Galeanu Mihai

Introduction & Funding Thesis

Workday (NASDAQ:WDAY) is a supplier of enterprise cloud purposes for finance and human sources. The inventory has underperformed the S&P 500 and Nasdaq 100 YTD. The corporate launched its Q4 FY24 earnings report final month, the place income and earnings exceeded expectations. It’s projected to develop its income by 15–16% to roughly $8.4B in FY25 because it continues to focus its efforts on increasing internationally whereas constructing its associate ecosystem to be able to develop effectively by way of referrals, co-selling, and constructing differentiated options to be able to drive higher enterprise outcomes for its prospects. On the similar time, the corporate can be investing its sources in integrating AI capabilities on its platform, together with the announcement of its acquisition of HiredScore, to be able to speed up its AI product roadmap. In the meantime, Workday’s profitability is rising together with increasing margins because it streamlines its working bills.

There isn’t a denying that the corporate has superior fundamentals; nevertheless, when trying on the valuation, I imagine that there’s room for at most 12% upside from its present ranges, which to me doesn’t current a beautiful entry level for long-term buyers. Consequently, I’ll keep on the sidelines, ready for a greater entry level to provoke a place, and fee the inventory a “hold” in the meanwhile.

About Workday

Workday is a cloud-based software program firm that gives options for monetary administration, spend administration, human capital, planning, and analytics in order that their prospects can higher plan, execute, and enhance their enterprise operations.

By way of its enterprise mannequin, Workday targets medium and enormous companies globally throughout completely different industries, the place it derives its income from a mixture of subscription {and professional} providers. The corporate makes use of a “land-and-expand” go-to-market technique, which permits it to promote subscriptions for extra product modules to current prospects as they broaden their footprint with Workday’s merchandise.

In FY24, the corporate generated $7.3B in income, out of which Subscription income accounted for 91% at $6.6B, whereas Skilled Providers accounted for the remaining 9% at $5.5B.

The great: Worldwide Income progress, Accomplice ecosystem, Product Innovation & Rising Margins

