Jaroslaw Kilian/iStock Editorial via Getty Images

Wizz Air (OTCPK:WZZAF) (OTCPK:WZZZY) is one of the businesses that I like a lot. On many of the routes I regularly fly, Wizz Air is one of the airlines to choose from. So, I get to see the aircraft and experience the service myself. In June 2023, I marked Wizz Air stock a buy, but the reality is that the stock price has declined significantly since. In this report, I discuss the reasons for that decline as well as the most recent earnings, and I will discuss whether there is any reason to adjust my rating.

Wizz Air Is Facing PW1000G Engine Issues

Dhierin-Perkash Bechai

The picture above is one I took in April 2024 when boarding my flight to Bucharest. In the same picture, we likely also see the reason why Wizz Air stock is down considerably. It is not the blue skies or the green trees in the background, but the engines mounted under the wing. Wizz Air has Airbus A320neo family airplanes that equipped with Pratt & Whitney PW1100G and those engines are subjected to the fleet management plan of RTX Corp. (RTX) as high-pressure turbine disks and high-pressure compressor parts may contain contaminated powder. In total, there are 1,200 engines that may be affected, but there are 600 to 700 engines that require accelerated removal and inspection with approximately 250 to 300 days of grounding time and 350 airplanes being grounded on average between 2024 and 2026.

The impact on Wizz Air has been significant; by the end of last year there were 13 airplanes grounded and by January that number had climbed to 33 with total grounded airplanes likely to have reached 40 by the end of March 2024. While I was taxing for my departure from Bucharest back to The Netherlands, we taxied past an airplane that was having its engine replaced. So, it is needless to say the disruptions are also visible on the tarmac. At the time of writing, there are 46 Airbus A320neo family airplanes grounded, which essentially means that over a fifth of the Wizz Air fleet is currently grounded and that excludes 5 Airbus A320ceo family airplanes that are also grounded. That provides a huge pressure on the ability to expand capacities and absorb fixed costs in an efficient way.

Wizz Air did expand capacity as much as possible during Q3 ahead of the groundings increasing significantly in the subsequent quarter, and it did receive compensation for groundings during the quarter. Wizz Air does not provide detailed statements on balance sheet or cash flows during the first and second quarter earnings release. So, at this point, it is not possible to get a grasp of how high that compensation is. What we do know, however, is that the company is receiving a significant refund from plane maker Airbus (OTCPK:EADSF) as deliveries are sliding. In FY2023, on gross CapEx of €640 million including advance payment for aircraft, Wizz Air received refunds in the amount of €463.4 million and for the first half of FY2024 €218.6 million was refunded while €112.3 million was paid in advances.

Wizz Air Sees Revenue Growth In Line With Cost Growth

Wizz Air

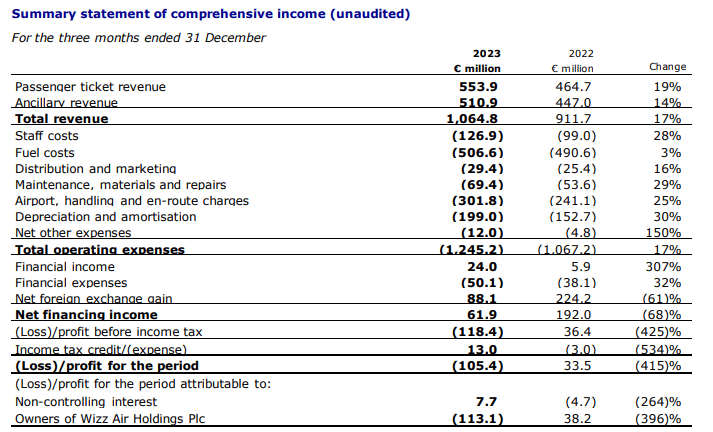

For the third quarter 2024 (Wizz Air starts it book year in April), revenues grew 17% with 19% growth in passenger revenues and 14% growth in ancillary revenues. Cost grew in line with revenues, but that was primarily driven by modest growth in fuel costs, as fuel prices declined 17.5%. The costs should also be viewed in the context of capacity additions, and then we see that things are looking a bit less smooth. Capacity increased by nearly 27% and revenue growth fell short of that, indicating lower unit revenues, which, according to my calculations, were around 6% lower. On a per-seat basis, costs decreased 9%, but most of that was achieved through the reduction in fuel prices. Excluding fuel, the costs came down by just 1.1%. So, we do see the inflationary costs offsetting much of the cost absorption, and that is an industry reality. In the end, I think that for the third quarter, Wizz Air did very well on containing unit costs while also adding capacity in anticipation of capacity being taken out of the market in Q4. That could explain why competitor Ryanair saw summer fares growth being softer than anticipated.

For the third quarter, operating income was a €180.4 million loss compared to €155.5 million loss a year earlier, driven by higher staff costs and navigation and handling fees and charges.

Is Wizz Air Stock A Buy?

