Thinkhubstudio

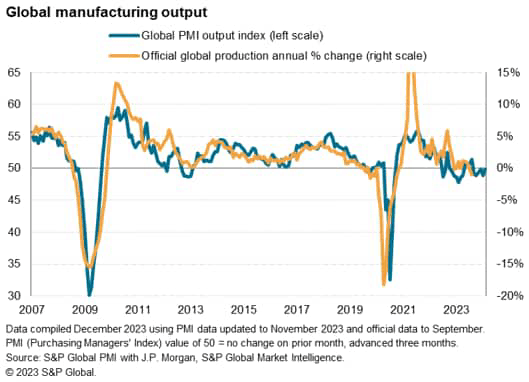

World manufacturing enterprise circumstances worsened for a fifteenth successive month in November, in keeping with the newest JPMorgan World Manufacturing Purchasing Managers’ Index™ (PMI™) compiled by S&P World. The headline PMI – a composite index primarily based on 5 survey variables – registered 49.3, up from 48.8 in October however remaining under the 50.0 no change stage to merely point out a moderation within the tempo of decline.

Manufacturing continued to edge decrease in response to an extra deterioration so as books. The latter additionally contributed to an extra month of subdued confidence concerning the outlook, prompting producers to chop employment for a 3rd month working. This represents one of many worst international job market performances because the international monetary disaster.

Corporations additionally continued to chop again their enter shopping for, although November noticed some easing within the current drag on output from cost-cutting associated stock discount insurance policies, which is able to probably present some help to manufacturing within the months forward if sustained.

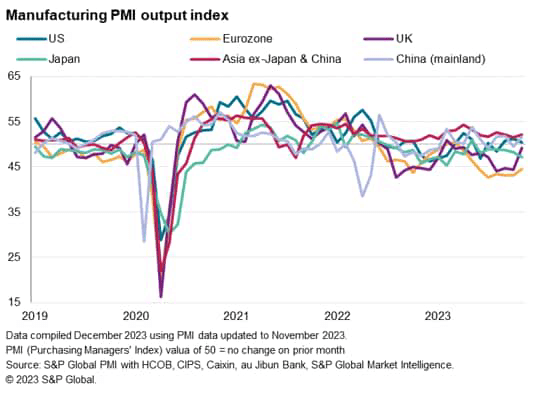

Europe continued to see the steepest downturn, with output additionally falling in Japan, although manufacturing returned to progress in mainland China and confirmed indicators of stabilising within the UK. Modest progress was once more in the meantime recorded in North America, together with within the US. By far the strongest efficiency, nevertheless, was recorded as soon as once more in India.

World manufacturing unit output edges decrease once more in November amid additional demand fall

World manufacturing output fell for a sixth consecutive month in November, in keeping with the newest PMI surveys compiled by S&P World and sponsored by JP Morgan, although the decline signalled by the survey’s manufacturing index was solely very marginal and the weakest seen through the current downturn.

Output has solely risen globally in simply 4 of the previous 16 months, reflecting a post-pandemic shift in spending from items to companies and subdued spending amid greater costs and elevated rates of interest, however current months have seen solely very modest declines.

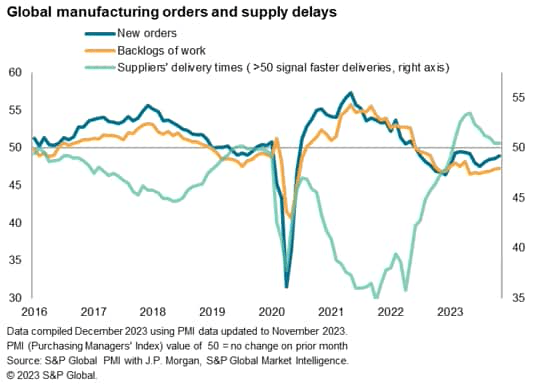

A key issue stopping a steeper decline in manufacturing has been the fulfilment of backlogs of orders, amassed through the pandemic-related provide shortages. Such shortages have eased significantly throughout 2023, facilitating greater output. Backlogs of labor have consequently now fallen for 17 consecutive months.

