DNY59

We beforehand coated Anheuser-Busch InBev SA/NV (BUD) in November 2023, discussing its (nonetheless) impacted gross sales quantity within the North American area, with losses intensifying because the administration had to offer monetary help to its wholesalers.

Then once more, we had maintained our Purchase score, with the administration’s profitable advertising efforts in different areas contributing to its glorious FY2023 steering and the promising consensus ahead estimates by way of FY2025.

On this article, we will talk about why we stay optimistic about its long-term prospects, with BUD reporting bottoming headwinds within the North American gross sales and stabling market share by FQ4’23.

On the identical time, the administration continues to spend money on the excessive development spirits-based ready-to-drink/ zero beer segments as customers more and more demand more healthy and expanded beverage choices.

Because of the well-balanced prospects, we consider that BUD might ship a greater than first rate capital appreciation over the following few years.

The BUD Funding Thesis Stays Tempting Right here, With Nice Upside Potential Forward

For now, BUD has reported a comparatively first rate FQ4’23 earnings name, with revenues of $14.47B (+6.2% YoY natural), adj EBITDA of $4.87B (+6.2% natural), and adj EPS of $0.82 (-4.6% YoY).

FY2023 introduced forth equally first rate numbers of $59.38B (+7.8% natural), $19.97B (+7% natural), and $3.05 (inline YoY), respectively, with the decline in its personal beer volumes by -2.3% YoY well-balanced by the expansion within the non-beer volumes by +2.1% YoY.

On the one hand, it’s obvious that BUD has confronted a drastic decline within the North American gross sales by -$1.37B and adj EBITDA by -$1.26B on a YoY foundation in FY2023, attributed to the Dylan Mulvaney backlash.

With the area being its top-line driver in FY2022, we will perceive why the beverage firm has not been in a position to recuperate from the backlash as many customers opt for competitor brands.

If something, BUD has been painfully “unseated” with Modelo now being the top-selling US beer, as Modelo Especial commanded the successful spot with 8.7% in retail share in comparison with Bud Mild at 7.3% for the the week earlier than and after the Tremendous Bowl.

With Bud Mild’s gross sales quantity down by -30% on a YoY foundation throughout the Tremendous Bowl week, it’s unsurprising that the administration has commented that the corporate’s “full growth potential (in FY2023) has been constrained by the efficiency of its US enterprise.”

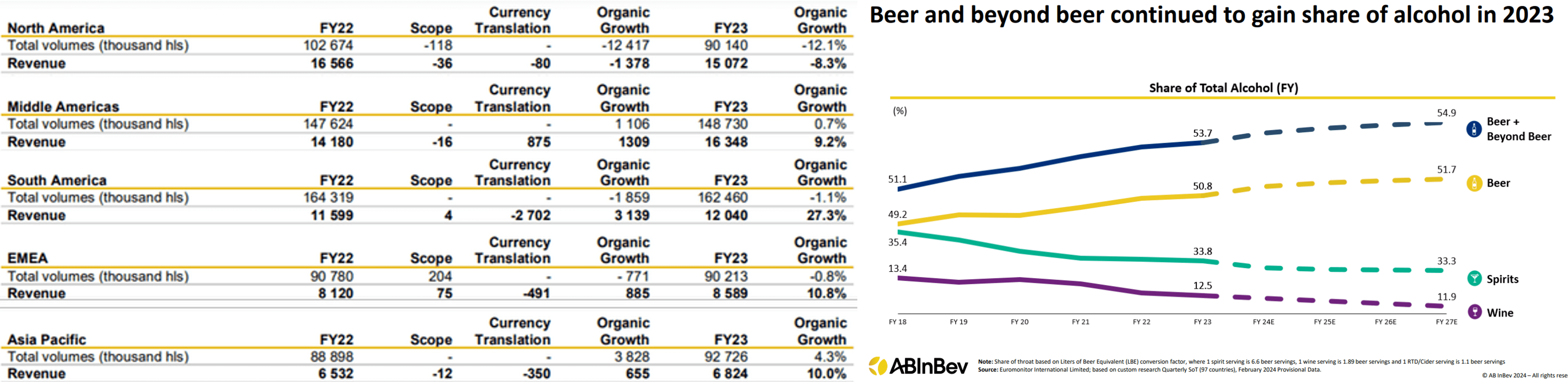

BUD’s International Operations

BUD

Alternatively, with BUD’s headwinds concentrated within the US, it’s also obvious that every one different areas reported greater than first rate development to this point, considerably balancing the state of affairs.

