JHVEPhoto/iStock Editorial by way of Getty Photos

Utilizing our money move returns on investments based mostly instrument, Yum Manufacturers (NYSE:YUM) seems prominently on our listing as a high-quality, investment-grade firm. Utilizing a traditional valuation matrix in addition to our DCF-based valuation instruments, it might be undervalued by as a lot as 24%. It’s a secure worth compounder reasonably outpacing the S&P 500 over 10 years. We provoke with a purchase ranking.

The Firm

YUM is the world’s largest restaurant chain with over 57,000 retailers throughout 155 nations. Its principal manufacturers embrace KFC, Pizza Hut, Taco Bell, and The Behavior Burger Grill. As of the 12 months ending Dec 2022, from whole income of $6.8bn, KFC contributed $2.8bn, with Taco Bell $2.4bn, Pizza Hut $1.0bn, and Behavior Burger $0.6bn.

The Q3 results launched on 1 Nov noticed income improve by 4% to $1.71bn however missed its predicted goal of $1.77bn. Revenues excluding international forex translation, grew 10%. EPS, nonetheless, beat targets and got here in at $1.44 in comparison with analyst expectations of $1.27. This is a rise of 32% over the identical interval final 12 months.

David Gibbs, CEO & Director stated within the Q3 earnings call:

…our business has softened somewhat bit, however the business is doing higher than most industries….

Additionally, Gibbs expects to fulfill and exceed long-term development targets:

Our twin development engines, KFC Worldwide and Taco Bell U.S., led the best way, with KFC exhibiting broad-based power throughout each developed and rising markets. With our sturdy year-to-date efficiency, we proceed to count on that our full-year 2023 outcomes will outperform all features of our long-term development algorithm.

YUM is well-positioned in its phase and is a wonderful defensive firm.

Consensus estimates EPS for FY23 to be $5.34, and FY24 $5.83, a rise of 18% & 9%. Revenues are anticipated to extend somewhat slower at 4.5% and seven.9% for FY23 and FY24.

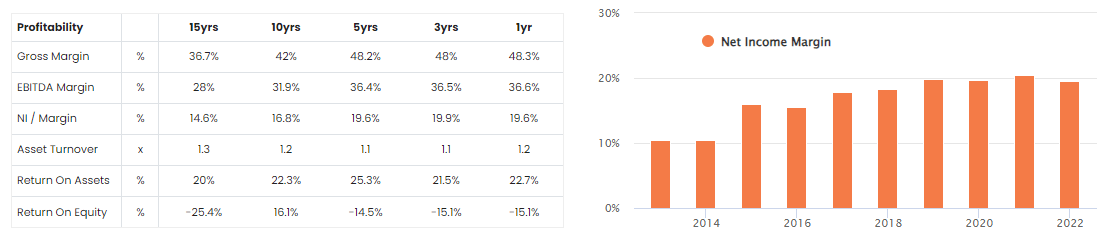

This equates to a internet revenue margin of 21% for each FY23 & FY24.

That is an enchancment from the 5-year internet revenue margin common of 19.6%.

Yum Manufacturers Profitability (ROCGA Analysis)

On all measures, we see the corporate has made enhancements in profitability. The enhancements will be seen within the momentum the place the short-term averages are higher than the longer-term averages, particularly because the spinoff of Yum China (YUMC) in 2016. Asset turnover is a measure of effectivity and is calculated by dividing the revenues by common belongings. Merely put, it measures the quantity of belongings used to generate income. For the reason that spinoff, YUM has additionally improved its asset turnover from 0.8x to 1.2x. One other very comparable ratio we like to make use of is the gross asset turnover. This makes use of an adjusted and comparable measure of belongings employed as a substitute of the e-book worth. These have additionally improved from 0.69x in 2016 to 1.01x in 2022.