A rising concern amongst producers, nevertheless, has been a continuous decline in inflows of latest orders over the previous 17 months, which implies order books have gotten more and more depleted.

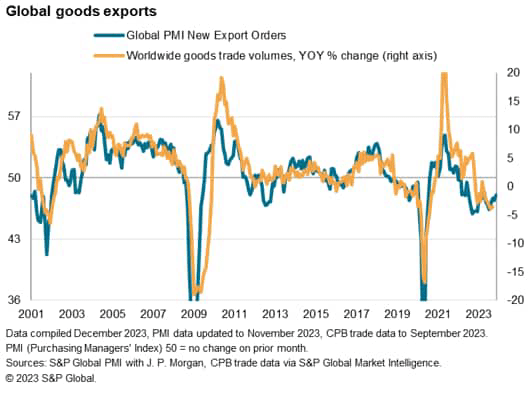

World commerce flows stay particularly weak, with new export orders for items falling globally for a twenty-first straight month in November, representing the worst spell for exports because the international monetary disaster barring solely the preliminary pandemic lockdowns. Whereas the speed of decline in exports moderated to the slowest for seven months in November, the speed of contraction remained marked by historic requirements.

Gloomy prospects drive job losses and cost-cutting

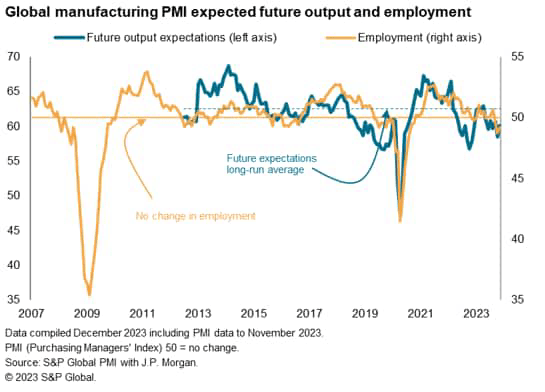

The sustained downturn in demand signalled by the survey contributed to an extra gloomy outlook for the yr forward amongst producers. Though enterprise expectations lifted from October’s current low, the extent remained properly under the survey’s long-run common.

This downbeat temper led to a 3rd successive month of falling employment within the manufacturing sector worldwide, as corporations sought to regulate working capability decrease according to demand. Though the tempo of job losses eased barely in November, the previous three months have seen the typical payroll discount exceeded since 2009 solely by that recorded the early pandemic months.

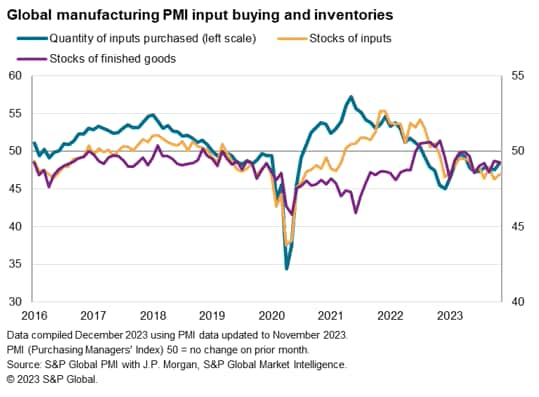

Equally, producers continued to concentrate on lowering their purchases of inputs, and ensured additional value financial savings via the running-down of inventories of each inputs and completed items.

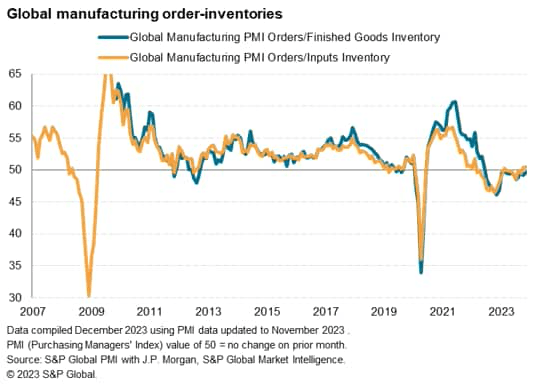

Stock cycle turning

There are some glimmers of higher information, nevertheless, notably via the survey knowledge on inventories, particularly these of inputs and uncooked supplies. Though nonetheless declining, producers’ buying of inputs fell on the slowest price for seven months in November.