This additional exemplifies the beverage firm’s well-diversified international choices throughout Beer and Past Beer (together with ready-to-drink drinks), Spirits, and Wine, permitting the administration to drag a number of levers to drive quantity development, market share enlargement, and balanced monetary efficiency.

If something, BUD has continued to spend money on its highest development phase, Past Beer, as consumers increasingly demand healthier and expanded alcoholic beverage choices.

This transfer has confirmed to be comparatively profitable, with BUD’s non-alcoholic beer choices producing a market main US gross sales of $117.42M in 2023, properly exceeding Heineken (OTCQX:HEINY) at $77.45M and Athletic Brewing at $51.83M.

Globally, BUD’s quite a few zero-beer choices have additionally triggered a formidable “high-teens revenue growth in FY2023,” underscoring its potential to enchantment to the well being aware customers.

If any factor, the BUD administration has already scored the first-ever beer sponsorship cope with Corona Cero within the Olympics by way of 2028, additional underscoring their willpower to generate new development.

On the identical time, BUD’s spirits-based ready-to-drink portfolio delivered double-digit quantity development, properly outperforming the trade in FY2023.

With Euromonitor projecting that nonalcoholic spirits might develop at a CAGR of +30% over the following few years, in comparison with the +6% estimates for typical spirits, we consider that we may even see the corporate’s well-diversified alcohol portfolio generate new development whereas capturing significant market shares within the long-term.

