ra2studio

The UK primarily based non-public fairness firm 3i Group (OTCPK:TGOPF) has had an excellent previous yr with an 83% rise in share worth. However its upward climb is hardly only a characteristic of the previous yr. Over the previous 5 years, it is up 3x. And that’s not all. It pays a dividend too. Prior to now yr alone, the entire returns at 88% are 5 proportion factors greater than the worth returns.

The plain query now’s whether or not its worth rise can proceed, particularly preserving in thoughts its heavy publicity to the buyer sector, which is mentioned extra intimately right here.

Shopper sector targeted investments

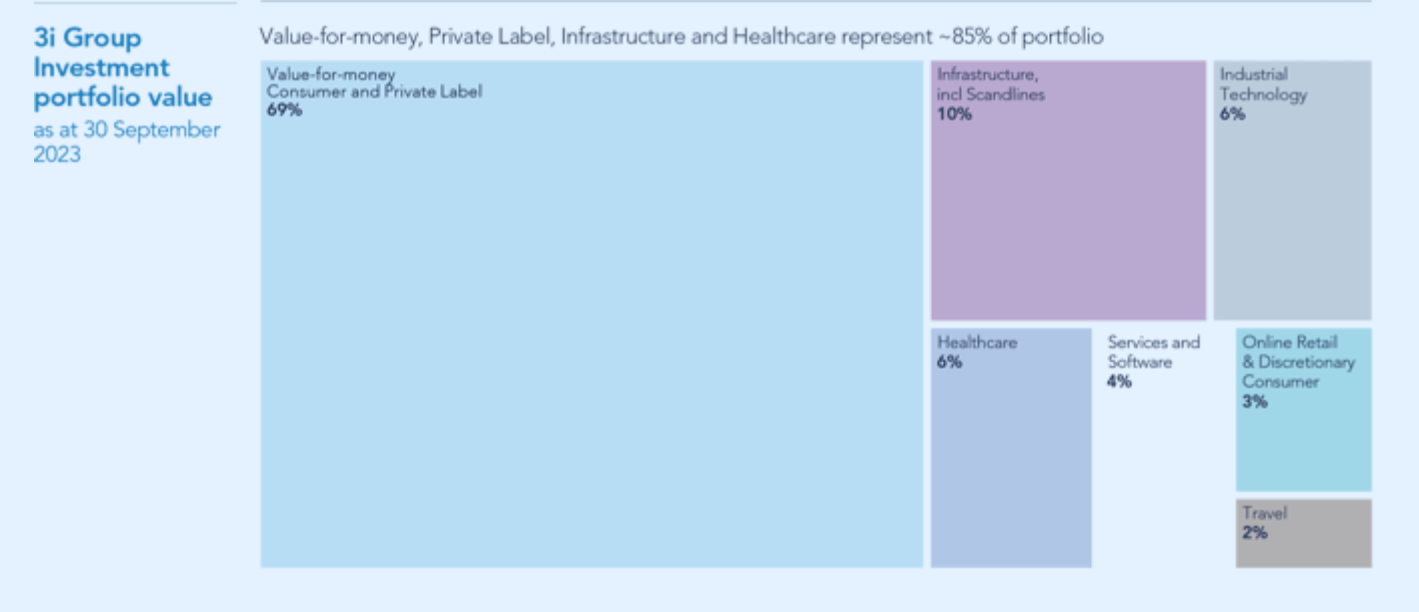

In precept, the fund invests in corporations throughout sectors. Nonetheless, it is arduous to disregard that 69% of its investments as of September 30, 2023 have been within the shopper sector. A lot of this funding in flip is in Motion, the Dutch non-food low cost retailer, which had a 63.5% share throughout the identical time. It additionally has an considerable curiosity in infrastructure investments (see chart under).

Supply: 3i Group

Monetary efficiency stays resilient

By way of efficiency, 3i is mainly in fine condition. In its temporary business update launched final week, the corporate updates on Motion’s strong monetary well being and likewise provides that “The rest of the 3i portfolio continues to demonstrate overall resilience with the majority of companies showing good momentum into 2024.”.

