Funding thesis

Worldwide Seaways (NYSE:INSW), Inc. is a US-listed small-cap firm doing enterprise in worldwide shipments of crude oil and oil merchandise.

Over the previous couple of years, 85% of income got here from contracts that have been concluded at spot charges, which has allowed the corporate to profit when maritime transport went via intervals of turbulence. For instance, as transport corporations have responded to the elevated dangers related to Houthi assaults within the Crimson Sea by diverting ships to different routes, Worldwide Seaways shares have risen greater than 15%.

The corporate operates a big fleet, which is barely youthful than the common market age. In 2023 it took supply of three new dual-fuel VLCC tankers, that are a lot wanted available in the market. Plans are to take supply of two LR1 tankers on the finish of 2025.

We’ve got not beforehand coated Worldwide Seaways, so on this overview, we are going to take a more in-depth take a look at the corporate’s enterprise construction.

We anticipate that the corporate will earn a income of $1 083 mln (+25% y/y) in 2023, and $945 mln (-13% y/y) in 2024. Income is ready to say no on the again of a lower in spot charges. The corporate’s EBITDA will whole $742 mln (+34% y/y) in 2023, and $580 mln (-22% y/y) in 2024. The ranking is HOLD.

The enterprise of Worldwide Seaways

Integrated in 1999, Worldwide Seaways, Inc. is engaged within the possession and operation of Marshall Islands-flagged, oceangoing vessels that transport crude oil and oil merchandise world wide.

Earlier than October 2016, Worldwide Seaways operated under the father or mother firm Abroad Shipholding Group, Inc. Then a deal occurred that led to the emergence of two companies – OSG and INSW – that had separate administration and possession. On July 16, 2021, Worldwide Seaways accomplished a merger with Diamond S Transport, making a joint fleet of 102 ships and making the corporate the US second-biggest tanker firm by the variety of ships and third-biggest by deadweight.

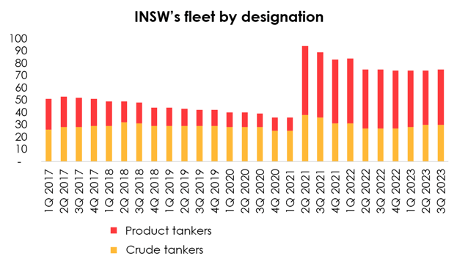

Since then, the corporate has reduce down its fleet as a part of an improve program, so it presently numbers 30 crude oil tankers and 45 oil-product tankers. The common age of Worldwide Seaways’ fleet is 12.6 years, in contrast with the market common of 12.8 years, which the corporate famous in its third-quarter presentation.

Make investments Heroes Stefan Lambauer/iStock Editorial by way of Getty Pictures

Based on INSW’s monetary outcomes for the previous 12 months, crude oil tankers and oil-product tankers make an equal contribution to the corporate’s income. Of the overall fleet, as of 3Q 2023, 81% of tankers are owned by the corporate, and the remaining 19% are leased.

Let’s now check out the markets for crude tankers and product tankers individually.

Tanker transport: crude oil

The corporate makes use of the next three kinds of tankers to ship crude oil:

- VLCC (Very Massive Crude Carriers) – massive tankers with a deadweight of 200-320 thousand tons (deadweight, or DWT, is a measure of how a lot weight a ship can carry, together with the burden of cargo, gasoline, contemporary water, ballast water, provisions, passengers and crew).

- Suezmax – oil tankers able to passing via the Suez Canal with full load; they’ve a deadweight of 120-180 thousand tons.

- Aframax (AFRA – Common Freight Price Evaluation). Non-OPEC oil exporting nations use the sort of tanker as a result of their ports and method channels are unable to accommodate bigger tankers. These tankers have a deadweight of 75-120 thousand tons.

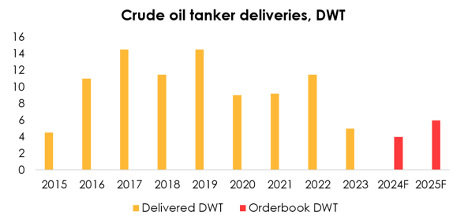

Forecasts from BIMCO and Danish Ship Finance agree that demand for crude oil tankers is predicted to exceed provide in each 2024 and 2025. The variety of orders to construct new vessels of this kind will improve too late to alleviate the tightness in 2024 and 2025. The explanation: the dearth of obtainable slots at shipyards.