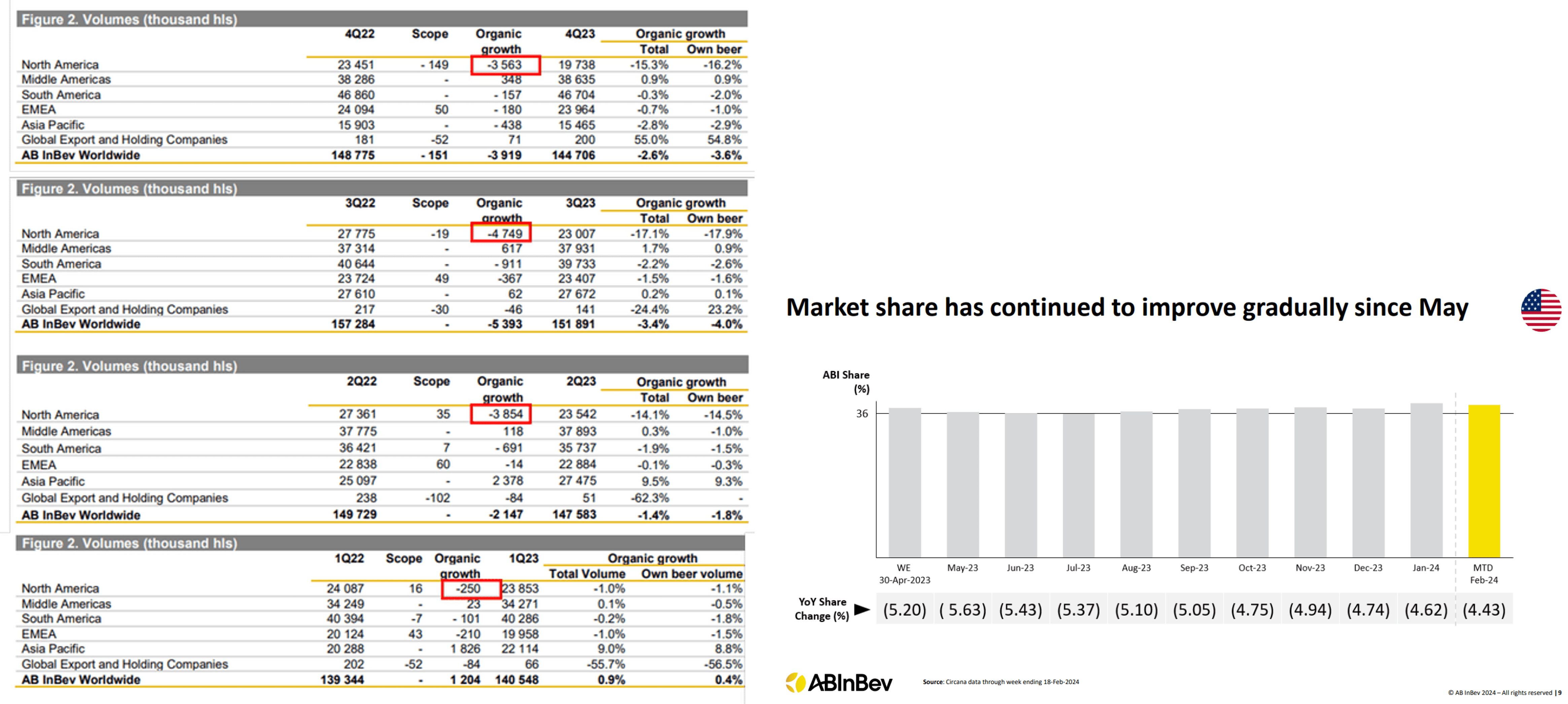

BUD’s Stabling Gross sales In North America

BUD

On the identical time, issues appear to be stabling on a QoQ foundation, because the decline in BUD’s North American bought volumes peaked by FQ3’23 at -4.74K hls and improved on a QoQ foundation by FQ4’23 to -3.56K hls.

The identical has been reported within the narrowing market losses of -4.43 factors as of February 2024, in comparison with the -5.63 losses reported in Might 2023 and -4.74 losses in December 2023.

Whereas the North American market is more likely to underperform within the near-term, we preserve our perception that the worst could also be behind us, because the administration continues to navigate the challenges and slowly regain its beer market share shifting ahead.

As BUD intensifies their advertising efforts and invests in a number of partnerships, it’s unsurprising that the North American adj EBITDA margin has suffered at 29.2% in FQ4’23 (-2.7 factors QoQ/ -6.3 YoY) and at 31.4% (-5.2 factors YoY) in FY2023.

Because of its intermediate-term headwinds, readers might need to word that related backside line headwinds might proceed till issues normalize.

For now, regardless of the US market headwinds, BUD continues to ship sturdy shareholder returns, with the constant share repurchases delivering secure share depend of roughly 2.01B, on prime of the spectacular dividend development of +9.3% YoY from €0.75 per share in 2022 to €0.82 per share in 2023.

On the identical time, the administration continues to deal with deleveraging its steadiness sheet with moderating long-term money owed of $72.03B (-6.3% YoY) and rising money/ equivalents of $10.33B (+3.6% YoY) in FY2023.

Because of this, it’s obvious that BUD has been placing a lot of its sturdy Free Money Circulate technology of $8.62B (+6% YoY) to good use, additional underscoring why the inventory stays a viable dividend funding thesis.

On the identical time, the administration has guided glorious adj EBITDA development of between +4% and +8% in FY2024, improved than its historic development at a CAGR of +2.5% between FY2016 and FY2023.