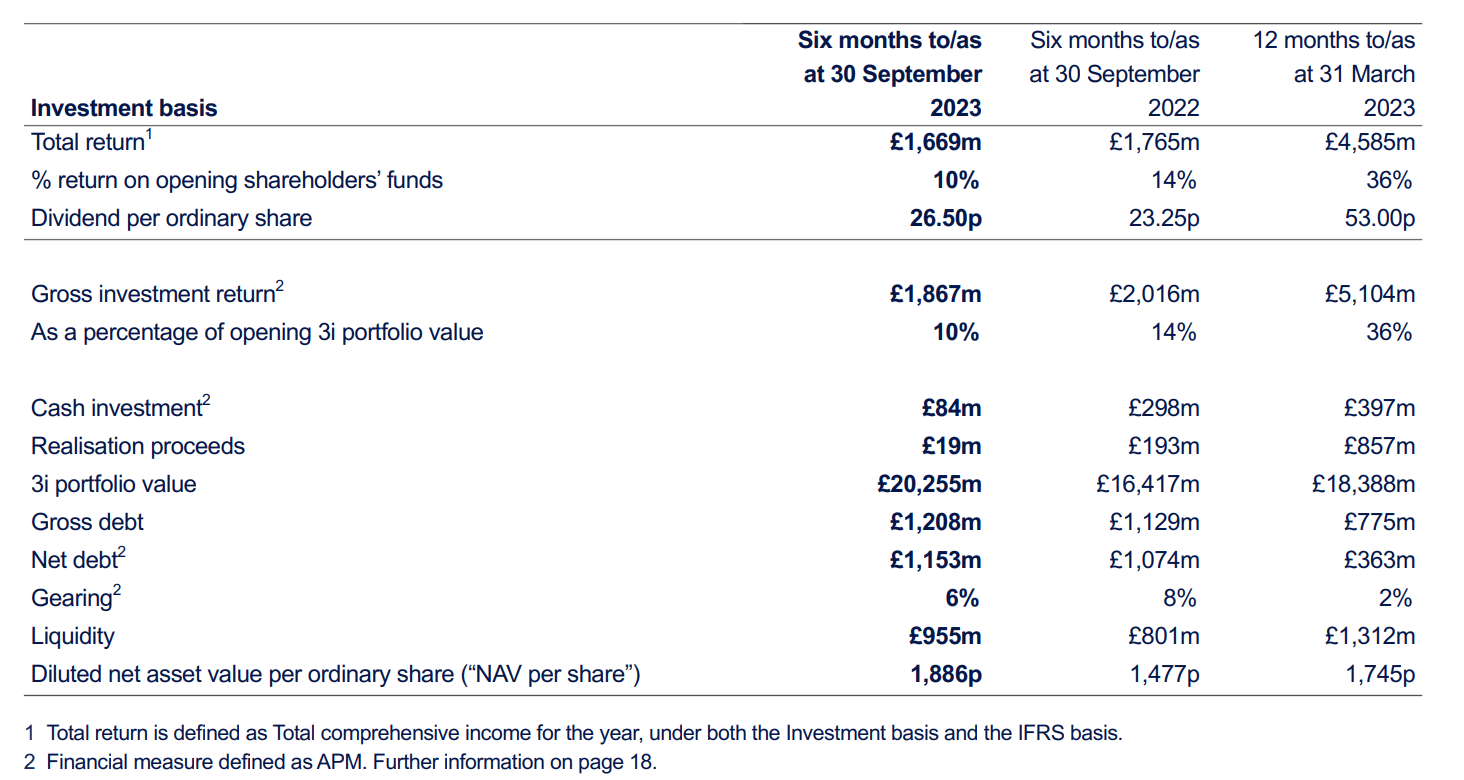

This, then is an extension of the last result update obtainable for the half-year ending September 30, 2023 (H1 FY24). The full return or internet revenue as a proportion of shareholders’ funds continued to stay in double digits, at 10%, regardless that they slowed down a bit from final yr (see desk under). At first look, the 5.4% YoY decline in internet revenue seems regarding however seems that it’s on account of international trade translation and never for any basic causes.

