This week the Bank of Canada and the ECB cut rates each by 25 basis points. For each, it was the central banks initial cut.

The Bank of Canada announced their interest rate decision on Wednesday. The central bank cut from what is restrictive policy, but acknowledge further cuts are dependent on upcoming data.

BANK OF CANADA RATE STATEMENT REVIEW

- “The Bank of Canada today reduced its target for the overnight rate to 4¾%, with the Bank Rate at 5% and the deposit rate at 4¾%.”

- “The Bank is continuing its policy of balance sheet normalization.”

- “The global economy grew by about 3% in the first quarter of 2024, broadly in line with the Bank’s April Monetary Policy Report (MPR) projection.”

- “In the United States, the economy expanded more slowly than was expected, as weakness in exports and inventories weighed on activity.”

- “Growth in private domestic demand remained strong but eased.”

- “In the euro area, activity picked up in the first quarter of 2024.”

- “China’s economy was also stronger in the first quarter, buoyed by exports and industrial production, although domestic demand remained weak.”

- “Inflation in most advanced economies continues to ease, although progress towards price stability is bumpy and is proceeding at different speeds across regions.”

- “In Canada, economic growth resumed in the first quarter of 2024 after stalling in the second half of last year.”

- “At 1.7%, first-quarter GDP growth was slower than forecast in the MPR.”

- “Consumption growth was solid at about 3%, and business investment and housing activity also increased.”

- “Labour market data show businesses continue to hire, although employment has been growing at a slower pace than the working-age population.”

- “Wage pressures remain but look to be moderating gradually.”

- “Overall, recent data suggest the economy is still operating in excess supply.”

- “CPI inflation eased further in April, to 2.7%.”

- “The Bank’s preferred measures of core inflation also slowed and three-month measures suggest continued downward momentum.”

- “Indicators of the breadth of price increases across components of the CPI have moved down further and are near their historical average.”

- “However, shelter price inflation remains high.”

- “With continued evidence that underlying inflation is easing, Governing Council agreed that monetary policy no longer needs to be as restrictive and reduced the policy interest rate by 25 basis points.”

- “Recent data has increased our confidence that inflation will continue to move towards the 2% target.”

- “Governing Council is closely watching the evolution of core inflation and remains particularly focused on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour.”

- “The Bank remains resolute in its commitment to restoring price stability for Canadians.”

Summary of BOC Macklems press conference:

Bank of Canada Governor Tiff Macklem emphasized that interest rate decisions will be made on a meeting-by-meeting basis, depending on economic data. He said that if the economy continues to perform as expected and inflation eases, further rate cuts can be anticipated. Macklem is determined to bring inflation back to the 2% target but acknowledges that the work is not done and will evolve with the situation.

Macklem noted that the economy has broadly evolved as expected, boosting confidence that inflation will gradually return to the 2% target. However, the timing of any further cuts will depend on incoming data, with recognition of potential risks and bumps along the way.

Macklem stated that their forecasts indicate a gradual move towards the inflation target, but there are limits to how far their policy can diverge from the U.S., and they are not close to those limits. He also mentioned expectations for slower population growth, which has been factored into their forecasts. Population growth has eased employment pressures but increased demand for housing.

HE feells that the economy appears to be heading for a soft landing, with room for growth above potential for a period. While the Bank of Canada is normalizing its balance sheet, the policy remains restrictive due to inflation being above target. Macklem stated that interest rates will not return to pre-Covid levels and acknowledged past periods of significant divergence with the U.S. Federal Reserve.

On Thursday, the ECB also cut rates and like the BOC, the path for rates going forward is dependent on the data.

ECB RATE STATEMENT REVIEW

- “The Governing Council today decided to lower the three key ECB interest rates by 25 basis points.”

- “Based on an updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission, it is now appropriate to moderate the degree of monetary policy restriction after nine months of holding rates steady.”

- “Since the Governing Council meeting in September 2023, inflation has fallen by more than 2.5 percentage points and the inflation outlook has improved markedly.”

- “Underlying inflation has also eased, reinforcing the signs that price pressures have weakened, and inflation expectations have declined at all horizons.”

- “Despite the progress over recent quarters, domestic price pressures remain strong as wage growth is elevated, and inflation is likely to stay above target well into next year.”

- “The latest Eurosystem staff projections for both headline and core inflation have been revised up for 2024 and 2025 compared with the March projections.”

- “Staff now see headline inflation averaging 2.5% in 2024, 2.2% in 2025 and 1.9% in 2026.”

- “For inflation excluding energy and food, staff project an average of 2.8% in 2024, 2.2% in 2025 and 2.0% in 2026.”

- “Economic growth is expected to pick up to 0.9% in 2024, 1.4% in 2025 and 1.6% in 2026.”

- “The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner.”

- “It will keep policy rates sufficiently restrictive for as long as necessary to achieve this aim.”

- “The Governing Council will continue to follow a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction.”

- “The Governing Council today also confirmed that it will reduce the Eurosystem’s holdings of securities under the pandemic emergency purchase programme (PEPP) by €7.5 billion per month on average over the second half of the year.”

- “The Governing Council decided to lower the three key ECB interest rates by 25 basis points.”

- “The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will be decreased to 4.25%, 4.50% and 3.75% respectively, with effect from 12 June 2024.”