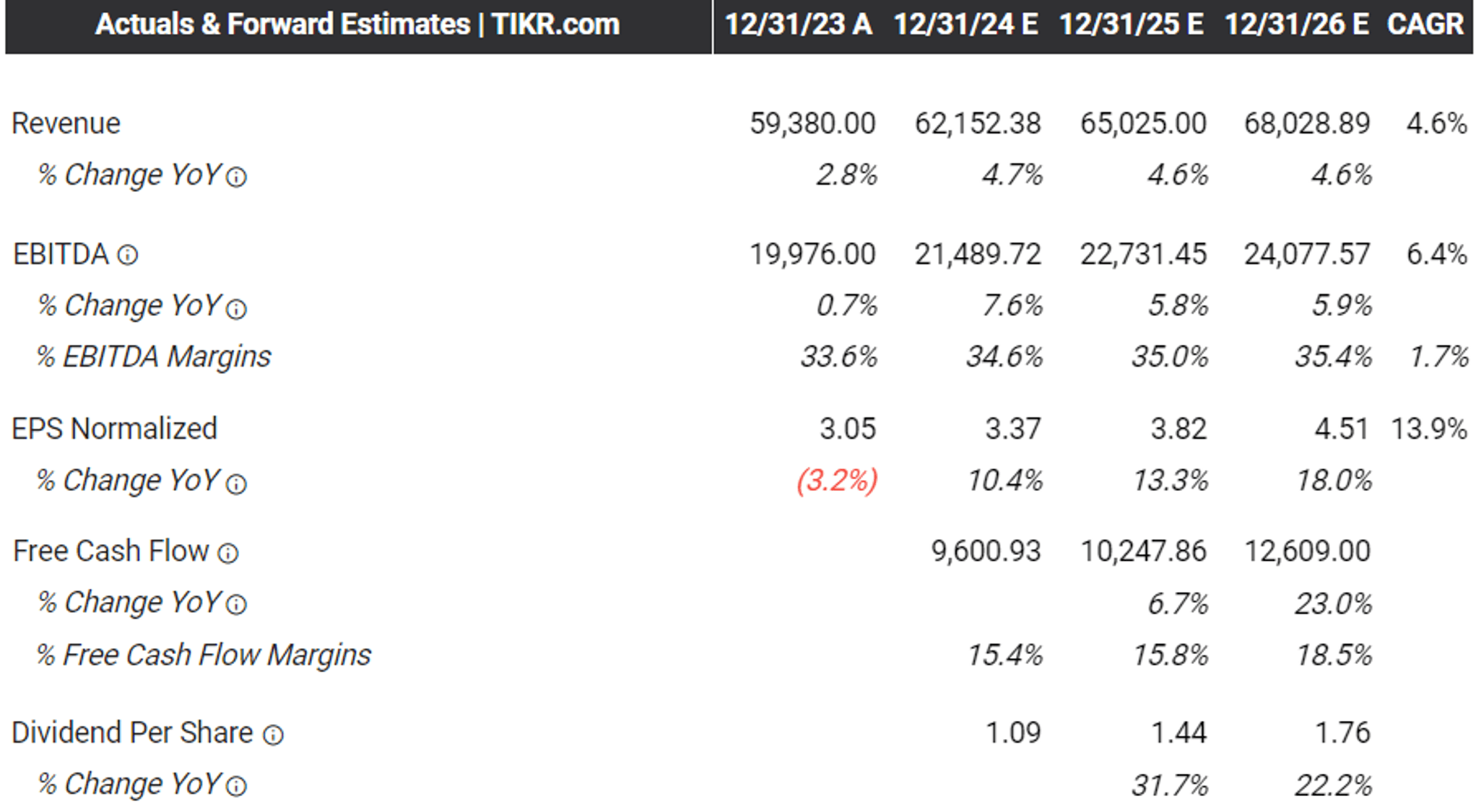

The Consensus Ahead Estimates

Tikr Terminal

Because of these promising developments, we will perceive why the consensus have reasonably raised their ahead estimates, with BUD anticipated to generate an accelerated prime/ backside line enlargement at a CAGR of +4.6% and +6.4% by way of FY2026.

That is in comparison with the earlier estimates of +4.5%/ +5.5%, additional implying that the market is assured concerning the firm’s potential to climate the temporal North American headwinds.

