mbbirdy

Overview

My suggestion for Wynn Resorts (NASDAQ:WYNN) continues to be a purchase score, as I count on progress momentum to proceed into FY24, with a constructive outlook for each the Las Vegas and Macau properties. Observe that I beforehand rated a buy rating for WYNN as I believed WYNN provided buyers a chance to experience on the restoration theme in China and Macau, particularly with the restoration in Macau nonetheless in its first innings. Additionally, the valuation had gotten cheaper, making the upside extra engaging.

Latest outcomes & updates

Whereas the share value painted a unique story (dropping from $110 to $85 earlier than November ’23), WYNN fundamentals continued to enhance, and working metrics in all properties proceed to recommend robust progress momentum, which I feel has satisfied the market that efficiency forward goes to be robust (share value rallied from $85 again to $105 in simply ~3 months from Nov’23 to Feb’24). For 4Q23, WYNN reported consolidated income of $1.84 billion and property EBITDA of $632 million, each beating consensus by $113 million and $69 million, respectively. The outperformance was pushed by robust efficiency in key properties: Las Vegas and Macau.

WYNN carried out very well in Las Vegas, the place it generated $697 million in income and $271 million in EBITDA. This interprets to an EBITDA margin of 38.9%, a 140bps vs final yr. Power was seen throughout the board, with on line casino up 19% y/y, rooms up 28% y/y, F&B up 13% y/y, and Leisure up 12% y/y. For the resort enterprise, each pricing and occupancy metrics additionally replicate a really wholesome degree of demand, the place 4Q23 ADR grew 28% to $631, now 96% above pre-covid degree (4Q19), and occupancy has just about recovered to the per-covid degree as nicely, coming in simply 50bps at 88.9%. As for the on line casino aspect of issues, WYNN efficiency continues to point that any impacts from COVID-19 are over and achieved with, as slot deal with and desk drop had been 79% and 59% larger than 4Q19, respectively. Adjusting for maintain, normalized EBITDA was up 14% y/y. I count on this robust momentum to proceed as administration famous quarter-to-date tendencies for January are just like 2023, wherein they’re seeing robust resort income efficiency. Additionally, the two main occasions (Tremendous Bowl and Chinese language New 12 months) ought to give an enormous enhance in February. On the latter, I imagine this outlook has excessive creditability, given WYNN has double the entrance cash and credit score on the books as of February 2023. As for the Tremendous Bowl, the income and revenue contribution needs to be important contemplating it has an identical ADR as F1 (which was a significant enhance to EBITDA, the place Las Vegas noticed its greatest October, November, and December efficiency). One detrimental level that buyers may ponder is the recent opening of Fontainebleau, as it’s a competitor. I feel it’s nonetheless too early to inform what the online affect is on condition that WYNN is nearer to the Sphere (opened in September 2023), which ought to profit from extra inbound visitors.

Google

The identical was true for Macau, the place WYNN generated $911 million in income and $297 million in EBITDA. Evaluating Macau’s efficiency to pre-covid ranges, hold-adjusted EBITDA has just about recovered as nicely (94% of pre-covid ranges); mass GGR (gross gaming income) and drop had been each above pre-covid at 117% in 4Q23 and 132% in January, respectively. Whereas slot GGR and VIP GGR are nonetheless beneath pre-covid, at 50% and 28%, respectively, I imagine this means potential for elevated progress within the close to time period as Macau catches as much as earlier ranges. Robust prime line and working efficiency contributed vastly to margin enchancment, now 140bps above pre-covid ranges at 32.6%. Importantly, Macau has not misplaced any market share since 4Q19, indicating the resiliency of WYNN’s Macau property.