Beneath we’ll use our affiliate’s returns on cash-generating belongings (ROCGA), a technique based mostly on money move returns on investments. It’s a measure of financial efficiency. Extra info on how ROCGA is calculated together with gross belongings, gross money, and money move returns on investments will be present in Bartley Madden’s paper “The CFROI Life Cycle“. Bartley Madden has been a big contributor to the Money Move Returns on Funding methodology.

YUM is extremely cash-generative and can also be rising modestly. It has been diligent and has returned extra money to its shareholders. As a lot as $9bn has been paid out as dividends and share repurchases over the previous 5 years and $22.3bn over 10 years. Shares excellent have gone down from 452m in 2013 to the present 280m, down 38%. With modest development and share buybacks, income per share has elevated steadily at over 7% CAGR over 7 years.

Thus far we now have seen modest development, enhancing margins, and higher asset turnover, all pointing to enhancing returns.

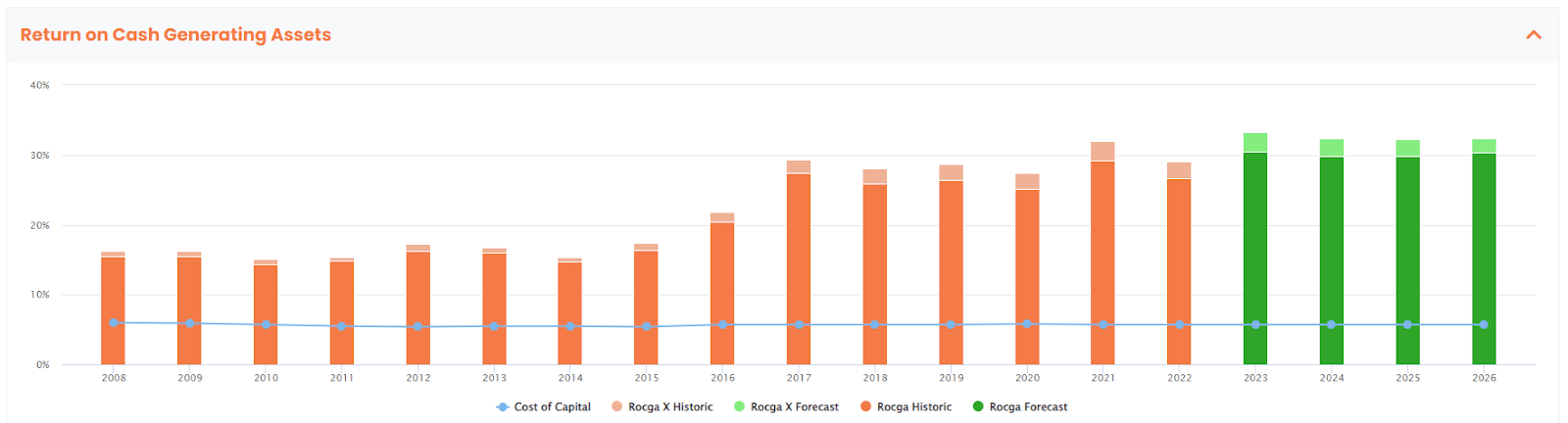

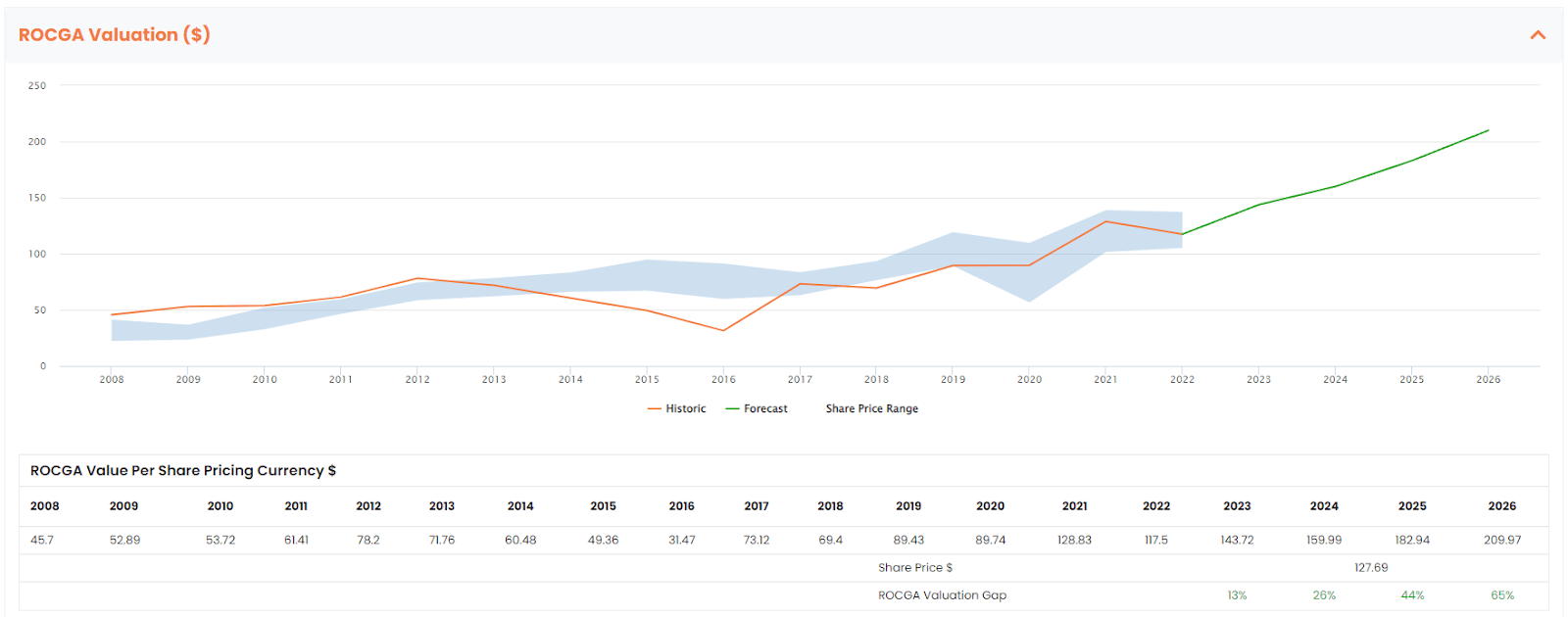

Yum Manufacturers Returns On Money-Producing Property (ROCGA Analysis)

For the reason that spin-off of Yum China in 2016, we now have seen returns on cash-generating belongings enhance. For the forecast years, we use consensus EPS.

YUM additionally has a robust steadiness sheet with an curiosity cowl of 4.2x and internet debt to EBITDA of 4.9x. Dividend yields have been roughly 2%, not forgetting the share repurchases.

Dangers

Inflation is receding, however an uptick would in flip put strain on prices of products offered and wage inflation. A macroeconomic slowdown may have a blended impact on the restaurant business with extra individuals deciding to cook dinner and eat at residence and a few transferring all the way down to the cheaper meals chains. YUM faces international change danger, however we predict this may solely be transitory, can go each methods and shouldn’t have an effect on the long-term prospects.

Standard Valuation

YUM can also be buying and selling at a slight low cost compared to McDonald’s (MCD) which is buying and selling at a PE of twenty-two.6x (FY24) and Chipotle Mexican Grill (CMG) 41.7x (FY24). CMG’s greater development can partially clarify the upper valuation ratio.

For FY24, YUM is buying and selling at 21.9x. That is the bottom since 2012 when the PE was 20.1x. The 5-year common historic PE ratio was 25.9x and FY24’s 21.9x presents a big low cost to historic averages.