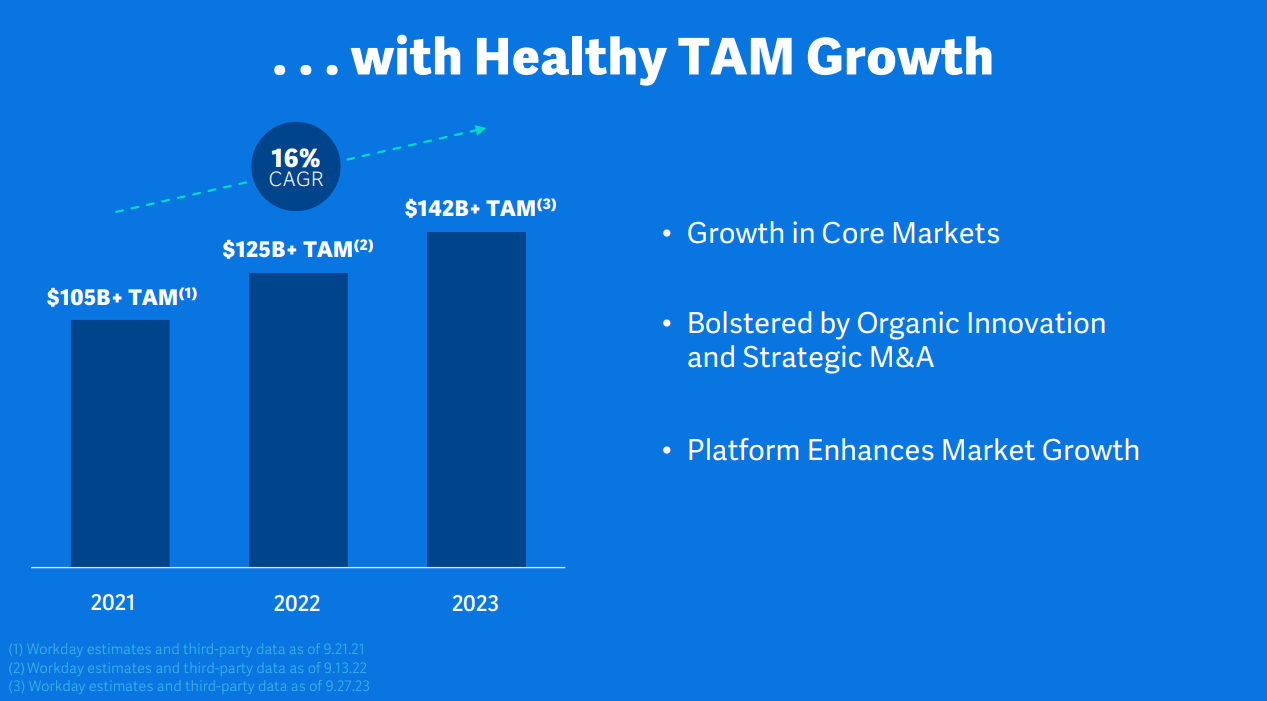

Workday operates in a big whole addressable market (TAM) that it estimates at $142B in 2023, as per its Investor Day Presentation. The TAM is calculated by summing up the sizes of the next markets: 1) Human Capital Administration (HCM) at $58B and a couple of) Monetary Administration at $84B. Provided that the corporate generated $7.3B in income in FY24, it could imply that it has penetrated 5% of its market share. As per its Investor Day Presentation, Workday has so far penetrated 50% of Fortune 500 firms and 25% of International 2000 firms, which implies it nonetheless has 50% of Fortune 500 and 75% of International 2000 remaining as a part of its goal market that’s left to be penetrated, thus presenting a big sufficient market alternative. Concurrently, Workday believes that it has doubtlessly $2B of enlargement alternative inside their current Prime 100 Accounts, because it continues to drive deeper adoption of its answer suite, thus permitting it to broaden its Annual Contract Worth (ACV) and harness economies of scale.

2023 Investor Presentation: Workday’s rising TAM

In FY24, the corporate generated $7.3B in income, up 17% YoY. Subscription Income contributed 91% to whole income, rising 19% YoY to $6.6B. One of many methods the corporate believes it might spearhead its progress trajectory within the coming years is thru worldwide enlargement, with a selected focus in Europe, Center East and Africa, because it estimates its worldwide TAM at $80B. For the complete yr FY24, worldwide income totaled $1.8B, rising 17% YoY, whereas US income additionally grew 17% YoY to $5.46B. This could imply that Workday has nearly 2.2% penetration of its options outdoors of the US, which makes it a extremely strategic alternative to broaden into to be able to drive income progress. In the course of the earnings call, Carl Eschenbach, CEO of Workday, highlighted that they noticed wholesome progress in ACV throughout key markets that embrace the UK, Spain, and France.

Moreover, Workday administration additionally highlighted Japan as a key funding precedence and has due to this fact employed a brand new chief, Chikara Furuichi, to drive progress in that area. In my view, this additional highlights the administration’s concentrate on driving progress in key areas outdoors of the US, particularly because the US market has matured and progress will possible stabilize transferring ahead. Consequently, if Workday continues to see success in gaining market share overseas, it can maintain its progress story alive.

Other than Workday’s strategic focus to drive progress internationally, the corporate can be centered on constructing its associate ecosystem, which I imagine will permit it to develop extra effectively by way of referrals, co-selling, and constructing differentiated options to be able to drive higher enterprise outcomes for its prospects. That is what Carl Eschenbach, CEO of Workday, mentioned in the course of the earnings name, which demonstrates the corporate’s concentrate on driving progress by way of sturdy associate ecosystems.

“During Q4, we announced a strategic partnership with Insperity. Through this partnership, Workday will become the platform powering Insperity’s PEO service for SMB organizations, effectively opening up a new market opportunity for us. It’s a terrific example of how we’re innovating our go-to-market strategy to drive growth. Another great example is the Spark&Grow offering, which we launched with Kainos. It helps our emerging and medium enterprise customers to go live on Workday in less than 4 weeks. We’ve seen incredible demand for this offering, and we’re just getting started. These are 2 great examples of momentum that is building across our ecosystem, which I’m pleased to share now includes more than 200 partners that have been onboarded to refer new sales leads and co-sell with us.”

