primeimages/E+ via Getty Images

Beware of noise, hurry and crowds

In his book Celebration of Discipline, American theologian Richard Foster warned that noise, hurry and crowds were the most significant obstacles to a vibrant spiritual life. The same could be said of successful value investing. When it comes to investing, ignoring the noise, exhibiting patience and being indifferent to the prevailing sentiment of the crowds sounds like the right thing to do. Most people would not argue with these principles, yet behavior suggests otherwise.

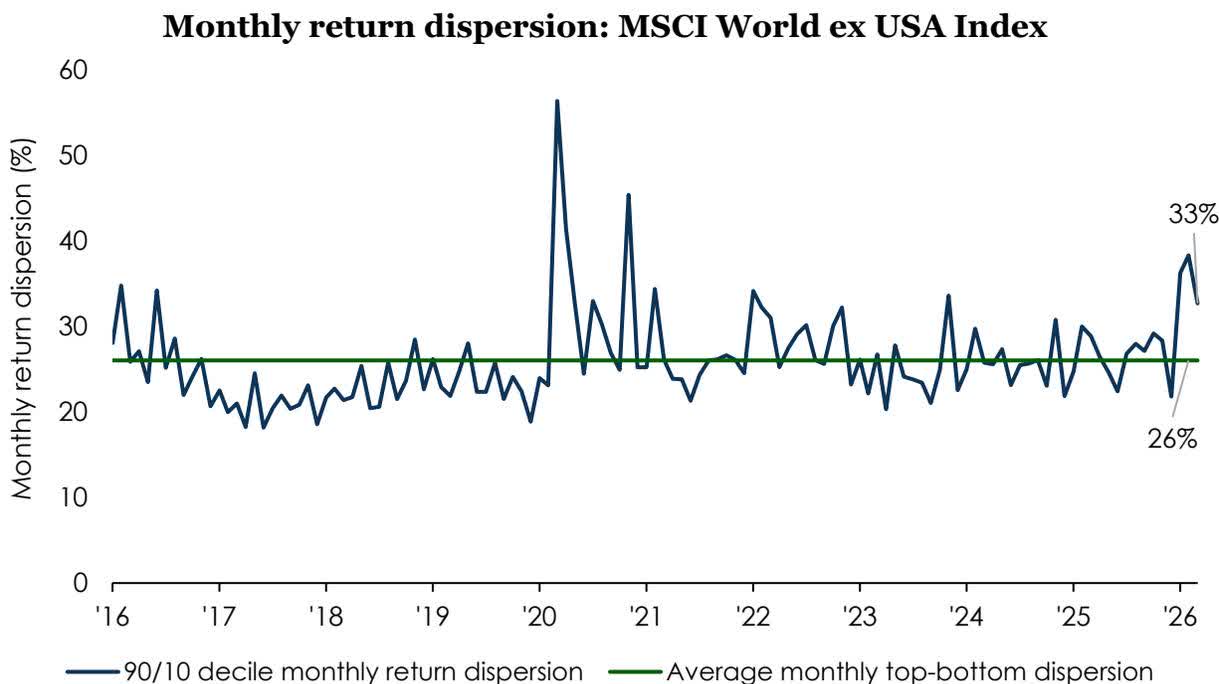

If there ever were a quarter of noise, this may have been it. The first 90 days of 2026 experienced near-record stock dispersion—that is, an unusually wide spread between the best- and worst-performing stocks—based on whatever company or industry the market happened to view that day as an AI winner or loser. For instance, the difference between the highest- and lowest-return stocks in the MSCI World ex-USA Index has been well above average, with a gap in performance of over 80 percentage points in the quarter, as investors debated the impact of AI. Then, in the last month of the quarter, bombs started falling in Iran and oil ran up well past $100 per barrel. As I write today, trying to make a deadline for publication with something timely and relevant, the White House announced progress toward a de-escalation. Noise galore.