Turning to Macau, we generated $297 million of EBITDA within the quarter on market share that was per the prior quarter and with 2019. From: 4Q2023 earnings call

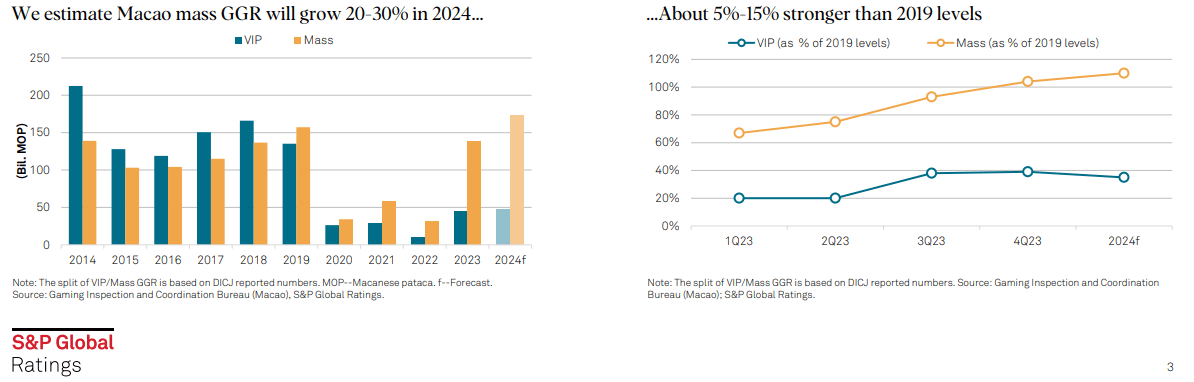

Just like Las Vegas, I count on momentum to proceed into FY24, the place business GGR is anticipated to develop by 5 to fifteen% stronger than 2019 levels. Macro elements just like the depreciation of the RMB and authorities efforts to drive home tourism all bode nicely for the Macau gaming business. Underlying client behaviors are additionally favorable for WYNN, as shoppers are shifting bills away from giant ticket objects to expertise spending (i.e., journey, gaming, and so on.).

S&P

Valuation and danger

Writer’s valuation mannequin

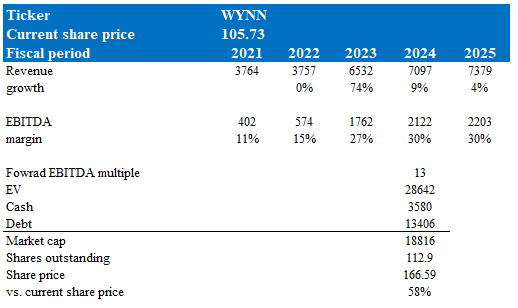

In keeping with my mannequin, WYNN is valued at $166.59, representing a 58% improve. This goal value is predicated on a consensus progress forecast for the following 2 years (9% and 4%). I imagine consensus estimates are affordable given FY23 did loads higher than I anticipated (11 factors outperformance vs. my expectation for 63% progress), which creates a harder comp for FY24 and FY25. The robust 4Q23 efficiency and outlook for WYNN in FY24 additionally assist an elevated FY24 efficiency earlier than reverting again to mid-single-digit progress, in keeping with its historic common progress (from post-subprime to pre-covid). Equally, due to the weaker EBITDA margin efficiency (reported 27% in opposition to my 29% expectation), I’ve tapered my expectation to consensus estimates of 30% for FY24 and FY25. Nevertheless, I’ve taken on a extra aggressive a number of assumption, in that I now assume WYNN will commerce at 13x ahead EBITDA (its common) vs. my earlier expectation of 12x due to the efficiency to date, momentum into FY24, and market sentiment (as seen from the inventory value rally).

Headline year-on-year comparability could possibly be a danger that impacts inventory sentiment for FY24, as administration expects harder comparisons as FY23 was a very robust yr, boosted by the F1 occasion. As well as, the worsening of macroeconomic circumstances may show to be way more than what WYNN can deal with if shoppers pull the plug on discretionary spending.

Abstract

My bullish suggestion on WYNN stays. WYNN’s fundamentals display sturdy progress momentum in each Las Vegas and Macau properties. 4Q23 performances exceeded consensus expectations, significantly in Las Vegas, the place all key segments exhibited power. Macau, too, showcased resilience, sustaining market share and indicating potential for elevated progress. With favorable macro elements and client spending tendencies within the gaming business, I imagine WYNN is positioned for a continued constructive trajectory into FY24. Whereas headline year-on-year comparisons and macroeconomic uncertainties pose dangers, the general outlook stays optimistic for WYNN’s efficiency.