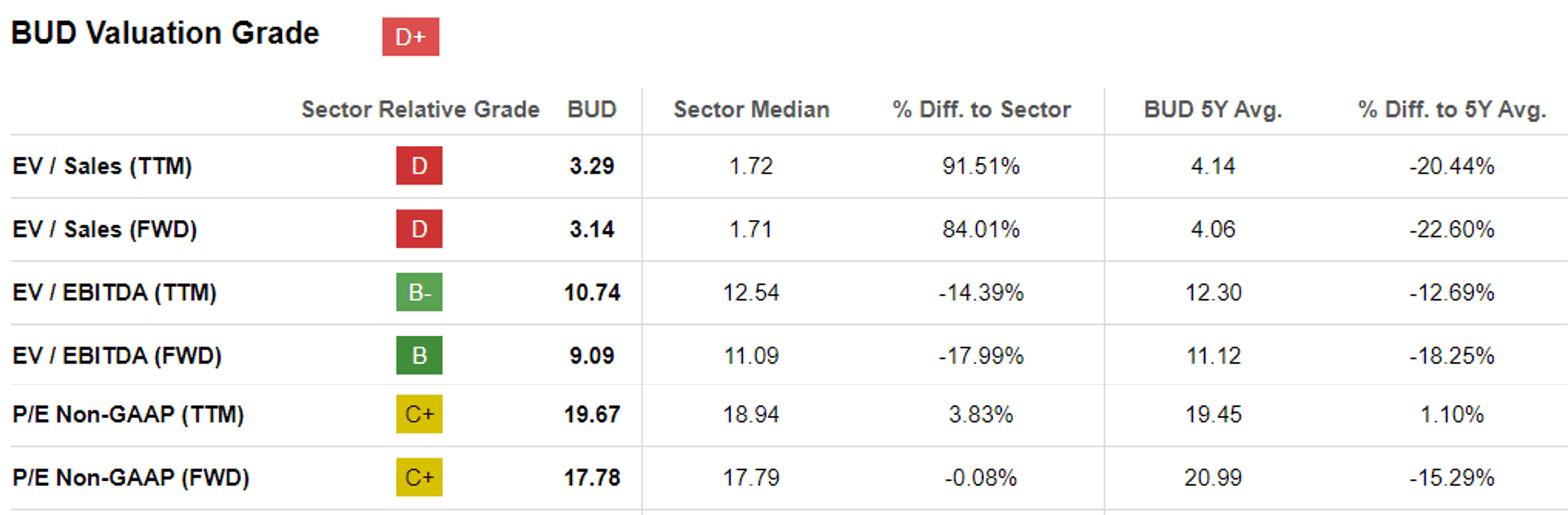

BUD Valuations

Looking for Alpha

Because of these developments, we preserve our perception that BUD stays attractively valued now at FWD EV/ EBITDA of 9.09x and FWD P/E of 17.78x, in comparison with the 3Y pre-pandemic imply of 13.25x/ 21.47x.

Whereas these numbers seems to be elevated in comparison with Molson Coors Beverage Firm (TAP) at FWD P/E of 11.83x, BUD’s valuations stay cheap when in comparison with its alcohol beverage friends, together with Carlsberg (OTCPK:CABGY) at FWD P/E of 16.58x, HEINY at 17.20x, and the sector median of 17.79x.

Because of this, we consider that BUD is just not costly right here, with the administration’s latest execution additional demonstrating why they’ve learnt their painful classes and are extraordinarily centered on reversing the US shopper sentiments whereas producing international development.

