redmal/iStock via Getty Images

The Nuveen Global High Income Fund (NYSE:JGH) is a closed-end fund that should appeal to those investors who are looking to earn a high level of income from the assets in their portfolio while adding some diversification to it. I have discussed why achieving some international diversification could be important right now in a few recent articles (see here and here). The fund currently boasts a 9.76% yield, so it does not disappoint in the income department. After all, this yield is substantially higher than the 1.34% yield of the S&P 500 Index (SP500) or the 3.41% trailing twelve-month yield of the Bloomberg U.S. Aggregate Bond Index (AGG). Unfortunately, the yield of the Nuveen Global High Income Fund is lower than that possessed by many of its peers:

|

Fund Name |

Morningstar Classification |

Current Yield |

|

Nuveen Global High Income Fund |

Fixed Income-Taxable-Global Income |

9.76% |

|

BrandywineGLOBAL – Global Income Opportunities Fund (BWG) |

Fixed Income-Taxable-Global Income |

11.44% |

|

DoubleLine Income Solutions Fund (DSL) |

Fixed Income-Taxable-Global Income |

10.61% |

|

PIMCO Dynamic Income Opportunities Fund (PDO) |

Fixed Income-Taxable-Global Income |

11.61% |

|

Western Asset Global Corporate Defined Opportunity Fund (GDO) |

Fixed Income-Taxable-Global Income |

11.99% |

|

abrdn Global Income Fund (FCO) |

Fixed Income-Taxable-Global Income |

14.48% |

This chart makes it quite clear that the current yield of the Nuveen Global High Income Fund is well below that of many of the fund’s peers. Investors in closed-end funds frequently make their purchase decisions based on a fund’s yield, and the value that the market assigns to a fund also tends to depend on the fund’s distribution. After all, a fund’s share price will frequently increase following a distribution hike even if nothing has fundamentally changed with its portfolio. As such, the lower yield could result in this fund being somewhat undesirable among some investors. However, we should still take a deeper look at it, as there is more to these funds than the distribution alone.

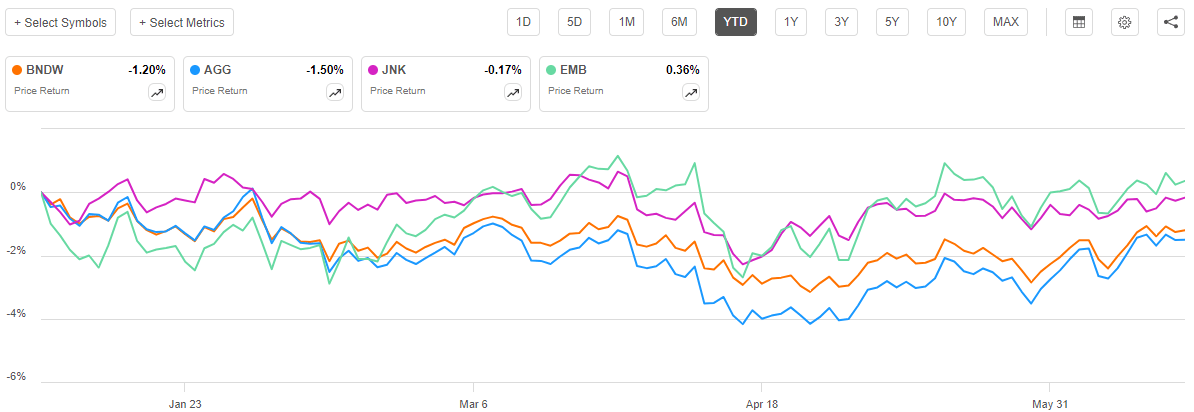

As regular readers might remember, we previously discussed the Nuveen Global High Income Fund in late January 2024. The domestic bond market has delivered a rather disappointing performance since that time, as investors began to realize that their predictions of a rapid decline in interest rates over the course of 2024 were entirely too optimistic, and they began repricing bonds and yields accordingly. However, some foreign bonds and especially emerging market bonds held up quite well. As we can see here, the Vanguard World Bond Index (BNDW) outperformed domestic investment-grade bonds year-to-date. We also see that domestic junk bonds (JNK) have been relatively flat while emerging market bonds (EMB) are actually up slightly:

Seeking Alpha

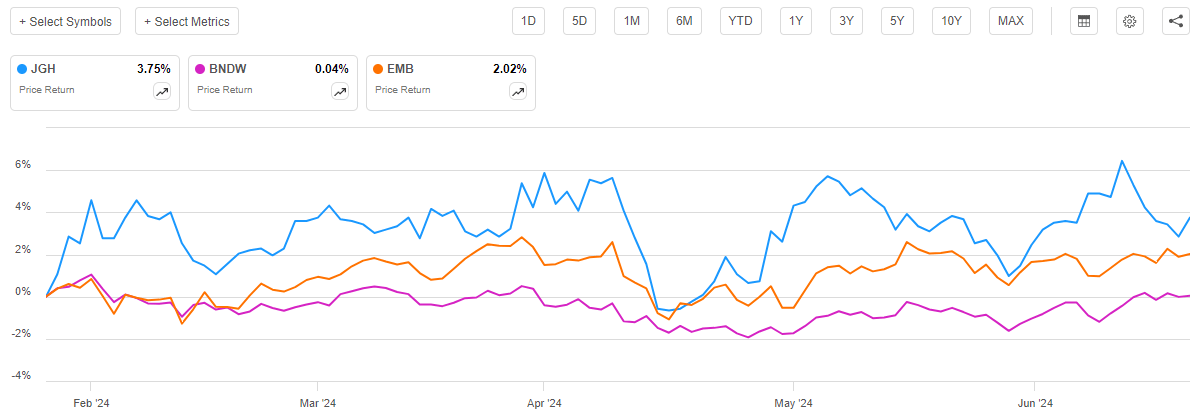

As the Nuveen Global High Income Fund’s name gives the impression that it is investing primarily in high-yield bonds, we can assume that its performance would more closely resemble that of the domestic junk bond and emerging market bond indices. As in, the assumption is that the fund’s share price has been reasonably stable since our previous discussion. However, this is not the case, as shares of this fund have risen by 3.75% since the previous article was published. This fund outperformed both of the international bond market indices shown in the chart above:

Seeking Alpha

This is something that could require further investigation, as it is possible that the fund’s valuation has gotten ahead of itself. It is also possible that this is just a side effect of the leverage that the fund employs, as that would boost the gains that it experienced from any emerging market bonds that it holds.

Investors in the Nuveen Global High Income Fund actually experienced better performance over the past several months than it appears. As I explained in previous articles:

A simple look at a closed-end fund’s price performance does not necessarily provide an accurate picture of how investors in the fund did during a given period. This is because these funds tend to pay out all of their net investment profits to the shareholders, rather than relying on the capital appreciation of their share price to provide a return. This is the reason why the yields of these funds tend to be much higher than the yield of index funds or most other market assets.

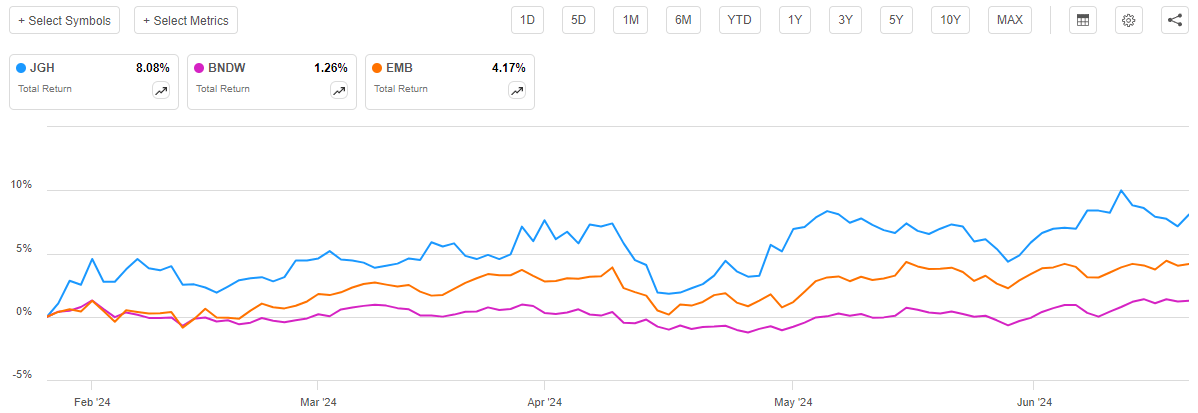

This is especially important for bond funds because bonds by their very nature deliver the majority of their returns via direct payments to their investors. Bond funds then distribute these payments to their own investors. When we include the distributions that were paid out by the Nuveen Global High Income Fund and both of the index funds over the period in question, we get this chart:

Seeking Alpha

As we can clearly see, investors in the Nuveen Global High Income Fund have actually realized a total return of 8.08% over a roughly five-month period, which has obviously substantially beaten both of the global bond indices. It is unsurprising that this would be the case, as most closed-end bond funds tend to outperform indices on a total return basis. This is mostly because of their use of leverage, which allows them to deliver substantially higher yields that directly increase the share price performance.

As we are all well aware, though, a fund’s past performance is no guarantee of its future results. As such, we should still have a look at this fund’s portfolio and positioning in order to make an educated guess about its future trajectory. Fortunately, the fund has released an updated financial report that should provide some very useful updates in this respect. We will be sure to pay close attention to this report over the remainder of this article.

About The Fund

According to the fund’s website, the Nuveen Global High Income Fund has the primary objective of providing its investors with a high level of current income. This makes a lot of sense considering the strategy that this fund employs. The website does an excellent job of explaining the strategy:

The Fund seeks to deliver high current income through a diversified portfolio of global high-income securities that may span the capital structure and credit spectrum, including high-yield bonds from the U.S. and developed and emerging markets, as well as preferred and convertible securities.

Its managed assets will include at least 65% in securities rated below investment grade, at least 40% in securities issued by non-U.S. entities, and up to 25% in debt obligations from issuers located in emerging market countries. Up to 15% may be invested in unhedged non-U.S. dollar denominated bonds; derivatives may be used for hedging purposes only. The Fund uses leverage.

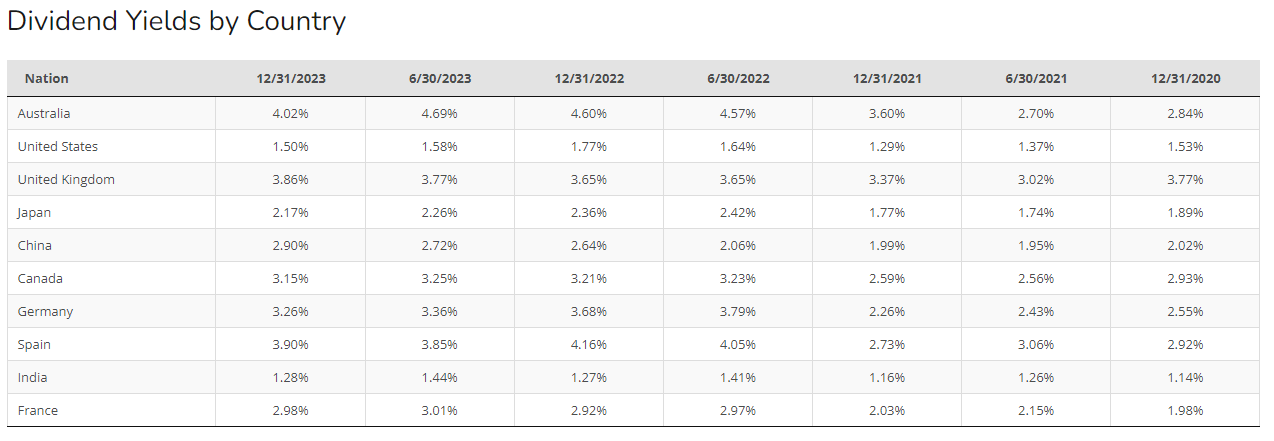

The first paragraph is interesting since it states that the Nuveen Global High Income Fund will invest in high-income securities that span the credit structure. Technically speaking, this could mean debt, preferred equity, or even common stock. The description does state that it wants high-income securities, but that is a fluid definition that could allow dividend-paying common equity to qualify. There are several countries in which the average dividend yield is substantially higher than that of the United States:

Siblis Research

For example, take a look at the average dividend yield of Australian or Spanish common stocks. The average common stock in one of those nations would have a very high yield from the perspective of most American investors. The fund’s description does not explicitly exclude investment in these securities, so it is conceivable that it might purchase them from time to time.

