Gilead’s virology packages, significantly in HIV remedy and prevention, current progress alternatives. Biktarvy, a number one HIV remedy, achieved a 12% YoY gross sales improve, contributing to a 9% progress in HIV general within the first 9 months of 2023. Lenacapavir, a long-acting oral integration inhibitor, reveals promise in HIV remedy. Part 1 and a couple of trials are underway, and Part 3 trials are anticipated to share knowledge in early 2024, presumably rising future gross sales within the firm’s major enterprise phase.

“In HIV treatment, we reviewed promising data from the Phase 1 study of GS-1720 or once-weekly long-acting oral integration inhibitor to be combined with lenacapavir and Phase 2 ARTISTRY-1 trial evaluating a once-daily oral lenacapavir and bictegravir combination.”

(Daniel O’Day, Chairman and Chief Govt Officer, Q3 2023 Convention Name)

One other small alternative is the enlargement of cell remedy. Gilead’s cell remedy phase, led by the acquisition of Kite, continues to develop, with third-quarter gross sales reaching $486 million, a 22% YoY improve. Yescarta and Tecartus, Gilead’s CAR-T cell therapies, demonstrated sturdy gross sales progress. With solely about 10% of eligible second-line massive B cell lymphoma sufferers within the U.S. presently handled with cell remedy, there’s vital untapped potential for additional adoption. Nonetheless, the phase continues to be small typically.

“As cell therapies are offered and delivered to more and more patients, we are confident that Kite remains well positioned to benefit from this expansion with its differentiated overall survival data for Yescarta and industry-leading manufacturing capabilities.”

(Johanna Mercier, Chief Industrial Officer, Q3 2023 Convention Name)

Dangers

The corporate relies on Veklury, Gilead’s therapeutic possibility for hospitalized COVID-19 sufferers. It noticed variable gross sales, declining by 31% YoY within the third quarter. The efficiency is extremely depending on COVID-19-related hospitalizations, making it weak to adjustments within the pandemic panorama and potential shifts in remedy protocols. So, regardless of being a number one Covid drug, there’s a excessive stage of uncertainty. Because the pandemic is phasing out, drug gross sales will possible decline within the medium time period, hurting EPS progress.

“While the COVID environment remains ever-changing, Veklury’s performance in the third quarter further reinforces its established role as a key part of the standard of care for patients hospitalized with COVID-19.”

(Daniel O’Day, Chairman and Chief Govt Officer, Q3 2023 Convention Name)

One other danger is the market dynamics within the HIV phase, which accounts for greater than 60% of the gross sales. Though the HIV remedy market continues to develop, the favorable pricing dynamics that contributed to earlier gross sales progress are starting to normalize. The third-quarter outcomes point out a shift in channel combine affecting common realized costs. Gilead acknowledges the normalization of pricing dynamics, emphasizing the necessity for adaptability within the aggressive HIV market.

“This was evident in the third quarter where HIV sales were up 4% year-over-year to $4.7 billion, driven by higher treatment and prevention demand and higher channel inventory, partially offset by lower average realized price due to a shift in channel mix.”

(Johanna Mercier, Chief Industrial Officer, Q3 2023 Convention Name)

The final distinguished danger is extra normal and is the continuation of stagnation attributable to pipeline dangers and discontinuations. Gilead’s numerous scientific pipeline carries inherent dangers, with 27 packages in Part 2 and 19 in Part 3. The discontinuation of the magrolimab ENHANCE and ENHANCE-2 packages based mostly on futility analyses underscores the uncertainty in scientific growth. The necessity for fixed success makes it tougher to keep up progress, as the corporate should regularly substitute its earlier blockbusters to maintain progress. With out it, the present stagnation could proceed.

“As is expected with the diverse and large clinical portfolio, not all our programs will benefit patients the way we hope they will and the ENHANCE and ENHANCE-2 programs evaluating magrolimab have both been discontinued based on futility analyses.”

(Merdad Parsey, Chief Medical Officer, Q3 2023 Convention Name)

Conclusions

Gilead Sciences is a difficult firm. It has proven long-term progress in gross sales and EPS that led to a rising dividend. Nonetheless, it has additionally suffered from stagnation over the past decade. It has a number of progress alternatives in oncology and HIV primarily, however traders are proper to be involved with their execution capabilities because of the stagnation. There are dangers, however there’s additionally a margin of security within the valuation to accommodate them.

Typically, an organization rising at a single-digit progress charge buying and selling for 11 instances earnings could be a good funding. Nonetheless, the corporate has been struggling to develop for too lengthy. Subsequently, I consider that the shares of Gilead Sciences are a HOLD. I’ll discover them engaging both at a P/E ratio of 8-9 or when the corporate lastly proves that it may possibly carry stable progress in gross sales.