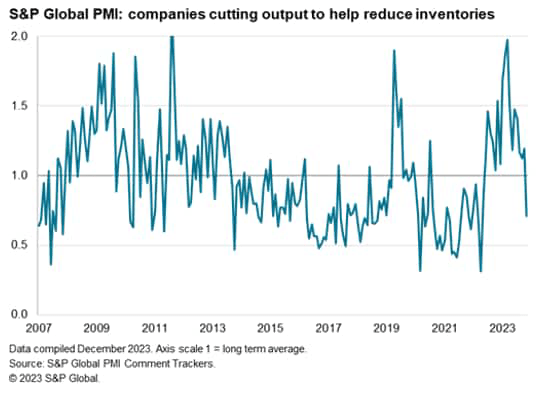

On the identical time, evaluation of anecdotal proof collected in survey responses (which powers our PMI Remark Tracker dataset) exhibits a marked fall within the variety of corporations globally which are reducing output intentionally as a way to cut back inventories.

As such, the information subsequently trace at a shift away from stock discount insurance policies and an easing within the accompanying drag on international manufacturing manufacturing, which seems to have helped elevate a few of the survey gauges in November.

A shift to the stock cycle changing into extra supportive to progress is likewise hinted at by the survey’s order-to-inventory ratio, particularly by way of orders relative to inventories of inputs. Nevertheless, it’s clear that any such inventory-led progress stimulus stays very modest, reflecting the truth that, though inventories of inputs have gotten extra depleted in comparison with the excessive ranges amassed through the pandemic, the necessity to replenish inventory stays low amid the continuing downturn in last demand.

Eurozone continues to report sharpest decline

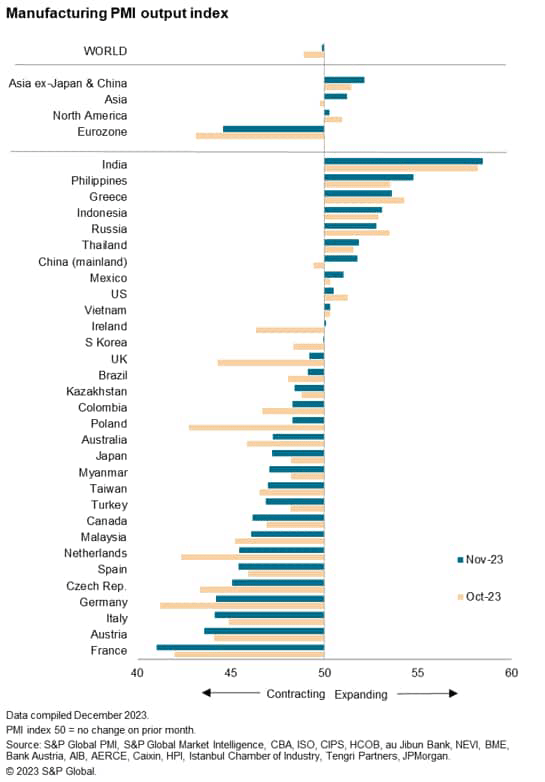

Drilling down geographically, solely 11 economies monitored by the S&P World PMI surveys reported greater manufacturing output in November whereas 20 reported decrease manufacturing.

By broad area, the eurozone as soon as once more reported by far the sharpest downturn whereas Asia returned to progress after briefly slipping into contraction in October. North American manufacturing continued to develop marginally.

In additional element, the seven fastest-contracting manufacturing economies have been all present in Europe, with France changing Germany because the worst performer. The UK notably noticed a near-stabilisation of manufacturing, and output in mainland China revived after slipping into contraction in October. Downturns in the meantime eased in South Korea and Taiwan, however deepened in Japan.

When it comes to one of the best performers, the strongest output achieve continued to be recorded in India, the place an ongoing manufacturing growth far outpaced all different economies coated by the S&P World PMI surveys, adopted by the Philippines, Greece and Indonesia.

Editor’s Word: The abstract bullets for this text have been chosen by In search of Alpha editors.