MISC

Tanker deliveries are anticipated to fall to three.5-4 mln tons of deadweight in 2024, the bottom in not less than 20 years, earlier than they’ll rise to about 6 mln tons in 2025, additionally a low quantity traditionally.

Danish Ship Finance

The EIA expects a slight extra of demand over provide in 2024 and, conversely, a slight oversupply in 2025.

Based on the EIA, international oil demand will climb by ~1% in 2024, reflecting a sluggish progress of world GDP and the declining share of this gasoline within the construction of consumption by motor autos. Progress might be primarily pushed by non-OPEC+ nations such because the US and Brazil, whereas OPEC+ provide, particularly from Saudi Arabia and Russia, will depend upon voluntary manufacturing cuts in 2024.

There are expectations that demand for VLCC will rise in 2024 because the US and Brazil ramp up their long-haul crude oil exports.

Based on analysis by Danish Ship Finance, most barrels from the Center East are shipped on VLCCs and presently makeup ~40% of China’s seaborne crude imports. Assuming the voluntary oil manufacturing cuts by Saudi Arabia and different OPEC members stay in place, OPEC nations within the Center East will solely have the ability to improve whole seaborne exports by 300,000 barrels per day in 2024. China should add import volumes from different nations to satisfy its anticipated 600,000 barrels per day improve in oil demand. For instance, China’s imports from the US and Brazil have been a key motive why demand for VLCCs climbed in 2023, and the variety of VLCCs going from these nations to China has doubled over the previous 6 years. If the pattern continues, and with the variety of tankers within the fleet remaining virtually unchanged, the utilization of the VLCC fleet will improve.

Environmental necessities create hurdles for VLCC vessels.

Virtually all VLCC vessels that transported crude oil from Brazil or the US to China in 2023 used typical gasoline, and a few third have been greater than 10 years outdated. The Brazil-China and US-China routes stretch over vital distances and require loads of gasoline, which prompts the discharge of enormous portions of greenhouse gases. Older VLCC ships will seemingly have to scale back pace to satisfy emission rules, which can imply longer journey instances. That can lead to greater utilization of the VLCC fleet and elevated demand for dual-fuel tankers.

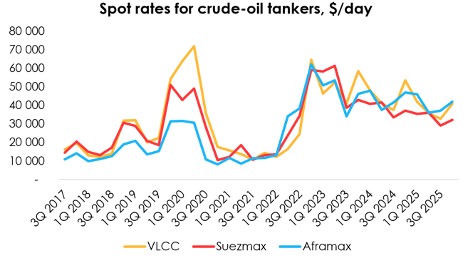

Thus, in 2023 each freight charges and costs for used crude oil tankers constantly remained at elevated ranges. Newbuilding costs additionally reached all-time highs and this pattern is drawing assist from the rising demand for dual-fuel tankers.

In 2024 demand is predicted to exceed provide with little potential for deliveries of recent tankers. Nonetheless, the imbalance might be smaller in contrast with 2023, so charges will proceed to say no from peak ranges as a part of seasonal fluctuations. Further demand for VLCCs may come up if China strikes to ramp up oil imports from Brazil and the US.

In 2025 extra tankers will enter the market, however demand is predicted to develop slower than provide and, in consequence, charges will proceed to say no. As a consequence of excessive fleet utilization, we don’t assume that charges will attain pre-crisis ranges.

Due to this fact, this is the efficiency of quarterly spot charges for VLCC, Suezmax, and Aframax tankers that we anticipate, making an allowance for seasonal fluctuations.

Make investments Heroes

The desk under exhibits common annual spot charges for the three kinds of tankers.

Make investments Heroes

Tanker transport: oil merchandise

The corporate makes use of the next three kinds of tankers to ship oil merchandise:

- LR2 (Lengthy Vary 2) – these vessels can name at most main ports and be used to hold each crude oil and oil merchandise. They’ve a deadweight of 80-160 thousand tons.

The LR1 and MR kinds of vessels, which have a smaller dimension, are used to move oil-product cargoes over comparatively brief distances, for instance from Europe to the US East Coast. Their smaller dimension permits them to entry most ports world wide.

- LR1 (Lengthy Vary 1) – a deadweight of 45-80 thousand tons.

- MR (Medium Vary) – a deadweight of 25-45 thousand tons.