Summary of ECB Pres. Lagarde’s press conference said:

In October 2022, inflation peaked at double digits, but by September 2023, it had reduced to 5.2%, and currently, it stands at 2.6%. President Lagarde emphasized the need for more data to confirm the disinflationary path, noting that while restrictive measures were more pronounced in September, various factors such as base effects and wage trends could introduce uncertainties. Wages, particularly in the services sector, play a significant role in inflation. Although wages remain elevated, there are signs of a recent decline, and the ECB must consider wage divergences across countries and the impact on services prices.

The ECB’s policy decisions and data releases are not perfectly synchronized, making it difficult to predict future actions. Lagarde stated that market pricing of rate cuts is independent of ECB decisions, which have resulted in a reduction of anticipated rate cuts from 64 bps to 36 bps for the remainder of the year, totaling ~61 bps. Despite various challenges, including unanticipated bumps in the disinflationary process, the ECB is committed to bringing inflation back to the 2% target in the medium term. The decision to moderate the restrictive stance was almost unanimous, except for one governor. The ECB will continue to take a serious approach to combating inflation, staying restrictive until the 2% target is achieved. Lagarde affirmed that the ECB is far from reaching the neutral rate, which remains a key objective.

The Fed and BOJ are next

Next week the Fed will announce their rate decision on Wednesday while the Bank of Japan will announce its intentions on Friday.

For the Fed, the Fed is expected to keep rates unchanged. Inflation remains sticky and although the most recent CPI and PCE data was encouraging, it remains above the target rate. Many of the Fed officials – including Fed Chair Powell – have expressed the need to keep rates unchanged given solid growth and higher-than-expected inflation in the 1Q. The Atlanta Fed GDPNow growth estimate did decline to 1.8% recently, but has bounced back to 3.1% helped by the US jobs report today.

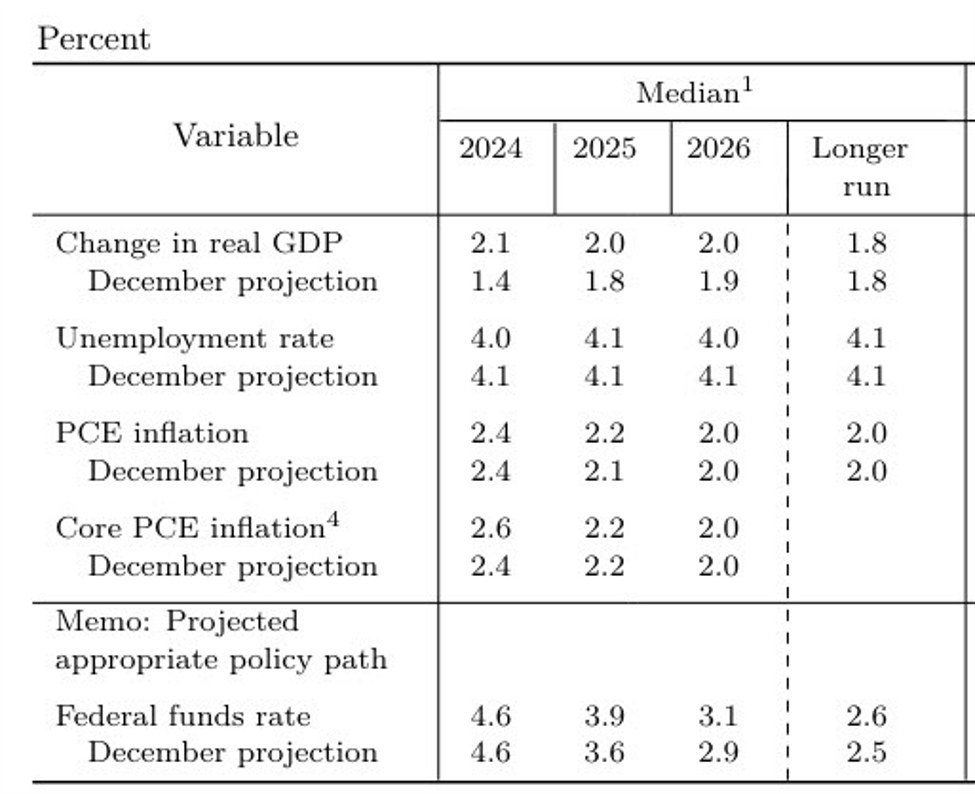

What will be of interest to the markets on Wednesday will be the projections for GDP, inflation and employment going forward, as well as the dot-plot of rate expectations at the end of 2024, 2025 and 2026 – especially the expectations for the end of 2024 (let’s face it, 2024 is hard enough. To forecast 2025 and 2026 is nice but just a guess).

The median of growth, employment and inflation from March’s projections showed GDP at 2.1% in 2024, unemployment at 4.0% and Core PCE at 2.6%. GDP is higher than that currently which may prompt a move higher in their end of year forecast. THe unemployment rate reached 4.0% today and as a result, may be raised as well. The Core PCE may be a touch low given the stickiness.

The dot plot forecast 3 cuts by the end of the year in March (target 4.6%). The market is currently pricing in about 40 basis points by the end of the year. That sounds about right.

Below is the look at the dot plot. It is hard to believe at the end of last year the Fed forecast 6 cuts in 2024.

Dot plot

The Bank of Japan is on a different path as they still maintain expansionary policy. They may look to pull back on bond buying when they announce its rate decision on Friday.