Love Worker/iStock by way of Getty Photographs

Xeris Biopharma Holdings (NASDAQ:XERS) is up 88% (YoY) and the inventory value is buying and selling simply 23.5% shy of the 52-week excessive of $3.07. It has been 4 years for the reason that U.S. FDA authorized Gvoke, the prefilled (ready-to-use) glucagon drug for the therapy of hypoglycemia in diabetes sufferers (from 2 years and above). Since then, and whereas contemplating the commercialization efforts of Keveyis and Recorlev; Xeris has been capable of develop its income from $2.7 million in 2019 to $152.7 million within the 12 months trailing to September 2023.

Thesis

Xeris Biopharma continues to point out nice potential in balancing its commercialization efforts into 2024 whereas sustaining optimistic working capital administration. By stable partnerships, the corporate has been enhancing its proprietary applied sciences: XeriSol and XeriJect to assist in the supply of medicine to sufferers making them comparatively engaging. Additional, Xeris continues to harness the ability of innovation with its new product candidate, Levothyroxine; which is already in its Section 2 research.

Transformative Diabetic Drug growth

I imagine Xeris has heightened curiosity within the growth of ready-to-use glucagon choices that dethrone the necessity for reconstitution. We have already got a minimum of two different corporations which have produced such a therapy together with XERS. Market chief, Eli Lilly and Firm (LLY) developed Baqsimi which was authorized by the FDA in 2019. In its Q3 2023, report, LLY said that, out of the $1.42 billion income collected within the 9 months ending September 2023, it realized about $579 million from the sale of its “rights for Baqsimi to US firm, Amphastar Pharmaceuticals.” You will need to observe that whereas LLY has a number of diabetes therapies, it recorded larger gross sales for Baqsimi exterior the US (within the three months to September 2023) as in comparison with US gross sales. We should remember the fact that XERS’ Gvoke gross sales are predominantly within the US.

Novo Nordisk additionally developed Zegalogue- a glucagon analogue which like Gvoke, is obtainable as an auto-injector (injection). In distinction, Baqsimi (in contrast to Zegalogue and Gvoke) is run within the nasal space within the type of glucagon powder. LLY’s “glucagon emergency kit” and Novo Nordisk’s “GlucaGen HypoKit” are conventional hypoglycemia glucagon kits that have been first approved in 1998 to be used with no age limits. Nevertheless, Xeris Biopharma’s Gvoke HypoPen and the pre-filled syringe (PFS) introduce what I might time period the fashionable period of hypoglycemia therapy for diabetes sufferers. The HypoPen is run utilizing an auto-injector as a liquid-stable drug formulation (the primary of its sort) with the identical formulation current within the PFS. What’s distinctive with Gvoke (the fashionable hypoglycemia therapy) is that it removes the necessity for premixing- because the liquid formulation is already in a secure state. This function permits straightforward self-administration.

In my estimation, world Gvoke gross sales will hit $400 million per 12 months shortly, contemplating there are about 38.4 million affected by diabetes within the US alone. Alongside the PFS and HypoPen. XERS additionally has the Gvoke Package and the Ogluo (glucagon) which was authorized on the market and utilization within the European Union by EMA and MHRA. The cost of 1 unique Gvoke equipment is about $373 per vial (which has 1ml of 1mg/0.2ml). The generic model prices lower than $300 per vial.

XERS additionally has the proprietary XeriSol and XeriJect growth applied sciences which for my part are revolutionary. The corporate attributes its capability to create the rescue, “ready-to-use, stable and highly concentrated” formulations to those two applied sciences. They virtually resolve the solubility/stability limitations which have plagued different medication by offering handy storage, and the general subcutaneous administration. XERS said that it owned about 174 world patents in regard to its “ready-to-use formulations eligible for expiry until 2036.

What about the management?