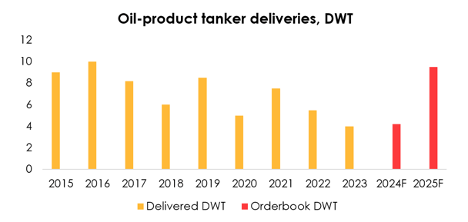

Forecasts from BIMCO and Danish Ship Finance agree that demand for oil-product tankers will virtually equal their provide in 2024, whereas they are going to be in extra provide in 2025 on account of scheduled deliveries of recent tankers. Based on combination estimates, the fleet of oil-product tankers will develop by ~2% in 2024 and by ~4.5% in 2025.

Due to this fact, provide will increase quicker than demand in 2025, which is prone to take away any shortages and make chartering schedules much less tight.

Danish Ship Finance

Future hull surveys and upgrades of exhaust fuel cleansing techniques (scrubber) may sometimes offset the growth of the worldwide fleet by as much as 2% in 2024 and 2025, lowering the chance of extra capability.

Rising gross sales of electrical autos are an element that restrains the expansion in demand for conventional fuels.

Based on the IEA, electrical car gross sales shot up from about 1 mln items to greater than 10 mln items from 2017 to 2022. Within the prior five-year interval, from 2012 to 2017, EV gross sales jumped from 100,000 items to 1 mln items, highlighting the exponential progress of the gross sales. The share of EVs in whole car gross sales expanded from 9% in 2021 to 14% in 2022 – and that is greater than 10 instances greater in contrast with 2017. In 2023, electrical car gross sales made up 18% of the worldwide whole for automobile gross sales.

Nonetheless, the world continues to be extremely depending on conventional motor gasoline.

The Worldwide Power Company estimates that motor autos make up about 60% of the present international demand for oil. This demand is steadily recovering, though motor gasoline consumption, for instance in the US and the European member nations of the OECD, has not but reached pre-Covid ranges.

Demand for motor gasoline is predicted to say no over the long run.

Dangers to additional progress in demand for motor gasoline may embrace subdued international GDP progress, the growing penetration of electrical autos, and the persevering with pattern towards hybrid work.

Eliminating using fossil fuels in transportation, particularly within the automotive trade, is without doubt one of the key methods aimed toward reaching carbon neutrality within the international economic system. For instance, the EU intends to ban the sale of recent vehicles with gasoline and diesel engines ranging from 2035, whereas the US and China are placing this objective off to a extra distant future. The Worldwide Power Company predicts that automotive autos will stop to drive progress in oil demand by the top of the present decade.

Thus, in 2023, freight charges, though nonetheless near historic highs, progressively declined throughout the 12 months, at the same time as whole demand for seaborne provides of refined merchandise exceeded the degrees that have been recorded over the identical interval within the final six years. The costs of used tankers and the costs of newbuilding proceed to rise, indicating robust demand for such shipments.

In 2024, as we anticipate, spot charges will progressively decline, however might be extremely delicate to geopolitical tensions.

In 2025 the fleet is predicted to increase probably the most since 2016 by way of deadweight. Mixed with a requirement that might rise by a mere 1% or so, this may put additional downward stress on spot charges.

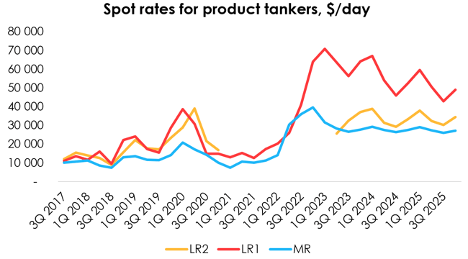

As such, we anticipate quarterly, seasonally-adjusted spot charges for LR2, LR1 and MR tankers to be as follows.

Make investments Heroes

The desk under exhibits common annual spot charges for the three kinds of tankers in query. In 2021 and 2022 the one LR2 tanker in Worldwide Seaways’ fleet operated below a set contract, so spot charges usually are not relevant to those years.

Make investments Heroes

Spot and longer-term contracts

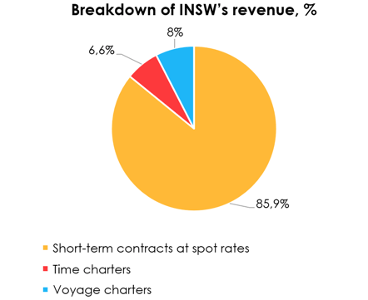

The corporate derives income by offering providers via:

- short-term contracts at spot charges;

- time constitution contracts for intervals starting from just a few months to a couple years;

- voyage charters, that are short-term contracts for the interval of length of every particular voyage.