The portfolio worth has additionally seen a wholesome improve of 23.4% year-on-year (YoY). The gearing ratio, which is the corporate’s internet debt-to-assets ratio has additionally improved to six% from an already wholesome 8% in H1 FY23.

Key Financials, H1 FY24 (Supply: 3i Group)

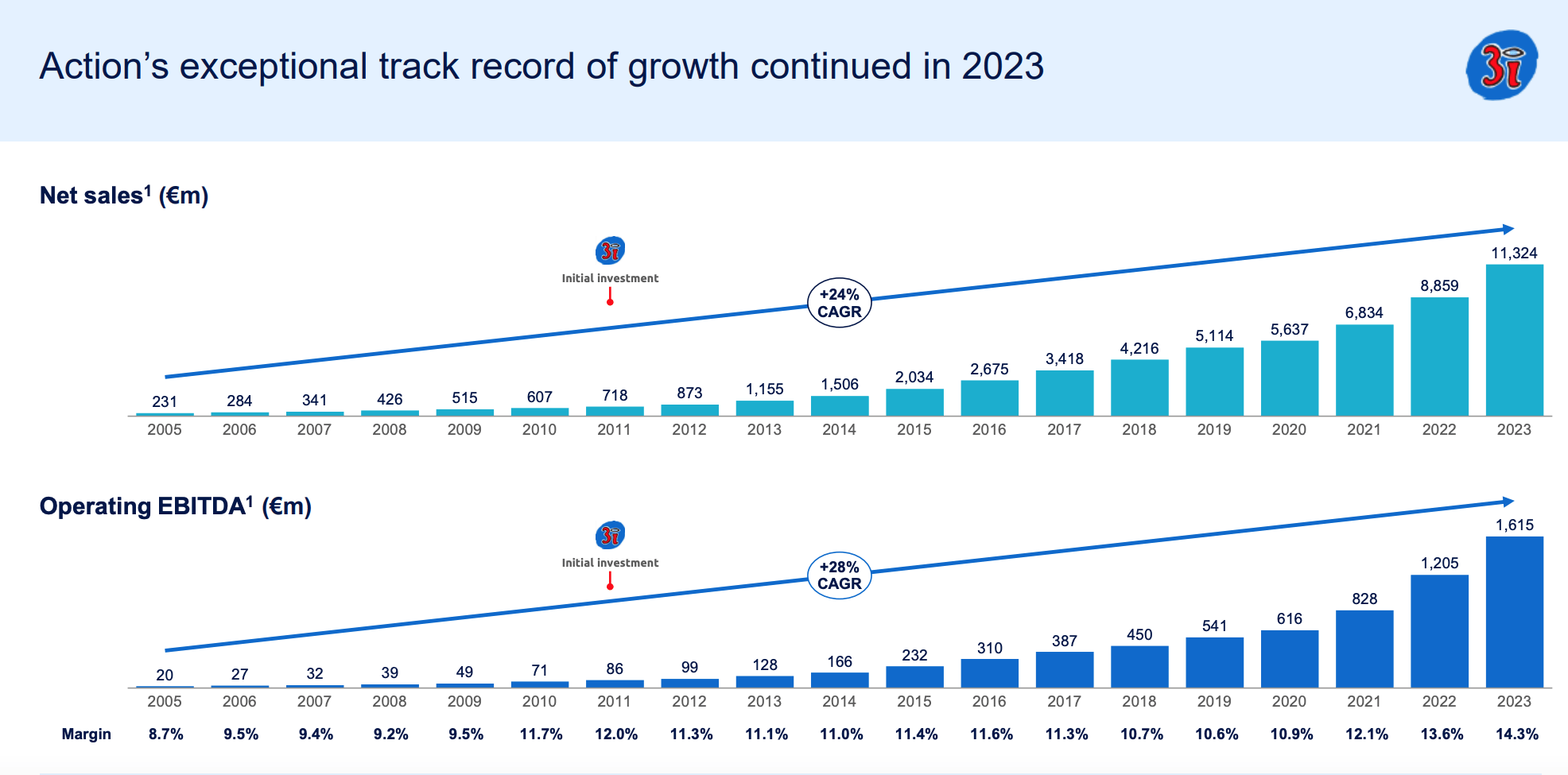

Motion’s spectacular development

To get a great understanding of what’s subsequent for 3i, it’s important to take a more in-depth have a look at Motion’s efficiency, on which it’s critically dependent. The retailer too, provides no causes to fret. Between 2005 and 2023, it has seen its internet gross sales compounded annual development fee [CAGR] at 24%. Additional, up to now 5 years, its common internet gross sales development of twenty-two% far exceeds the 12% common for its friends. 2024 has additionally began on a powerful observe, with like-for-like gross sales development of 21% YoY for the primary 11 weeks of the yr.

The corporate’s working EBITDA has additionally been rising since 2005 at a CAGR of 28% as much as 2023. With sooner working EBITDA development in comparison with internet gross sales, the margin expanded to 14.3% from 8.7% in 2005. It has additionally improved from the ten.7% even 5 years in the past (see chart under). Motion additionally anticipates touching a 15% margin by 2026.

Supply: 3i Group

Contemplate the dividend yield on value

With a strong efficiency in H1 FY24, the corporate additionally elevated its dividends by 14% YoY. Whereas the prospects look good for the complete yr too, even when it will increase them on the similar fee for the complete yr FY24, the dividend yield would nonetheless be considerably underwhelming at 1.9%, nonetheless. That is barely decrease than the TTM yield of two%. However as identified firstly, the delicate dividend yield obfuscates the affect of passive features from the inventory over time.

