Sundry Photography

The sentiment in the market right now is undoubtedly cautious. Amid the backdrop of higher interest rates and an uncertain macro recovery, the best strategy is to lean in more on “growth at a reasonable price” stocks, allocating more of your portfolio toward value-oriented tech.

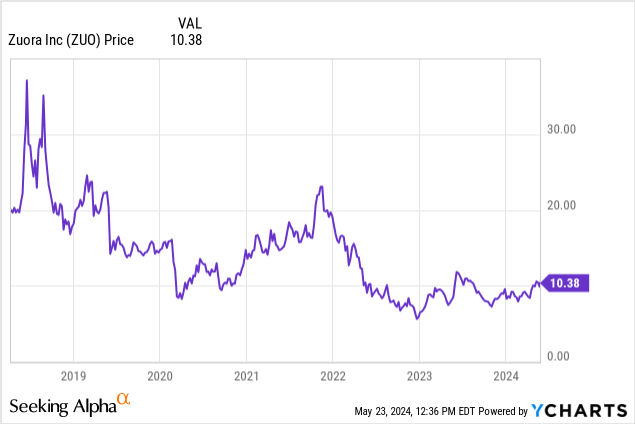

And while these names are far from exciting, companies like Zuora (NYSE:ZUO) are a perfect long-term hold that will have little correlation to how the broader markets do. After years of lagging behind its tech peers, shares of Zuora have shot up nearly 20% this year, buoyed by an especially strong Q1 earnings print that defied expectations.

The fact remains that Zuora is one of the cheapest small/mid-cap enterprise software companies in the market, trading at a low single-digit multiple of revenue. And while it is certainly a niche product, it has few direct competitors that exactly address its use case of powering billings solutions for fellow subscription companies. It recently doubled down on its niche by making a tuck-in acquisition of a company called Togai, which helps businesses build metered and usage-based pricing configurations and perfectly complements Zuora’s existing suite of billing management tools.

I last wrote a very bullish opinion on Zuora in March, when the stock was still trading in the ~$8 range. After a 20%+ rally and a strong Q1 earnings print, I remain bullish on Zuora’s prospects for the remainder of the year and encourage investors to stay long. In my view, the Zuora rally is just getting started.

As a reminder for investors who are newer to this stock, here’s my updated long-term bull case on the company:

- Zuora caters to subscription-based business models and is the category leader in this niche. Given the fact that more and more businesses are adopting this type of model, Zuora’s base of potential customers has widened significantly. Zuora’s uniqueness in this regard is also important to point out: companies can choose a regular ERP, but Zuora’s subscription-focused solutions help to address common pain points. Its recent acquisition of Togai, a billing tool for metered and usage-based pricing, further expands its reach.

- Improving net retention rates above 100% as Zuora grows along with its customers. Zuora’s net revenue retention rates are still above 100%, indicating net upsell. As Zuora’s clients grow their subscriber bases, so does Zuora’s opportunity to monetize and grow alongside its customers. The company has noted that upsells have hit a “record pace”, and highlighted several key milestones, like GoPro’s subscription-based storage and insurance program (a key feature of the company’s planned turnaround) hitting one million subscribers.

- Gross margin leverage. A better subscription versus professional services revenue mix has helped Zuora lift its gross margin profile to life-to-date highs, reversing a common concern investors had with this stock at the time of its IPO.

- Ripe for a takeover, especially at low valuations. While I never like to base any investment decision based on high hopes that the company will get acquired, Zuora checks off a lot of boxes for being acquired: it’s small with just a ~$1.5 billion market cap; it offers a very unique product that many larger software companies may want to get their hands on, especially during times when organic growth is fading; and it has positive pro forma operating margins.

- Strong cash position. The company has over $0.5 billion of cash and just shy of $0.2 billion of net cash (after netting off debt) on its books, giving it ample financial flexibility to pursue acquisitions of its own and other growth opportunities.

In my view, Zuora’s Q1 upside is a precursor to a much longer rally. Stay long here and keep riding the recent upward wave.