Xeris Biopharma has been on steady growth ever since Paul Edrick took over as CEO of the company in 2017. He took the company public in 2018 and has since raised about $253 million in equity financing having overseen multiple clinical and pre-clinical studies. However, the commercialization of its key drug candidates adds the icing to the cake proving the success of his sales background. In terms of decision-making, Paul is the right man to steer the company to growth in productivity and operational efficiency.

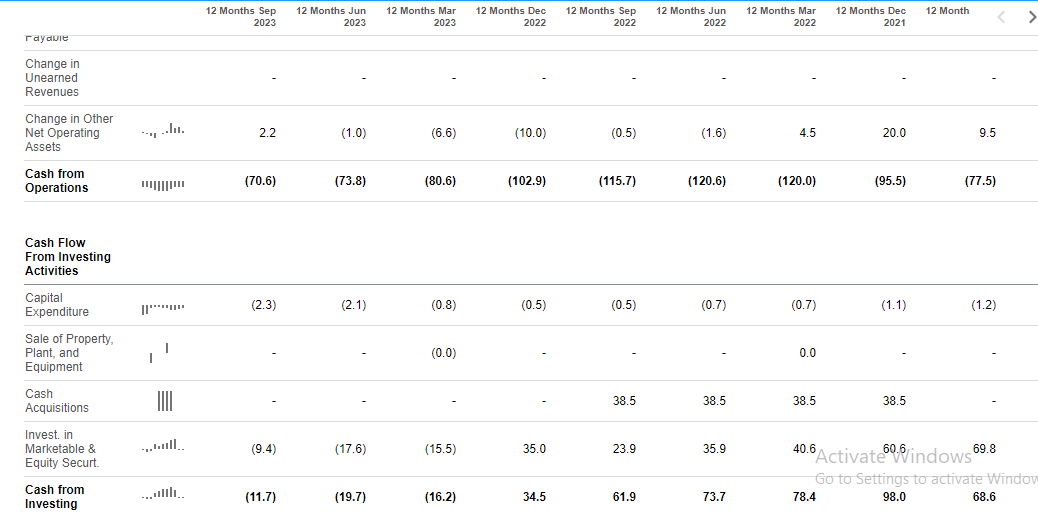

Xeris has reduced its annual net loss from $125.6 million in FY 2019 to $61.8 million in the 12-month trailing period ending September 2023. Additionally, in the 9 months ending September 30, 2023, Xeris’ management used $54.5 million in its operating activities, representing a 37.2% (YoY) decline from $86.8 million used in the same period in 2022. This reduction was attributed to the management’s lower usage of its working capital in 2023. The same decrease was witnessed in the CapEx with a~$5 million reduction. Paul and his team prioritized more short-term investments in the period that involved operational output as opposed to reinvestments. I expect the management to balance operations and CapEx heading into 2024 which will lower the strain on equity financing while growing commercial activities to boost sales.

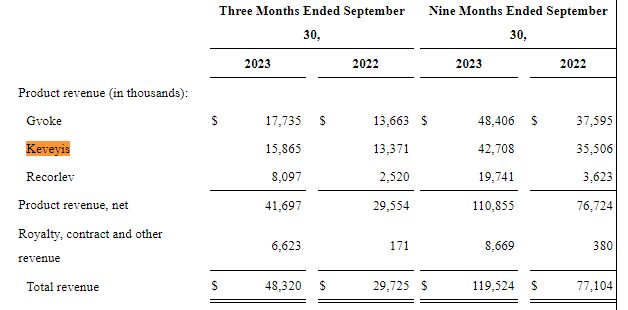

It will come as no surprise if Xeris decides to follow LLY in the sale of its Gvoke rights. I make this presumption since XERS relies on third parties to sell and distribute all its drug products. At the moment, Gvoke is the most attractive drug product in terms of revenue generation. This commercialization procedure holds for Keveyis and Recorlev as well. XERS has recorded continuous revenue realization from 2022 to 2023 in its product sales. Keveyis was approved in 2015 as the first therapy treatment in the US for hyperkalemic and Primary Periodic Paralysis (PPP). It was the second-best-selling product for XERS after Gvoke raking in $15.9 million while Gvoke realized $17.7 million in the three months ending on September 30, 2023.