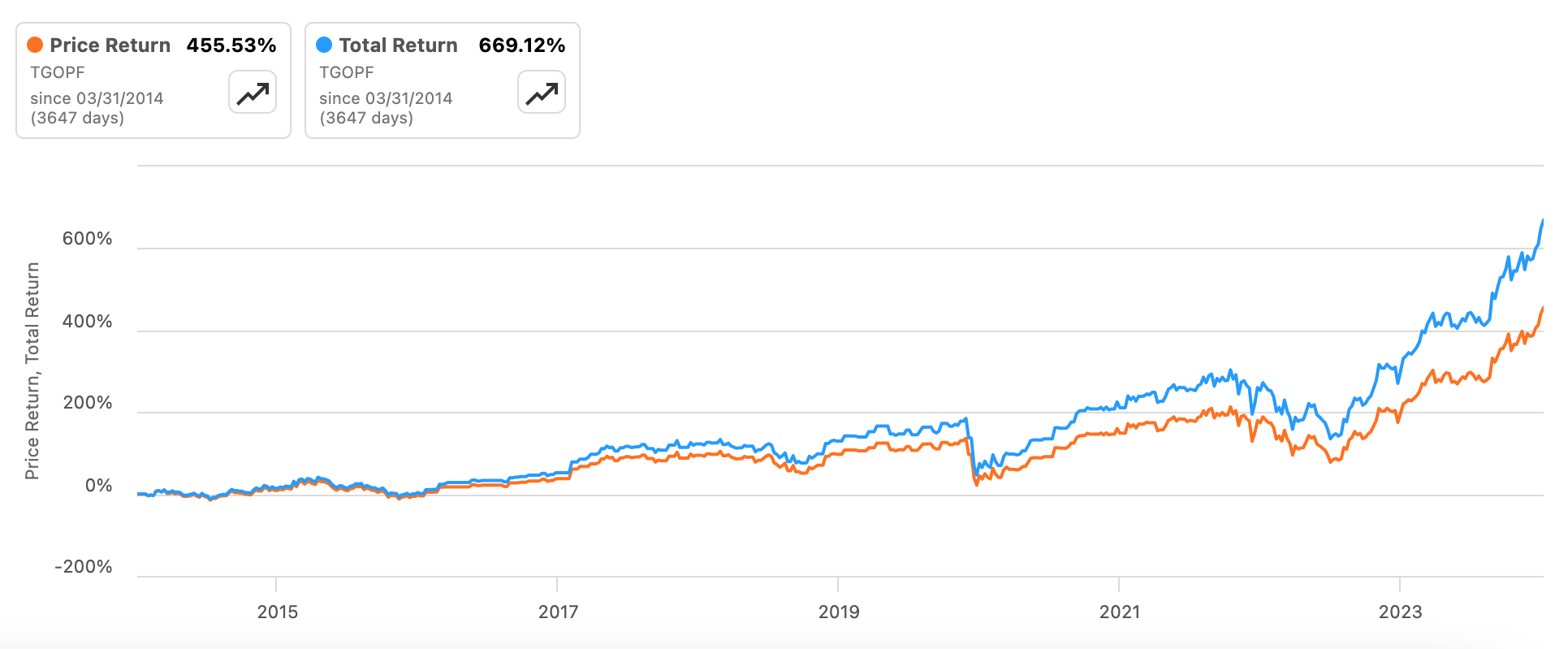

Contemplate this. The yield on value for an funding made in 3i 5 years in the past is 5.25% and 10.4% on an funding made 10 years in the past. Furthermore, over the previous decade, the entire returns on the inventory have been 214 proportion factors greater than simply the worth returns, that are fairly good in their very own proper (see chart under).

Worth and Complete Returns, 10y (Supply: In search of Alpha)

The market multiples

Additional, the inventory’s market multiples look good too. Assuming that the international trade developments stay unfavourable for the complete yr FY24, like in H1 FY24, the online revenue will drop. Nonetheless, the ahead GAAP price-to-earnings (P/E) ratio nonetheless is available in at a low 6.2x, which compares properly with its friends.

For instance, Blackstone (BX), the largest publicly listed non-public fairness fund by market capitalisation, has a corresponding ratio of 25.6x. However even smaller funds by market capitalisation than 3i, like TPG (TPG), have a a lot greater ahead P/E at 22.1x. This means that there continues to be a big upside forward for 3i.

On the similar time, the NAV per share can be price contemplating. If the quantity continues to develop by 27.7% YoY for the complete yr FY24, the identical as in H1 FY24, the determine could be at GBP 22.3. Nonetheless, the 3i inventory is buying and selling at a 26% premium to this degree in its house itemizing on the London Inventory Alternate. This may sometimes submit a threat to its worth now, however the inventory hasn’t been deterred by it within the latest previous. The truth is, it has persistently traded at a cushty premium to NAV over the previous yr.

Heavy Motion funding poses a macro threat