On the similar time, Workday stays dedicated to driving sturdy product innovation to be able to proceed to drive new prospects in addition to deepen adoption amongst its current buyer base. To date, Workday has launched Workday Abilities Cloud, which makes use of AI to achieve insights into a corporation’s present abilities to be able to allow managers to successfully lead and foster the profession progress of their staff members based mostly on abilities and pursuits. They additional introduced their acquisition of HiredScore to be able to speed up their AI product roadmap in order that they will ship insights to be able to enhance recruiting and inside mobility inside a corporation.

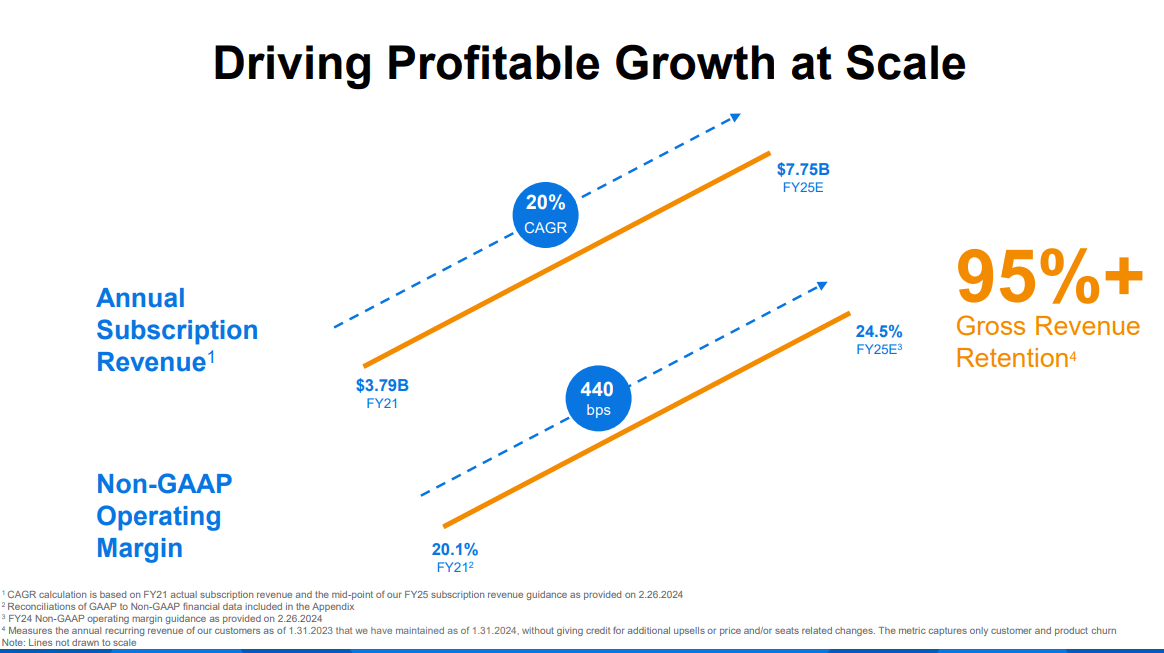

Shifting gears to profitability, Workday generated $1.7B in non-GAAP working earnings in FY24, which grew 42% YoY at a margin of 24%, in comparison with a margin of 19.5% from the prior yr. One of many causes for the enlargement in margin will be attributed to the streamlining of working bills that grew 10% YoY, relative to income that grew 17% YoY, which demonstrates the corporate’s rising operational effectivity. On the similar time, Web Retention fee (NRR) is above 100%, which signifies that the corporate is constant to see success in driving deeper adoption of its options throughout its current prospects, serving to it unlock economies of scale.

