alephx01

Thesis

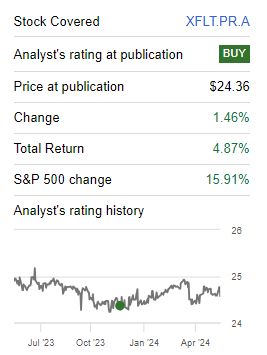

We wrote about the 6.50% Series 2026 Term Preferred Shares (XFLT.PR.A) half a year ago, when we started covering the securities with a ‘Buy’ rating. In our original article, we highlighted the strong coverage for the securities and the appealing yields. The security is up since our rating:

Prior Rating (Seeking Alpha)

With the preferred shares now close to par and tight overall spreads in the credit markets, we are going to highlight why the risk/reward profile for XFLT.PR.A has changed, and why we are downgrading the security to Hold.

Preferred shares – a yield play

CEF preferred shares are issued in order to obtain leverage. Usually, they have a $25/share par value (which is the case here), and upon termination return said par value to holders. Unlike regular equity, preferred shares do not have any upside because they do not represent an ownership in the business. They are a form of debt. And just like debt, they represent a yield play.

As a rule of thumb, when buying preferred equity one needs to be very careful when it trades around par or above, since there is no upside to be had in a normalized economic environment.

Traditional preferred shares do not have a defined maturity date, and can be perpetual. In the case of XFLT.PR.A, they are term preferred shares with a defined maturity date in March 2026:

Maturity Date (Prospectus)

This translates to holders getting $25/share once the shares mature in 2026. Until then, a holder can only clip the coupon, and if buying under par, they can realize a capital gain upon the maturity of said term preferred shares. That capital gain is embedded in ‘yield to maturity’ calculations, but disappears when the shares trade at par.

CLOs have been on a tear lately

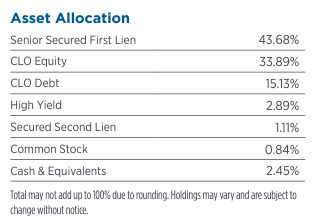

The CEF contains a portfolio of CLOs, leveraged loans and bonds:

Collateral (Fact Sheet)

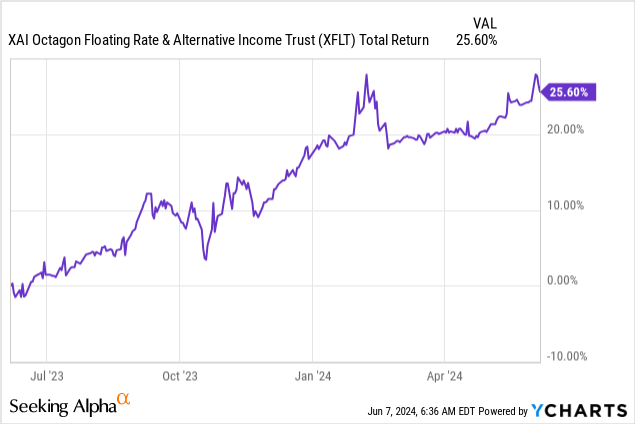

As the underlying holdings have performed, the CEF common shares trading under the ticker XFLT have seen a robust total return:

The common shares are up more than 25% on a total return basis in the past year, a performance which has helped the credit spreads of the preferred shares. There is a high correlation between required preferred shares spreads on underperforming CEFs versus performing ones. The more robust the common shares, the better, the lower the required credit spread for preferred shares.

In today’s high rate environment, CLOs have performed admirably. A floating rate asset class generally for IG CLO bonds, CLOs have been able to act as a pass-through vehicle for higher yields.

Current yield is too low to buy

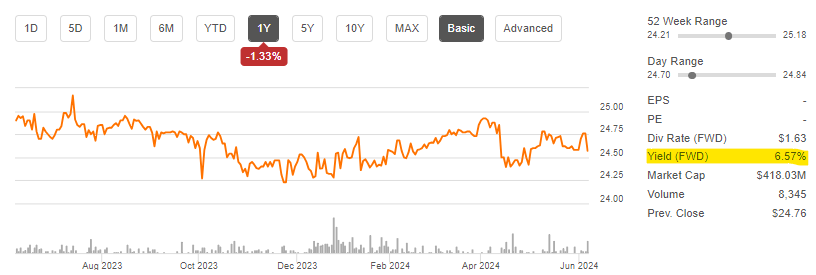

With the rally in price, the preferred share’s current yield is now too low to buy:

SA Landing Page (Seeking Alpha)

At only 6.6%, the current yield is barely above what AAA CLO ETFs offer. We have recently covered an Invesco AAA CLO ETF in the ‘ICLO: Invesco’s AAA CLO Fund, 6.7% Yield‘ article. This makes the XFLT preferred shares a hold here rather than a buy. An investor needs to pick-up spread when buying more illiquid assets, such as XFLT.PR.A, and that spread is just not there currently.

As we can see from the Seeking Alpha landing page, the securities had a volume of only 8,345 shares, thus highlighting the retail nature of the placement, and the low liquidity offered here. Look for current yields in excess of 7% in order to re-enter the name via a buy. Until then, the shares represent just a hold. If they end up trading above par, we would look to even sell at those levels.

The preferred shares are becoming a cash parking vehicle

As we near the maturity date in March 2026, the preferred shares will become more of a cash parking vehicle, with pricing around par and a very low duration. As discussed in the original coverage article, the preferred shares have a mandatory term maturity date, and have the common shares fully subordinated.

However, because of low liquidity, a significant risk-off event could see a gap down in pricing on a high volume sell day. That sort of scenario would constitute a buying opportunity.

Holding for the yield

As we have seen from the above analysis, the term preferred shares have an ever decreasing duration, and although the current yield is not competitive from a new money perspective, it represents a compelling story for investors who are already in the name. When holding CEF preferred equity, one should look for stability and predictability. XFLT.PR.A offers both.

The only outside risk factor for this name is represented by a significant bout of risk aversion, an event which would drain liquidity and potentially see a down day on high volumes. Securities like XFLT.PR.A are not set-up for high volume days, and in the case of a number of large holders heading for the exists, prepare for unusual gap-downs in price. Those gap-downs would be temporary in nature, since the term maturity date is fairly close.

Conclusion

XFLT.PR.A are the term preferred shares from the XFLT CEF. The fund uses the preferred shares to leverage its structure, and pays out a 6.5% coupon to holders. With the shares trading near par now, the current yield has been greatly reduced, making an entry into the name at the current levels unappealing. The term preferred shares have a low duration and ample coverage, thus represent an appealing instrument to hold. As they continue to near their maturity date, expect lower volatility, although there might be liquidity-driven gap-down days.