What does pose a possible threat is its funding in Motion. It has labored out very properly for 3i up to now however the huge publicity to it renders the fund susceptible too. The chance comes from the challenged macroeconomic well being of Europe. Though it has pursuits throughout huge European nations like France and Germany, apart from the Netherlands, which might steadiness out its efficiency, it is arduous to disregard the eurozone’s weak development as such. GDP barely grew within the closing quarter of 2024, by just 0.1% YoY.

Some enchancment is predicted in 2024 to 0.8% as per the European Fee, however even that is pretty low development. It’s not till 2025 that development is predicted to enhance to 1%+ charges. Some extra respite is feasible as inflation comes off drastically to 2.7% this yr from 5.4% final yr. However the important thing level right here is that the economic system isn’t out of the woods but. As a shopper firm, Motion is vulnerable to being impacted. And by extension so is 3i.

What subsequent?

Nonetheless, it does need to be acknowledged that the danger to Motion in 2024 is already decreased from final yr. Which means there’s a great likelihood that it may proceed to carry out this yr, as already evidenced in its gross sales for the primary 11 weeks of the yr. This bodes favourably for 3i, which too, has seen a good whole return for H1 FY24, even because it has seen a internet revenue contraction from final yr on account of unfavourable trade fee dynamics.

Even when the online revenue for the complete yr continues to say no on the similar fee as that seen in H1FY24, the inventory’s ahead GAAP P/E ratio nonetheless appears to be like good, although, compared to friends. Furthermore, its dividends add up considerably over time regardless that its sustained worth rise has stored the dividend yield low. It is also of consolation that the inventory sometimes trades at a premium to its NAV per share, as it’s doing now.

On steadiness, I imagine the positives for 3i outweigh the dangers. I’m going with a Purchase score on it.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please pay attention to the dangers related to these shares.