This autumn FY24 Earnings Slides: Workday’s rising income and profitability

Trying ahead into FY25, the corporate is expected to develop its revenues between 15 and 16% YoY to $8.35-$8.41B, with Subscription income projected to develop barely sooner between 17 and 18% YoY to roughly $7.74B. In the meantime, the non-GAAP working margin is anticipated to develop barely to 24.5%, which might translate to a non-GAAP Working Earnings of $2.04B. In the course of the Investor Day presentation, the administration additional outlined that it expects subscription income to develop yearly between 17 and 19% till FY27, whereas producing a non-GAAP working margin of 25%. I imagine that thus far, the corporate has executed properly, and if it continues to drive deeper market share internationally with the assistance of its associate ecosystem whereas investing in innovation to deepen adoption of its answer amongst its current buyer base, it ought to be capable to obtain each its income and profitability targets.

The unhealthy: Giant gamers and an unsure world macroeconomic surroundings

To date, Workday has very properly navigated a troublesome macroeconomic surroundings; nevertheless, with inflation above the Fed’s 2.2% and rates of interest at 5.25-5.5%, there’s a rising probability of a broader slowdown, which can tip the US economic system right into a recession. In the meantime, now we have already seen elements of Europe falling into a recession, together with Japan. This may increasingly harm Workday’s progress trajectory, particularly its plans for worldwide enlargement, if we see firms chopping down enterprise spending to be able to shield their margins.

On the similar time, Workday also faces competition from deep-pocketed gamers reminiscent of SAP (NYSE:SAP), Oracle (NYSE:ORCL) within the mid-market and enormous enterprise market that Workday operates in. Whereas product innovation pertaining to generative AI can play as a significant differentiation issue, I’d notice that Workday is smaller in measurement in comparison with these bigger gamers within the trade, which might show to be a aggressive drawback.

Tying it collectively: Workday has a 12% upside from its present ranges.