Over the previous two years income from short-term contracts made up on common greater than 85% of the corporate’s whole income, whereas time charters did about 7%, and voyage charters about 8%.

Make investments Heroes

Mounted-rate time constitution contracts are presently in place for 3 VLCCs (7-year contracts), two Suezmaxes (till 2024 and 2025), one Aframax (till 2026) and 5 MRs (length varies from just a few months to 2 years). Mounted charges are largely decrease than spot charges.

Voyage charters generate income not solely from funds for hiring a vessel but additionally from lightering providers (operations to switch oil and LNG cargoes from ship to ship).

Monetary outcomes

We forecast the corporate’s income primarily based on the variety of income days for every kind of its tankers and the constitution fee of their contracts.

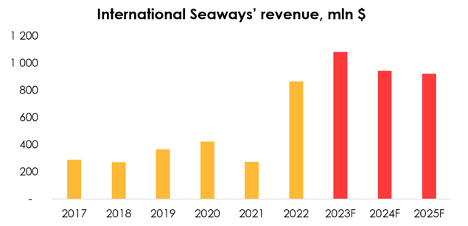

Due to this fact, we anticipate the corporate to earn a income of $1 083 mln (+25% y/y) in 2023, and $945 mln (-13% y/y) in 2024. Income is ready to say no in 2024 on account of expectations that spot charges will fall and the truth that contracts primarily based on these charges make up greater than 80% of the corporate’s whole income.

Make investments Heroes

Working prices

The corporate’s working prices embrace the next:

- Voyage bills – gasoline, port costs, canal tolls, cargo dealing with operations and brokerage commissions paid by the corporate below voyage charters. These bills are subtracted from transport revenues to calculate TCE revenues.

- Vessel and crew bills – crew prices, vessel shops and provides, lubricating oils, upkeep and repairs, insurance coverage and communication prices related to the operation of vessels

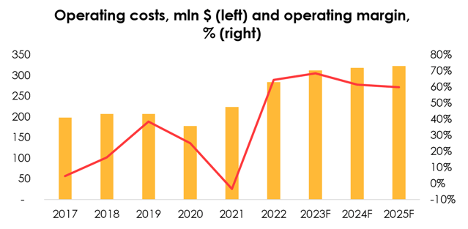

Assuming that bigger/decrease tonnage tankers require proportionally extra/much less funds, we venture working prices primarily based on the common prices per 1,000 deadweight tons, which averaged $8,900 during the last 12 months.

Based mostly on the projected variety of ships in Worldwide Seaways’ fleet and the identified deadweight for every of the tanker sorts, we anticipate bills to function the fleet to succeed in $312 mln (+10% y/y) in 2023, and $319 mln (+2% y/y) in 2024.

We presently know that offers have been signed for constructing two LR1s, with the supply anticipated within the second half of 2025. There’s additionally an choice for 2 contracts to construct further LR1s, with the supply time ranging from the second half of 2025 and ending within the first quarter of 2026.

Make investments Heroes

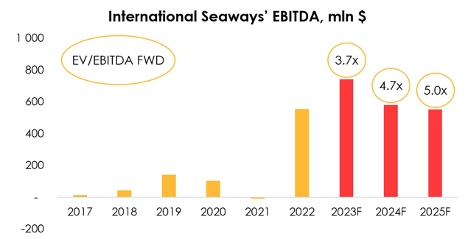

The corporate’s EBITDA is ready to whole $742 mln (+34% y/y) in 2023, and $580 mln (-22% y/y) in 2024. The decline is generally attributable to expectations of decrease income.

Make investments Heroes

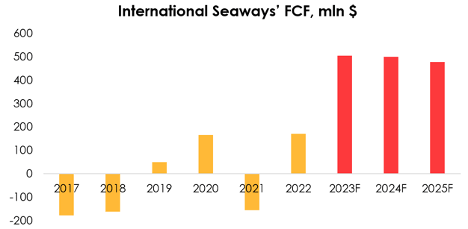

The corporate’s FCF is ready to whole $504 mln (+194% y/y) in 2023, and $499 mln (-1% y/y) in 2024.