Q1 download

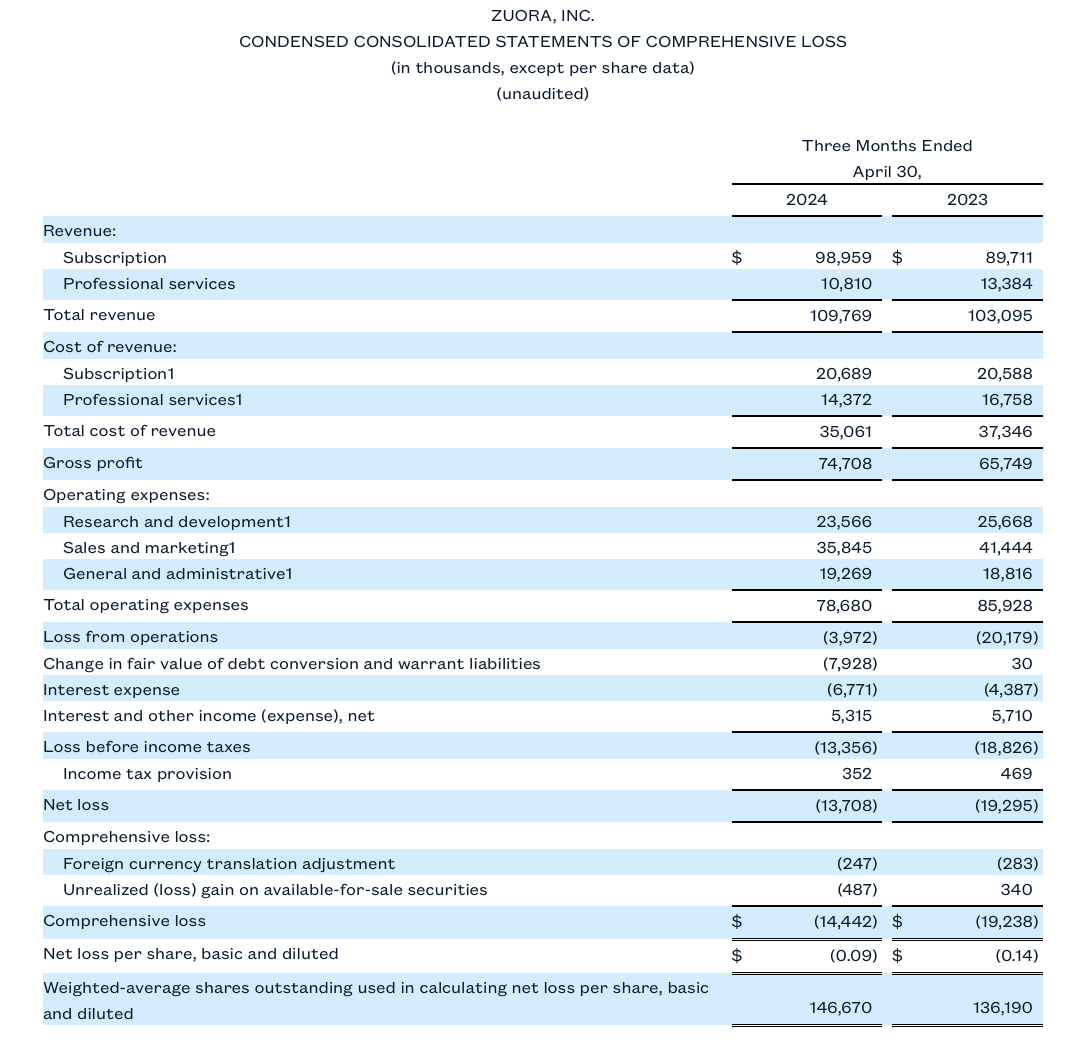

Let’s now go through Zuora’s latest quarterly results in greater detail. The Q1 earnings summary is shown below:

Zuora Q1 results (Zuora Q1 earnings release)

Zuora’s revenue grew 6% y/y on a total basis to $109.8 million in the quarter, ahead of Wall Street’s $108.8 million (+5% y/y) expectations. Subscription revenue saw stronger 10% y/y growth, decelerating only one point from Q4’s 11% y/y growth pace.