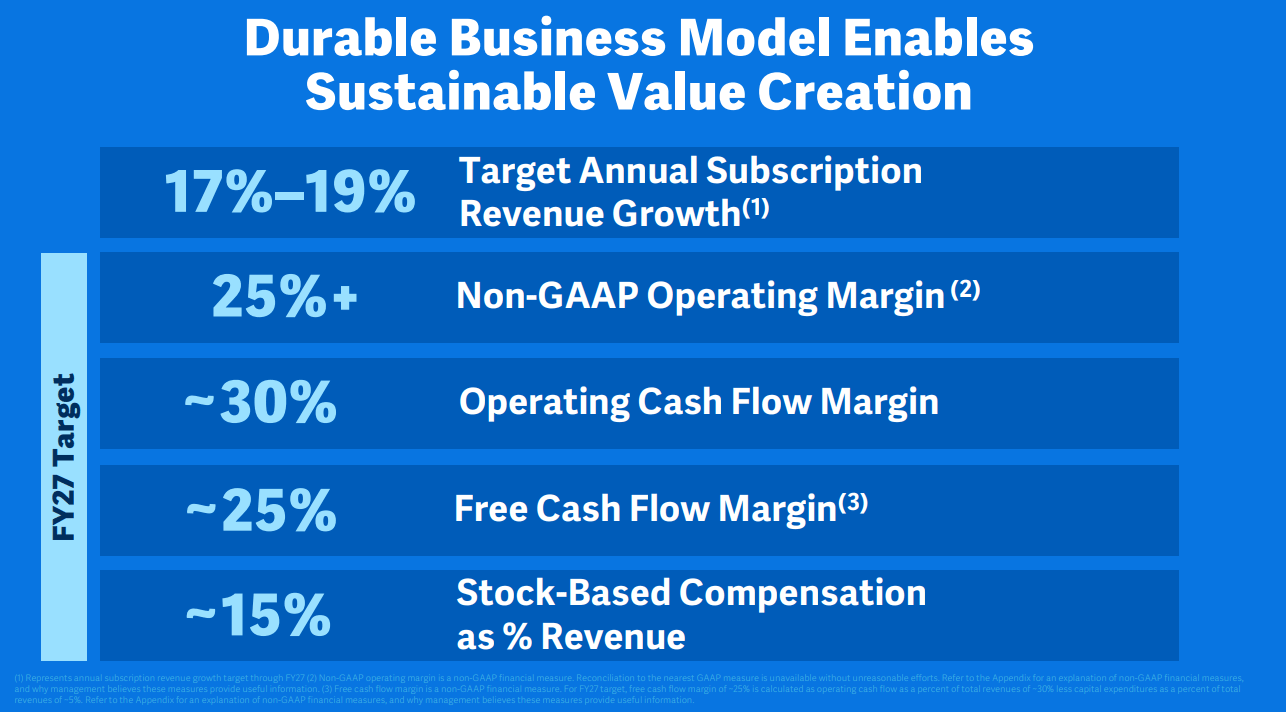

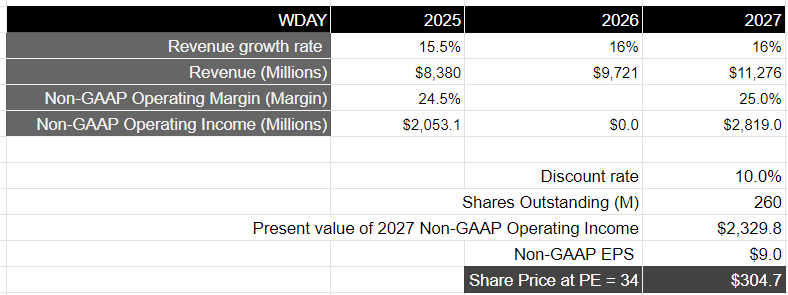

Assuming that Workday continues to develop its whole income by 16% yearly till FY27, it ought to generate roughly $11.3B in income. I imagine Workday will be capable to obtain their projections, given the administration’s focus to drive progress internationally, whereas constructing its associate ecosystem and investing in its product innovation on the similar time. By way of profitability, Workday administration believes it ought to be capable to preserve a non-GAAP working margin of 25%. Provided that Workday’s present non-GAAP working margin is between 24-25%, it ought to be capable to preserve that till FY27, per administration’s expectation, because it continues to unlock working leverage, because it drives deeper adoption of its options amongst current prospects, whereas streamlining working bills. At a non-GAAP working margin of 25%, it could translate to a non-GAAP working earnings of $2.8B by FY27, which is equal to $2.3B when discounted at 10%.

2023 Investor Day Presentation: Workday’s long-term monetary mannequin

Taking the S&P 500 as a proxy, the place its firms develop their earnings on common by 8% over a 10-year interval, with a price-to-earnings a number of of 15-18, I imagine that Workday ought to commerce at twice the a number of, as I imagine it can develop its earnings at twice the speed of the common S&P 500 firm over the following 3 years. That might translate to a price-to-earnings a number of of roughly 34, which is twice the PE ratio of the S&P 500, or a value goal of $304, as will be seen within the valuation mannequin beneath. This represents an upside of 12% from present ranges.

Writer’s Valuation Mannequin

Nonetheless, trying on the S&P 500, its present ahead price-to-earnings ratio stands at 20.9, which is above its 5-year common of 19.1 and 10-year common of 17.7. Which means that within the shorter timeframe, we might see a large pullback within the S&P 500 of at the very least 10% to revert its PE ratio to its 10-year common. This might happen, within the occasion of inflation coming in increased than anticipated, or Q1 earnings coming barely beneath expectations. Provided that Workday has a beta of 1.33, a decline of 10% within the S&P 500 can translate to a 13% decline in Workday’s inventory value, by which case, there could be no internet upside on the present inventory value degree, given the 13% margin of security. Consequently, I’ll fee the inventory a “hold” in the meanwhile.

Conclusion

Workday has strong fundamentals and nice progress drivers that embrace its associate ecosystem, worldwide enlargement, and speedy product innovation. On the similar time, the administration stays centered on bettering profitability. Nonetheless, based mostly on my valuation, I imagine that there’s roughly 12% upside from the place the inventory is at the moment buying and selling, which I imagine doesn’t current a beautiful entry level for long-term buyers. Consequently, I will probably be ready for a greater alternative to provoke a place within the firm and, within the meantime, fee the inventory a “hold” in the meanwhile.