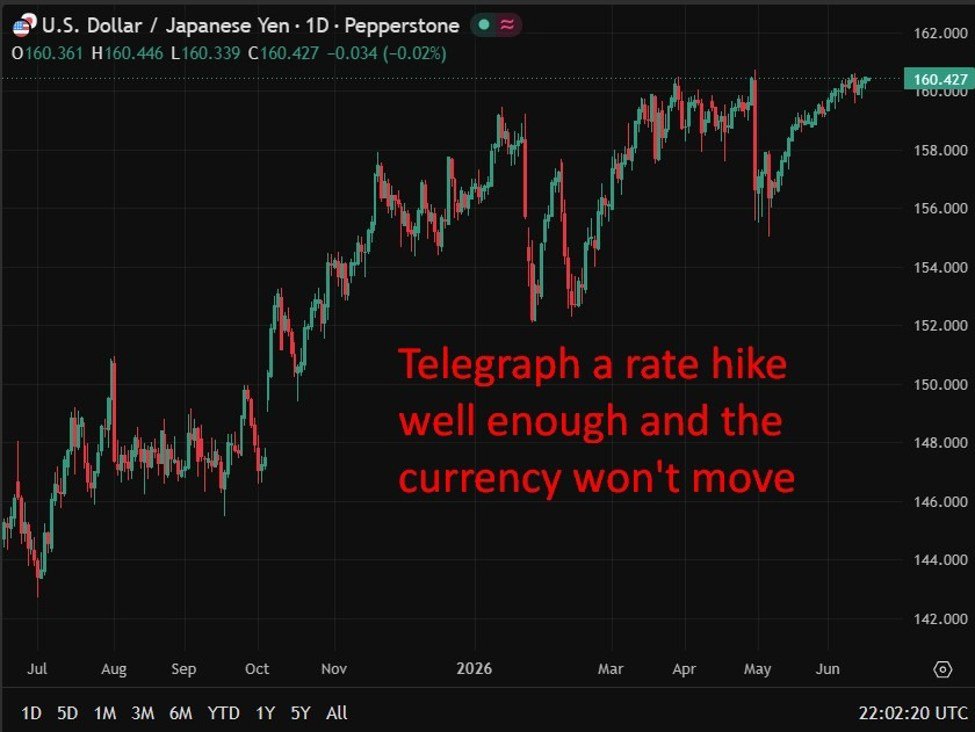

The yen’s inability to rally on the back of a rate hike underscores how deeply entrenched bearish positioning has become, with leveraged funds having built up significant short exposure over the past month. Intervention risk is rising again as dollar/yen approaches levels that previously triggered official action, with the 161-162 zone flagged as the likely threshold. Falling energy prices from the reopening of the Strait of Hormuz offer a partial offset for Japan’s import bill and could modestly support the currency, but analysts caution this dynamic also bolsters global risk appetite, which in turn sustains carry trade demand and limits yen upside.

—

The yen remained weak after the BoJ raised rates 25bp to 1.00%, with analysts warning of intervention risk near 161-162 and a disorderly carry trade unwind seen as unlikely given the well-telegraphed move.

Summary:

Sources: MUFG; analyst commentary

- The BoJ raised its policy rate by 25 basis points to 1.00% but gave no strong signal on the timing of the next move, according to MUFG

- MUFG said the yen’s failure to strengthen after the hike keeps pressure on Japanese authorities to intervene again

- Leveraged funds have increased short yen positions significantly over the past month, adding to concerns about speculative selling pressure, MUFG noted

- The US-Iran deal to reopen the Strait of Hormuz should ease some fundamental selling pressure on the yen by lowering energy prices and reducing expectations for Fed rate hikes, per MUFG

- If the BoJ holds off on another hike until December, the yen will remain in negative real interest rate territory and continue to function as a carry trade funding currency, other analysts warned

- A repeat of the sharp carry trade unwind seen in August 2024 is considered unlikely given the hike was well telegraphed and largely priced in, analysts said, though dollar/yen risks extend to the 161-162 zone where further intervention is probable

The Japanese yen failed to find meaningful support after the Bank of Japan raised its policy rate by 25 basis points to 1.00%, leaving the currency under pressure and keeping the prospect of official intervention firmly in play, analysts said.

MUFG said the central bank gave no firm steer on the timing of its next move, and that the yen’s lack of response to the hike would sustain pressure on Tokyo to step back into the market. The bank noted that leveraged funds had been aggressively building short yen positions over the past month, fuelling concern that speculative flows, rather than fundamentals, are driving the currency’s weakness.

One potential source of relief identified by MUFG is the US-Iran agreement to reopen the Strait of Hormuz. Lower energy prices would reduce Japan’s import costs, a structural drag on the yen, while also dampening expectations for further Federal Reserve tightening, which has kept the interest rate differential between the US and Japan wide and unfavourable for the yen.

Other analysts flagged that if the BoJ refrains from hiking again until December, Japan will remain in deeply negative real interest rate territory when adjusted for inflation, preserving the yen’s role as the preferred funding currency for carry trades. With volatility expected to stay subdued through the northern summer, renewed appetite for carry strategies could push dollar/yen above 160.70, with the 161-162 zone identified as the area where intervention becomes most likely.

Despite the parallels with the August 2024 episode, when a BoJ rate increase triggered a violent and rapid unwinding of yen carry trades, analysts said a repeat of that dislocation looks unlikely on this occasion. The current hike was extensively communicated in advance and was largely anticipated by markets. Lower oil prices, while supportive of Japan’s terms of trade, also underpin global risk sentiment and help sustain equity market momentum, factors that limit the conditions needed for a disorderly reversal.