SDI Productions

Abstract

Following my coverage of Zoom Video Communications (NASDAQ:ZM), for which I beneficial a maintain score as I didn’t see any indicators of development restoration within the close to time period on account of weaker demand from SMBs (on account of them shutting down) and gross sales cycle normalization, this publish is to supply an replace on my ideas on the enterprise and inventory. I stay on the sidelines (hold-rated) for ZM because the macro scenario remains to be unfavorable in the direction of ZM. I acknowledge the underlying development drivers—Zoom Telephone and Zoom Contact Heart—that ZM has, and they’re actually doing properly. Nonetheless, till headline development begins to point out higher numbers, I simply don’t see how the inventory will work within the close to time period (the inventory just about sidelined for the previous 12 months).

Funding thesis

Whereas administration has raised its FY24 steering, from the current 3Q24 efficiency, I can inform that ZM remains to be going through headwinds from the macroclimate. Income development continues to decelerate for the 8th straight quarter, rising solely by 4.9% in 3Q24. As well as, the explanation behind the weak whole deferred income information (-6% to -8%) is one other essential piece of proof that prospects are nonetheless holding again on spending. Particularly, prospects try to handle their money to make the most of an setting with excessive rates of interest, which is why billing frequencies on enterprise offers are lowering.

For This autumn, we count on deferred income to be down 6% to eight% year-over-year, partially pushed by shorter billing frequencies on Enterprise offers arising from the excessive rate of interest setting. 3Q24 earnings call

I is likely to be oversensitive on this, however the greater implication from that is that it suggests enterprises usually are not in a rush to undertake ZM’s product choices (they clearly worth money curiosity greater than investing in growth-oriented ZM merchandise). A further issue contributing to the weak deferred income information, which signifies a weak spending setting, is the truth that contract renewals are being obtained with decrease gross sales worth.

we anticipate that as we get by way of the tip of this yr, we have moved by way of most of these transitions the place organizations have finished their very own reductions and are aligning their licenses to that. 3Q24 earnings name

It is because prospects are downsizing their contracts on account of layoffs. Apart from the plain impression that it will have on development, my concern is that there is likely to be extra contract renewal headwinds coming forward – ZM goes to see peak contract renewal season in 1CQ2024 which, primarily based on the current developments, means that these contracts are going to be renewed at decrease worth as companies have lesser want after the layoffs.

So the opposite factor, as a reminder, proper, we will have an enormous renewal cycle in Q1, after which that is the height. 3Q24 earnings name

. If my assumption is correct, near-term renewals ought to be damaging for development because of the downsized contracts. This contract renewal headwind also needs to proceed to stress the NRR (web retention fee) for Enterprise prospects (which declined from 109% in 2Q24 to 105% in 3Q24). The information that Fed goes to chop fee in 2024 is unquestionably constructive for ZM as the price of doing enterprise is now lesser, which suggests companies can now afford to rent extra workers for development. Nonetheless, I don’t assume the impression will likely be fast as companies are more likely to stay cautious and maintain on to money (guarantee a robust stability sheet) till the financial system outlook is clearer.

So anyplace from one simply type of 5 years. So common finally ends up being round 3. So I imply the fact is we all know that almost all had the chance to resume in FY24. 26th Needham Growth Conference

That mentioned, there are 3 facets of ZM enterprise that I feel have potential to assist ZM cushion this macroclimate: Zoom Telephone and Zoom Contact Heart. Zoom Telephone remains to be a major development driver for the corporate, which is strategically concentrating on upselling Zoom platforms with bundled merchandise. For context, administration reported a 330% year-over-year improve within the variety of Zoom One bundle customers, together with telephone customers. Bundling works very properly for ZM as a result of it considerably elevates the client expertise as an entire (the bundle contains options like a whiteboard, scheduler, telephone, and chat). The general impression is that it helps enhance buyer retention and push ZM deeper into the operational workflow processes of its buyer base. People are ordinary creatures; the extra they use ZM, the extra acquainted they’re, and the much less possible they’re to change resolution suppliers. Zoom Telephone ought to proceed to see traction as ZM has the intention to roll out a down-market telephone providing, additional reducing the adoption barrier. As for Zoom Contact Heart, as of 3Q24, it has reached round 700 prospects, which is 40% sequential development (200 additions from 2Q23), and Zoom Digital Agent prospects practically doubled quarter over quarter. I imagine ZM’s choice to roll out this product is well timed, as a whole lot of corporations need to cut back prices (particularly with the excessive wage setting), and one obvious method is to outsource contact centers. And the explanation ZM is ready to win market share, in my view, is as a result of it has a big buyer base that’s already utilizing a few of its merchandise. This makes it simple for ZM to bundle every little thing collectively at a cheaper price to encourage prospects to make use of them.

Valuation

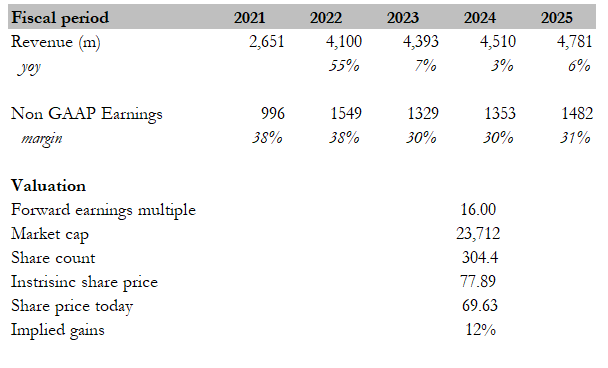

Personal calculation

My goal value for ZM, primarily based on my mannequin, is ~$78. My revised assumptions are as follows:

- FY24 ought to develop by 3% as an alternative of my prior 2%, reflecting administration’s FY24 new steering.

- FY25 development is adjusted upwards by 100 bps to mirror the 100 bps better-than-expected efficiency. I proceed to count on development restoration in FY25 because the macro scenario ought to stabilize, and ZM has two growth-driving merchandise.

- Earnings margins stay flat in FY24 as development is modest, however FY25 ought to see some type of margin growth as income development recovers.

My valuation methodology for ZM remains to be to check ZM towards the broader market (SPX index) as a result of there usually are not sufficient listed friends which might be direct rivals. The ratio between ZM and the SPX index has seen a downtrend ever since ZM development began to sluggish, touching 0.73x as we speak. As I count on development to recuperate again to mid-single-digits, this ratio ought to see some type of restoration too. The final time ZM was rising at mid-single digits, the ratio was round 0.8x. Attaching that 0.8x to the present SPX a number of (20x ahead PE), ZM ought to commerce at 16x.

Danger

No matter product development drivers ZM has as we speak might not impression the inventory value in any respect if the general macro scenario will get worse. It is because the market goes to cost in additional demand deterioration, which can additional erode deferred income development, trigger additional NRR compression as contract renewals come up, and in the end impression headline development figures.

Conclusion

My maintain suggestion stays for ZM. Whereas Zoom Telephone and Zoom Contact Heart present promise, the macroeconomic local weather stays a major burden. Particularly, the weak whole deferred income information and contract renewals with decrease gross sales worth and downsized contracts are indicators of weak development within the near-term.