Make investments Heroes

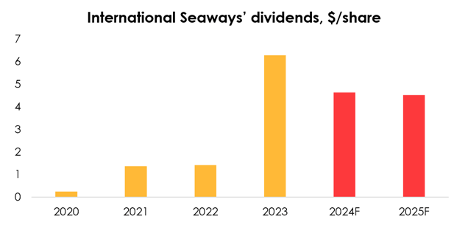

The corporate pays a quarterly dividend of $0.12 per share, however on account of increasing income in 2023, together with its common dividend it 4 instances paid a further dividend starting from $1.13 to $1.88, which corresponded to a dividend yield of 13%.

Assuming the corporate continues to pay further dividends on the again of robust earnings which are pushed by higher-than-historical-average spot charges, we anticipate the dividend yield to be about 9% in 2024 and 2025.

Make investments Heroes

Valuation

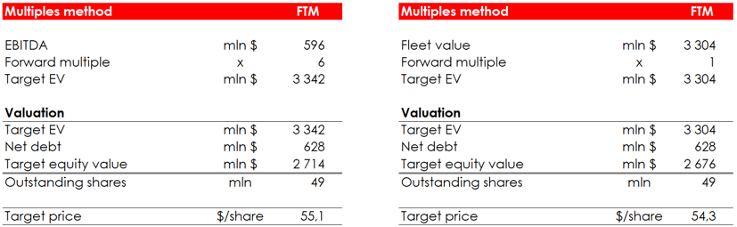

We use two strategies to guage the corporate: the tactic of EV/EBITDA multiples and the EV/market-value-of-the-fleet ratio. The second technique displays that the enterprise worth is simply too low relative to the market worth of its fleet.

The goal worth is $55. The ranking is HOLD.

Make investments Heroes

Tanker assaults within the Crimson Sea

Having studied the corporate’s enterprise and prospects intimately, let us take a look at the burning challenge for transport corporations in latest months – the Houthi assaults within the Crimson Sea – and perceive if Worldwide Seaways’ enterprise is uncovered to the dangers of present occasions.

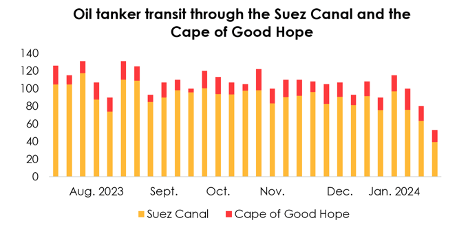

In mid-December, transport corporations responded to the elevated dangers related to the Houthi assaults within the Crimson Sea by diverting vessels to different routes. Regardless of the elevated dangers, there was no vital discount in tanker visitors via the top of December, except for container ships, the variety of which within the Crimson Sea has decreased considerably since December 16. This is because of the truth that, based on MariTrace, greater than half of the vessels concerned in incidents are container ships, and they’re probably the most dangerous. By the top of December, half of the container ships that repeatedly transit the Crimson Sea and Suez Canal have been avoiding the route as a result of menace of assaults.

In December 2023, the motion of tankers carrying crude oil and petroleum merchandise within the Crimson Sea was fairly stable. Based on the Houthis, they assault ships sure for Israel and primarily non-oil cargo. Further prices (vessel bills, insurance coverage prices) weren’t a significant concern for many tanker corporations, because the Crimson Sea remained way more accessible than the route round Africa, however for the reason that starting of the U.S.-led airstrikes, it seems that increasingly more tanker corporations have determined to avoid the risk and transit via the Cape of Good Hope (making the route virtually 1/3 longer) and even stop operations.

Reuters

The U.S. and a quantity of other countries proceed to tighten maritime safety, however growing dangers from air assaults have led a major variety of corporations to refuse transit via the Suez Canal, which is prone to have an effect on and improve spot oil tanker freight charges. Undoubtedly, the disaster within the Crimson Sea is creating an much more tense scenario within the tanker transportation market.

Conclusion

Based mostly on the mixture crude oil and refined product tanker information described above, we anticipate oil tanker demand to exceed provide in 2024 with little potential tanker arrivals.

Because the imbalance guarantees to be smaller than in 2023, spot charges will proceed to say no from peak ranges however will nonetheless be properly above historic values over the previous 3 years, which can assist tanker corporations preserve sturdy monetary outcomes.

After a secure December 2023 for oil tanker visitors via the Suez Canal, a major proportion of corporations have stopped transporting oil via this route in January 2024, which is prone to result in greater spot charges for oil tankers within the close to future.