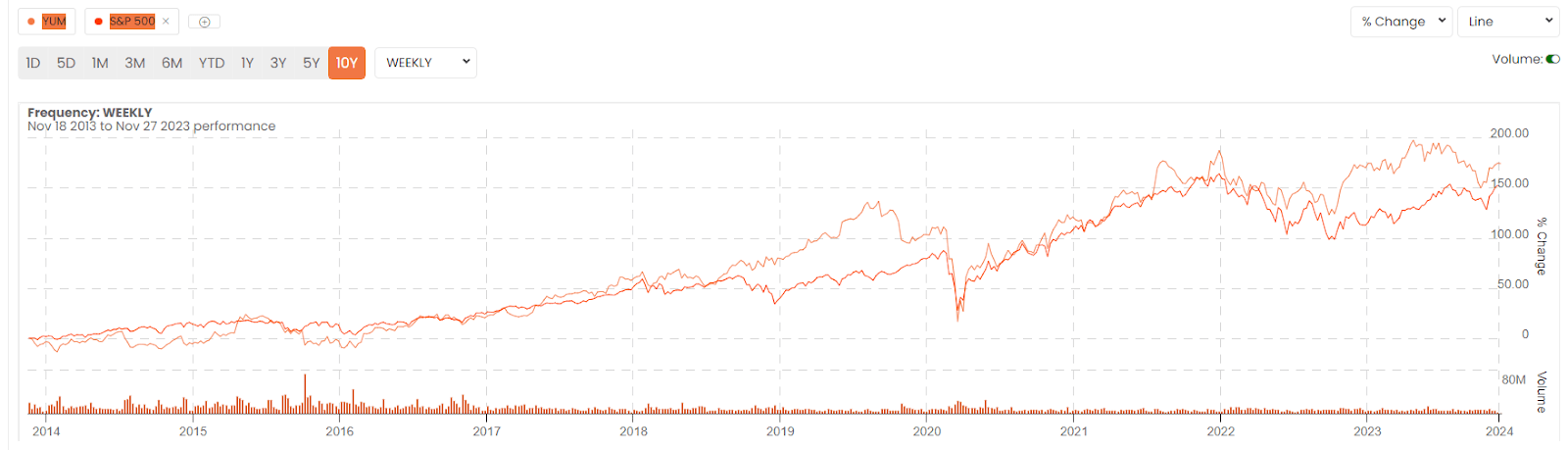

Yum Manufacturers & S&P 500 10-year Efficiency (ROCGA Analysis)

Trying on the 10-year efficiency, the corporate has stored tempo with and barely outperformed the S&P 500.

Money Move Returns On Investments Valuation

To worth an organization, we use our affiliate ROCGA Analysis’s quantitative and systematic money move returns on investments based mostly DCF valuation instruments. Step one includes modeling the corporate, back-testing the valuation for correlation with the historic share costs, and utilizing that very same mannequin to forecast ahead.

Worth is a operate of returns and development in cash-generating belongings. The whole worth of the corporate is the current worth of present belongings and the current worth of development belongings.

Yum Manufacturers Default ROCGA Valuation (Chart created by the creator utilizing ROCGA Analysis platform)

The blue band above represents the share worth highs and lows for the 12 months and the orange line is the DCF model-driven historic valuation. The inexperienced line is the forecast warranted worth derived utilizing the identical mannequin together with consensus earnings and default self-sustainable natural development. Self-sustainable natural development is a ratio of investable free money as a ratio of invested capital. Funding will be by way of acquisitions, natural, or self-investments by way of share buybacks.

The valuation mannequin above is extremely correlated to the share worth vary and we use the identical mannequin to mission ahead with consensus EPS. The share worth vary and the model-driven valuation didn’t correlate nicely through the transitory spin-off interval of 2015-2016.

Yum Manufacturers has always generated worth, as evident within the share worth efficiency and the constant improve in ROCGA worth per share. Our mannequin predicts this can proceed and for FY24, YUM might be undervalued by as a lot as 24%.

Conclusion

Yum Manufacturers is a high-quality, value-generative investment-grade firm. It’s buying and selling at a reduction to its historic PE averages and from a money move returns on investments based mostly DCF evaluation. We provoke with a purchase ranking.