One of the core drivers of outperformance is better install-base expansion. Net revenue retention rates hit 104%, though this was lower than 108% in the year-ago Q1. Per CEO Tien Tzuo’s remarks on customer expansion on the Q1 earnings call:

One highlight of Q1, I would say, is our install-base expansion. Our stable of large enterprise customers continues to anchor the durability of our business. Our customer satisfaction levels continue to rise as measured by Net Promoter Score. Customers continue to love our new innovations, and this is driving strong expansion opportunities. In fact, in Q1, we saw a year-over-year increase in cross-sells, with customers either adding another Zuora product or adopting our technology in new business units. Some examples. Our customers are adopting additional products like Zephr […]

Our Zuora Revenue to Zuora Billing cross-sells are working. Last quarter we talked about Toast, as a great example, well this quarter we saw another Zuora revenue customer, a global leader in customer experience and contact-center solutions with over $1.2 billion in annual revenue. They added Zuora Billing with advanced consumption to help them analyze millions of customer usage data point to monetize their AI-powered support offerings.

We are supporting our customers to expand into new countries or regions.”

And yet from a sales execution standpoint, the company has also prioritized landing smaller, faster wins. These proofs-of-concept can be a great way for Zuora to get in the door, while expanding usage and cross-selling over time.

ARR growth, meanwhile, stood at 8% y/y in the quarter, which the company noted continued to be held back by macro-driven customer churn and lengthening sales cycles – both of which were already factored into the company’s guidance for both Q1 and the year.

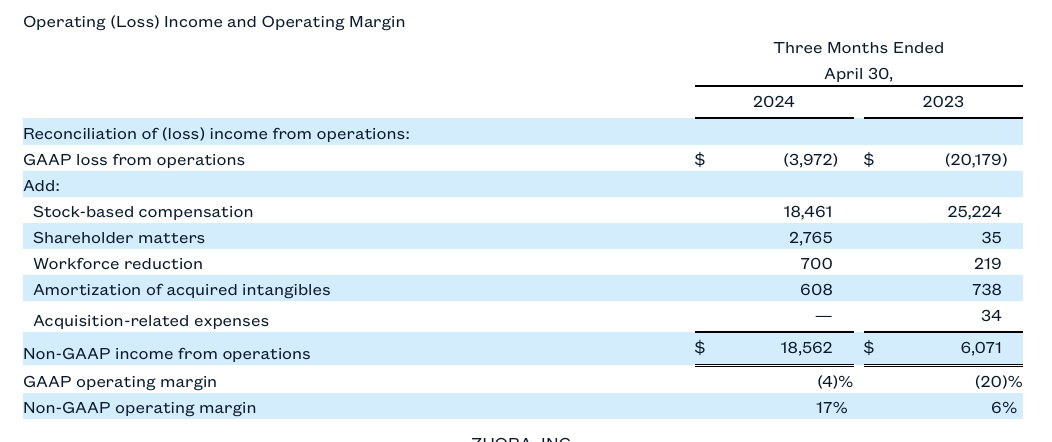

And from a profitability standpoint, note as well that Zuora’s pro forma operating margins leaped 11 points y/y to 17%:

Zuora operating margins (Zuora Q1 earnings release)

Pro forma EPS of $0.11 also quashed Wall Street’s expectations of $0.07.