Seeking Alpha

As seen above, XERS is growing its revenue away from product development through licensing, royalties, and other contracts. It grew this revenue category by 3,773% (YoY) in the three months ending on September 30, 2023.

New Developments into 2024

Xeris’ focus into 2024 will also be on XP-8121, an injection of levothyroxine used for the treatment of hypothyroidism. Various drugs have been approved by the US FDA for the treatment of thyroid gland problems. Among the drugs approved include Levoxyl originally produced by Jones Pharma which was acquired by King Pharmaceuticals (at a valuation of $3.6 billion). It was finally acquired by Pfizer as a fully-owned subsidiary in 2010. Statistics indicate that at least 20 million people are affected by thyroid gland diseases globally with the US registering more than 13 million patients who are “hormone replacement therapy.”

One unique feature of Levothyroxine-XP-8121 is that it is being developed as a once-weekly subcutaneous dose while other common hypothyroidism treatments are daily treatments in the form of tablets. For example, the Unithroid drug tablet, developed and marketed by Amneal Pharmaceuticals is an “oral single daily dose.” Tirosint developed by IBSA Pharma is also a daily dose that requires patients to refrain from meals before administration.

By September 2023, XERS had already begun its phase 2 dosage study to assess the patient’s reaction after receiving Levothyroxine. I am looking forward to its Phase 3 study by 2025 when it will engage with the FDA before commercialization.

Dangers to the Enterprise

Excessive money burn charge into 2024

In the 12 months trailing to September 2023, Xeris used up $82.3 million in both operating and investing activities.

Seeking Alpha

This amount was used against the cash balance of $66 million recorded as of September 30, 2023. Calculations indicate that the cash runway for Xeris Biopharma is nine (9) months before the current cash balance runs out. Without considering any other financing option, XERS will have sufficient cash to run until June 2024 or H1 2024. The company will need additional financing for H2 2024.

Use of third-parties

As noted earlier, XERS relies on third parties to supply and sell its lead drug products whose delayed lead times may affect the company’s revenue realization. This aspect also means Xeris, on its own, has limited sales, supply, and other commercial logistics that would enable it to rapidly increase revenues in a short time.

High cumulative net loss over the years

Xeris’ accumulated deficit has increased 8.8% (YoY) to $603.6 million in the nine months to September 2023 from $554.8 million last year. While the company is looking towards a cash-flow positive situation, it is yet to break even in regard to expenses outweighing profits.

Valuation

For valuation, XERS’ forward price-to-sales ratio is 2.01 against the industry average of 4.17 (indicating a difference of -51.73%). This difference shows the stock is slightly undervalued with an upside potential above 50% into 2024. However, the 12-month trailing price-to-book ratio is 81.27 against the industry average of 2.27 (a difference of 3,475.56%). We may also see a downside especially if the company does not work to lower its accumulated deficits and minimize losses into 2024.

Backside line

In the meanwhile, XERS is a maintain however, I’ll revise it to purchase and develop my place as soon as it lowers its accumulative deficit in addition to the operational bills. It’s going to even be very important to see the way it resolves its excessive money burn by H2 2024 with strategic issues earlier than taking Levothyroxine to Section 3. Nonetheless, XERS comes out as a gorgeous inventory combining diabetes therapy, and paralysis/thyroid gland remedy in its manufacturing performs. The corporate’s administration has labored in direction of the commercialization of its three main drug merchandise since 2017. Regardless of the excessive gathered deficits through the years, XERS has steadily grown its revenues whereas exploring different new drug candidates akin to Levothyroxine. It will likely be very important for the corporate to enhance its operational efficiencies to decrease bills towards earnings to stability its money circulation into 2024. I’ve additionally thought of the concept the administration could determine to promote its main product to extend its money circulation into the longer term.