Source: FactSet. Monthly data from 12/31/2015 through 3/31/2026. Returns represent the average performance of top and bottom decile stocks within the MSCI World ex USA Index; spreads are calculated as top decile minus bottom decile. Charts are for informational purposes only and do not depict the performance of any Harris | Oakmark strategy or product.

We aren’t technology neophytes; we believe AI is for real and is changing the way many of us work, and there will be winners and losers. However, we do believe the market has been too eager to declare victory and defeat. Where there is a real threat of change, we lower our estimate of value by reflecting a higher risk of disruption. In the case of large, deeply embedded enterprise software companies such as SAP, we think the market has skewed too negative on the risks introduced by AI, when in fact, there is a real possibility that AI is additive. We do not pretend to know how the Iran conflict is going to end, but there have been scores of these conflicts over my nearly 27 years at Harris | Oakmark and the world keeps turning. Remember, WTI (West Texas Intermediate) oil futures have both been in the triple digits and negative over the past six years. Meanwhile, population and incomes grow and the global economic pie along with them. We see the same bewildering headlines you do, but remain focused on the clarity of business values, which are far more stable than daily headlines.

The only way to really hurry your way to success in the equity markets is to have insight into the next tick and the ability to act before it moves. This requires an advantage in physics, not insight. At Harris | Oakmark, we estimate the intrinsic value of a business. There is an identifiable reason (or reasons) why the market price and our estimate differ. Often it boils down to our time horizon being longer than the marginal market participant. It takes time for value to be realized. Fixed income investors seem to understand this better than equity investors. In the bond world, one typically starts the conversation with duration—in other words, the desired time horizon for the securities you are looking to own. Equities are perpetual in duration, which means their theoretical time horizon is longer than that of even the longest bonds. Yet much of the market coverage focuses on one-minute charts, and the financial press seems to like or dislike a company based on how well it performed over the last quarter relative to broader expectations, with almost no airtime given to the long-term outlook for the business. Today, an estimated 60% of index options tied to the S&P 500 have same-day expirations and there are even new 5- and 10-minute option contracts being marketed for indices and cryptocurrencies. This short-termism reflects investors losing touch with the actual duration of the assets they own. Just because you can trade a stock one minute at a time (or less) doesn’t mean you should. At Harris | Oakmark, we think of equities as proportionate interests in real businesses that have real value based on the total future cash flows of the business. We have more insight into what the business ought to look like over time than where the stock will go over the next day, quarter or year. Don’t get me wrong, we would love the value gap to close the second we buy a stock, but unfortunately that is not how markets function.

Following the crowd is the easier—but more dangerous—path. I’m sure I’m not the only one who pleaded with my parents that, “everyone else was doing it” to which they replied, “if everyone else jumped off a cliff would you?” In markets, it is generally cause for concern when everyone seems to believe the same thing. Market participants make markets and markets price assets. Crowding occurs when there is more than typical agreement between market participants. That “agreement” gets priced into the asset such that there is little room for different outcomes without the stock getting pummeled. Beyond that, crowding introduces endogenous (or self-inflicted) risks that go beyond fundamentals, such as distorting liquidity dynamics on a security such that the distribution of future price outcomes skews negatively. By nature, as value investors we seek mispriced stocks—specifically, stocks selling well below their intrinsic value. Often this means going against the “crowd”. In our view, if everyone seems to believe something, you should assume a good portion of that belief is priced into the security. Meaning, if you and the crowds are right, there is little to no excess return and if wrong, painfully below average returns are likely. When a stock is undervalued, investors can afford to be wrong given the stock is unlikely priced to perfection. This is the essence of the “margin of safety” concept and the reason we require a significant discount before investing in any company.

We cannot promise much as regulated investment advisors but know that we are truly committed to a disciplined process that ignores the noise, exhibits patience, and is indifferent to the crowd.

Thank you for your partnership with us in our international equity portfolios.

We are eager to hear from you, so please do not be shy.

Tony Coniaris, CFA, Portfolio Manager

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.