Valuation and key takeaways

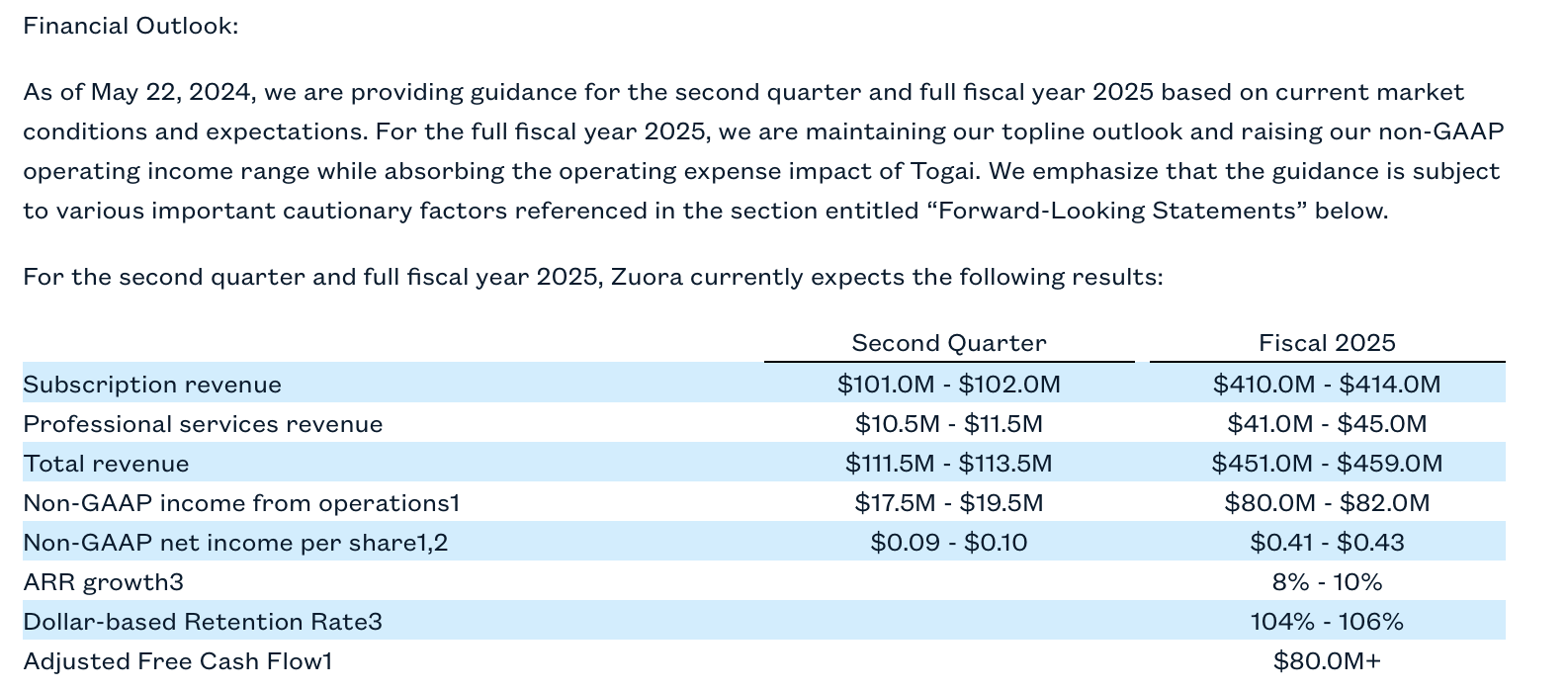

Note that, at least in my view, there’s a good deal of conservatism that sits in Zuora’s current-year outlook. The company updated its FY25 outlook to include absorbing Togai’s operating expenses (and yet pro forma operating income expectations came up by $1 million at the midpoint, driven by better trends in Q1), while it also held its full-year revenue outlook. Togai is to be sold as a standalone offering as well as bundled within Zuora’s existing suite for existing customers, so while we don’t have any financial details behind the transaction, it should be accretive to growth.

Zuora outlook (Zuora Q1 earnings release)

At current share prices near $10, Zuora trades at a $1.54 billion market cap; and after we net off the $547.1 million of cash and $362.3 million of debt on the company’s latest balance sheet, its resulting enterprise value is $1.36 billion. This puts Zuora at a 3.0x EV/FY24 revenue multiple, and a 17x multiple of FCF.

Given the rally that has already occurred over the past few months, I do think Zuora has already realized some of its value-based upside, and so my rating is slightly watered down (from a strong buy to simply now a buy). I’m confident holding Zuora up to a 4x EV/FY24 revenue multiple, implying a price target of $13 and ~25% further upside from current levels.