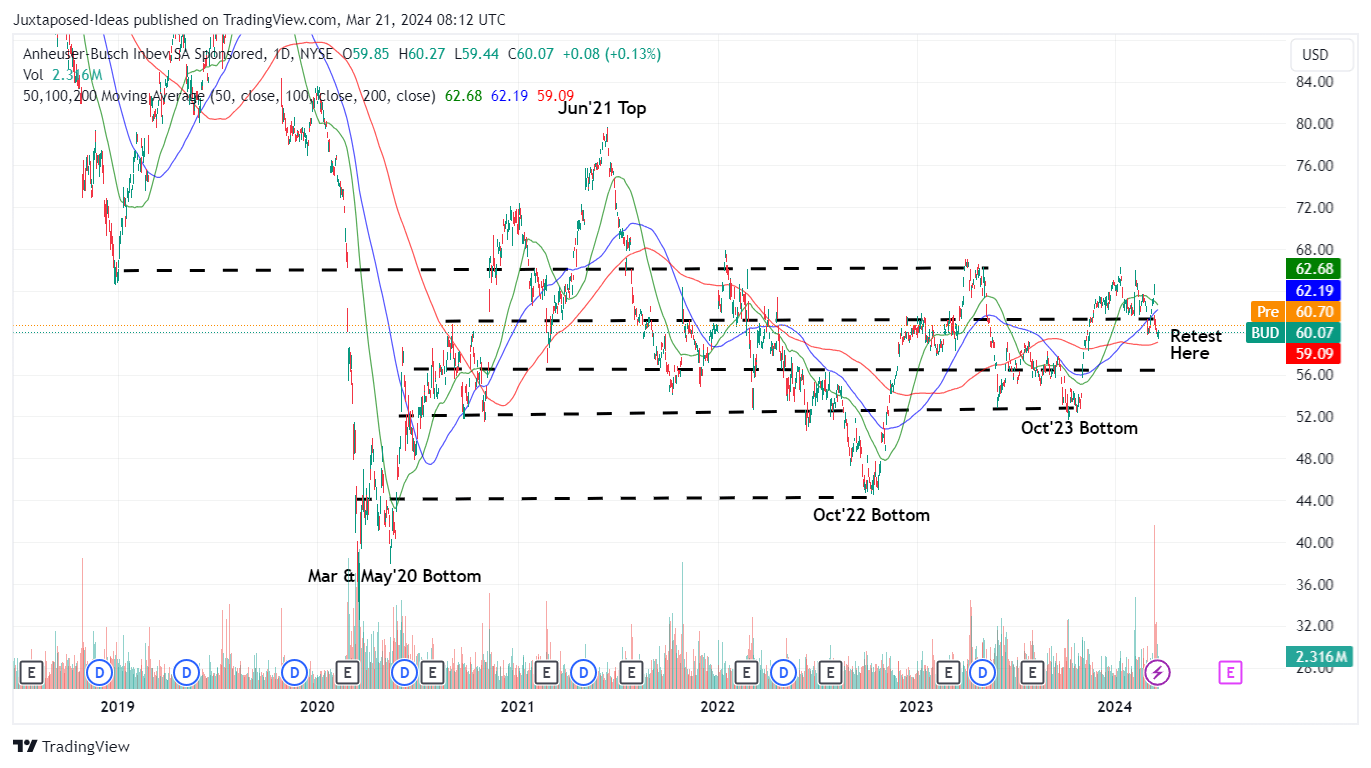

So, Is BUD Inventory A Purchase, Promote, or Maintain?

BUD 5Y Inventory Worth

Buying and selling View

For now, BUD has misplaced a part of its latest FQ4’23 beneficial properties, as it’s reported that Altria (MO) can be promoting a part of their BUD stake to fund share repurchases.

Nevertheless, we consider that the latest pullback triggers an expanded ahead dividend yield of 1.37%, comparatively inline with its 4Y common of 1.39%. Dividend hunters can also stay up for the 2023 dividends payable on June 07, 2024 for shareholders of report Might 06, 2024.

Based mostly on the FY2023 adj EPS of $3.05 and the FWD P/E valuations of 17.78x, we consider that BUD is buying and selling close to to our honest worth estimate of $54.20. Based mostly on the FY2026 adj EPS estimates of $4.51, there seems to be a wonderful upside potential of +33.8% to our long-term value goal of $80.10 as properly.

Because of its (potential) twin pronged returns by way of capital appreciation and dividend incomes, we’re sustaining our Purchase score for the BUD inventory right here.