The Aerospace Forum

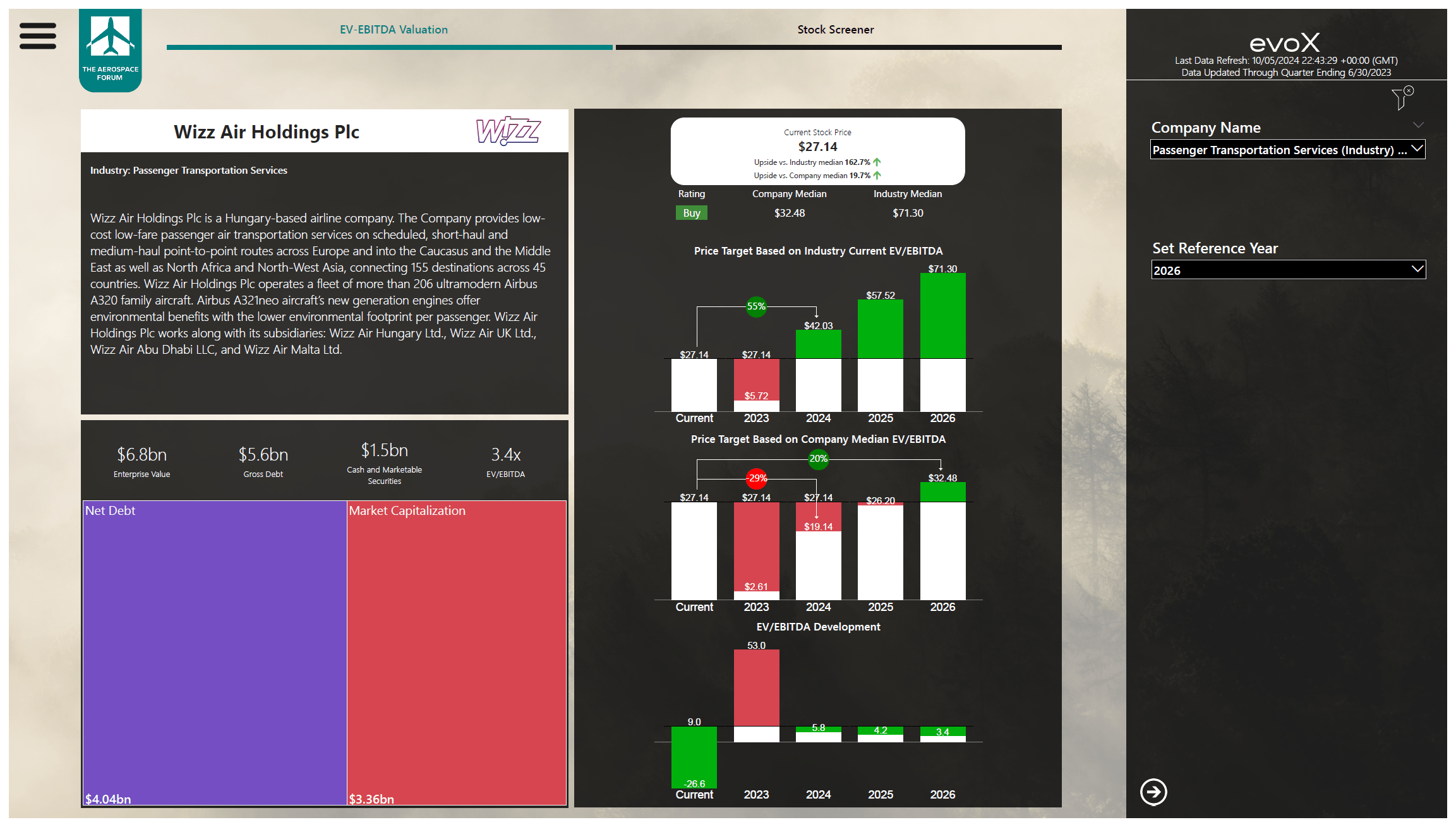

I believe that Wizz Air is navigating the engine crisis as best as it can. The airline is mitigating the impact of the engine crisis by absorbing new airplanes, extending leases and improving utilization, while it is receiving compensation from RTX. The big question is whether Wizz Air stock is a buy. In order to assess that, I have implemented the most recent balance sheet data, cash flows and projections for EBITA and cash flows into my model. Wizz Air has yet to reported FY24 results, but against FY25 earnings the stock would be somewhat fairly valued. Allowing the stock to trade one year ahead of earnings, we see 20% upside for Wizz Air stock. Based on the low EV/EBITDA compared to the peer group, I believe that Wizz Air stock is a compelling investment opportunity as FY26 price targets show solid upside while EV/EBITDA multiple expansion towards industry standard would provide even higher upsides.

Conclusion: Wizz Air Remains A Buy On Prudent Crisis Management

While the year is not quite unfolding the way Wizz Air had expected, I believe that management is executing the best it can with low-cost in mind, and while the impact of the engine crisis will be felt by Wizz Air for some time, they are receiving compensation from RTX Corp., and they continue to take delivery of aircraft that will help the company offset some grounding impact. Next to that, the airline is receiving payments from plane maker Airbus for slides in the delivery schedule. So, there is a clear plan to control cost. The bigger question will be the strength of unit revenues going into the summer. For the summer season, Wizz Air has guided for flat capacity, which should provide some protection against unit revenue pressure. Though, the big question is what competitors such as Ryanair do will do in terms of exerting pricing pressure.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.