With that said, the fund’s first-quarter 2024 holdings report states that the Nuveen Global High Income Fund had the following asset allocation on March 31, 2024:

|

Asset Type |

% of Total Portfolio |

|

Corporate Bonds |

61.0% |

|

Sovereign Debt |

11.8% |

|

Variable Rate Senior Loan Interests |

8.7% |

|

Institutional Preferred Stock |

8.4% |

|

Contingent Capital Securities |

5.9% |

|

Retail Preferred Stock |

0.9% |

|

Asset-Backed Securities |

0.1% |

|

Common Stock |

0.1% |

|

Repurchase Agreements |

3.1% |

We definitely see that the Nuveen Global High Income Fund is not exclusively a bond fund, which does match up a bit to the statements that I just made about it. In particular, we see that 15.2% of the fund’s assets are invested in preferred stock (contingent capital securities are basically preferred stock issued by European banks). That is not something that we would see in most global bond funds. It should work well from an income perspective, though, since preferred stocks usually have higher yields than bonds issued by the same company. Thus, the presence of these securities should allow the fund to generate a higher level of income than it would if its portfolio was solely invested in bonds.

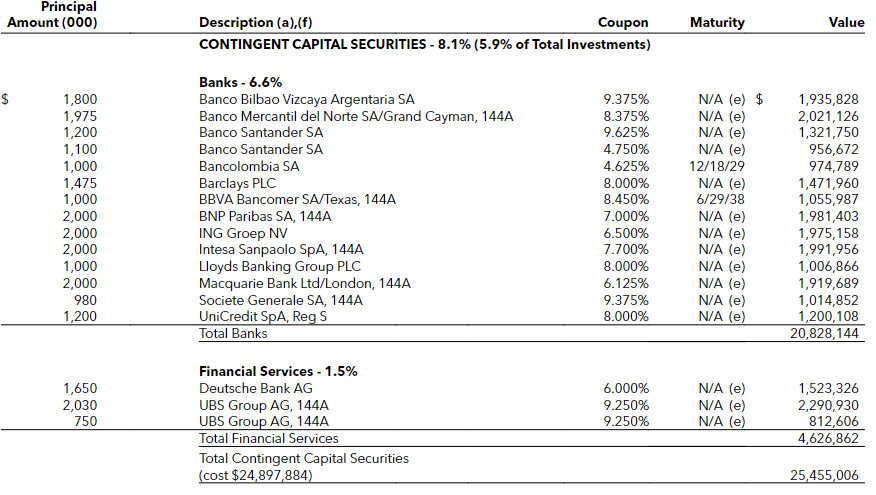

The fund’s description on the website states that at least 40% of its assets will be invested in securities issued by entities in foreign nations. Unfortunately, the fund’s first-quarter 2024 holdings report does not provide a breakdown of the home countries of the issuers in the portfolio. The sovereign debt held by the fund obviously comes from foreign nations (funds trading in the United States do not call U.S. Treasuries “sovereign debt”) and the contingent capital securities held by the fund are all issued by foreign entities:

Fund Q1 2024 Holdings Report

We can immediately see that all of those, which are all of the contingent capital securities held by the fund, are European banks. That will normally be the case because American banks do not generally issue contingent capital securities. The regulations between the United States and the European Union differ in that regard and result in different types of securities being favored or disfavored by banks on each continent.

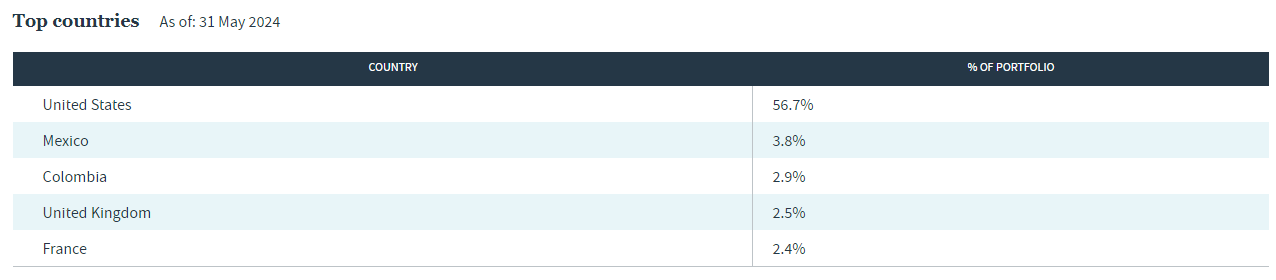

However, the sovereign debt plus the contingent capital securities only total 17.7% of assets. That is well below the 40% that the fund claims must be invested in foreign securities. A look across the rest of the portfolio, however, reveals that some of the corporate bonds, some of the preferred stock, and some of the common stock allocations are invested in securities from foreign issuers. When we look across the whole portfolio, we get this country allocation:

Nuveen Investments

We can immediately see that 56.7% of the fund’s assets are invested in securities from American issuers. That leaves 43.3% invested in securities from foreign issuers, which does satisfy the 40% requirement. That is, however, a lower weighting to foreign securities than the fund had when we discussed it in January. At that time, the fund had a 55.4% weighting to the United States and a 44.6% weighting to foreign-issued securities. This is somewhat disappointing as it weakens our thesis of using the fund as a way to obtain international diversification. After all, the fund’s management appears to be shifting the portfolio towards domestic securities when our thesis basically requires that it go in the other direction.

The shift towards domestic securities appears to be a conscious choice on the part of the fund’s management. As we saw in the introduction, foreign bonds have actually outperformed domestic bonds year-to-date. This is partly because we have already seen a few foreign central banks, such as those in the European Union and Canada, reduce their benchmark interest rates and add a bit of support for bond prices. Emerging market bonds actually benefit from the fiscal and monetary problems with the U.S. dollar, so that explains some of the strength that we have seen there. When we consider that foreign bonds are outperforming domestic ones, the only possible way for the fund to have increased its domestic weighting is if it actively sold some of the foreign bonds that it previously held and used the proceeds to purchase domestic bonds. That is not what we want to see if we are trying to increase our own exposure to foreign bonds.

The Nuveen Global High Income Fund has a bit lower foreign allocation than many of its peers:

|

Fund Name |

Foreign Weighting |

|

Nuveen Global High Income Fund |

43.3% |

|

BrandywineGLOBAL – Global Income Opportunities Fund |

52.4% |

|

DoubleLine Income Solutions Fund |

~40%* |

|

PIMCO Dynamic Income Opportunities Fund |

24.08% |

|

Western Asset Global Corporate Defined Opportunity Fund |

44.59% |

|

abrdn Global Income Fund |

~85%** |

* The foreign weighting of the DoubleLine Income Solutions Fund is uncertain. The most recent documentation provided by the fund’s sponsor states that 39.87% of assets are invested in emerging markets, with no specific weighting provided for developed market bonds. Third-party sources put the fund’s non-U.S. allocation at 29% to 42%. Considering this information, the fund’s non-U.S. weighting is probably in the low-40s, but this is uncertain.

** The abrdn Global Income Fund has 17.6% of its assets invested in North American securities, according to the most recent fact sheet. It does not specify how that is divided up among the United States, Canada, and Mexico. 85% seems to be a reasonable estimate for its non-U.S. exposure, but the actual value could be 100 to 200 basis points higher or lower.

We can immediately see that there are a few funds on this list that have a much higher allocation to non-U.S. assets than the Nuveen Global High Income Fund. This further weakens our thesis of using this fund as a way to increase the international diversification of our portfolios. After all, it appears that there are quite a few closed-end funds in the market that would prove to be more effective at this particular task. There is, of course, always the chance that the Nuveen Global High Income Fund will increase its foreign exposure so that it is more in line with the best of its peers (the BrandywineGLOBAL and the abrdn funds), but historically this fund has not usually run much above the 40% minimum foreign asset exposure that it is mandated to have. As such, investors who are looking for a single-fund solution to increase their international exposure may be better off looking elsewhere.

Leverage

As is the case with most closed-end funds, the Nuveen Global High Income Fund employs leverage as a method of boosting the effective yield that it earns from its portfolio. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase bonds issued by entities around the world. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

However, it is important to note that the use of leverage is somewhat less effective today with domestic borrowing rates at 6% than it was a few years ago when money could effectively be borrowed for nothing. This is because the difference between the rate at which the fund can borrow and the yield that it receives on the purchased assets is much narrower than it once was.

The use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like a fund’s leverage to exceed a third as a percentage of its assets for this reason.

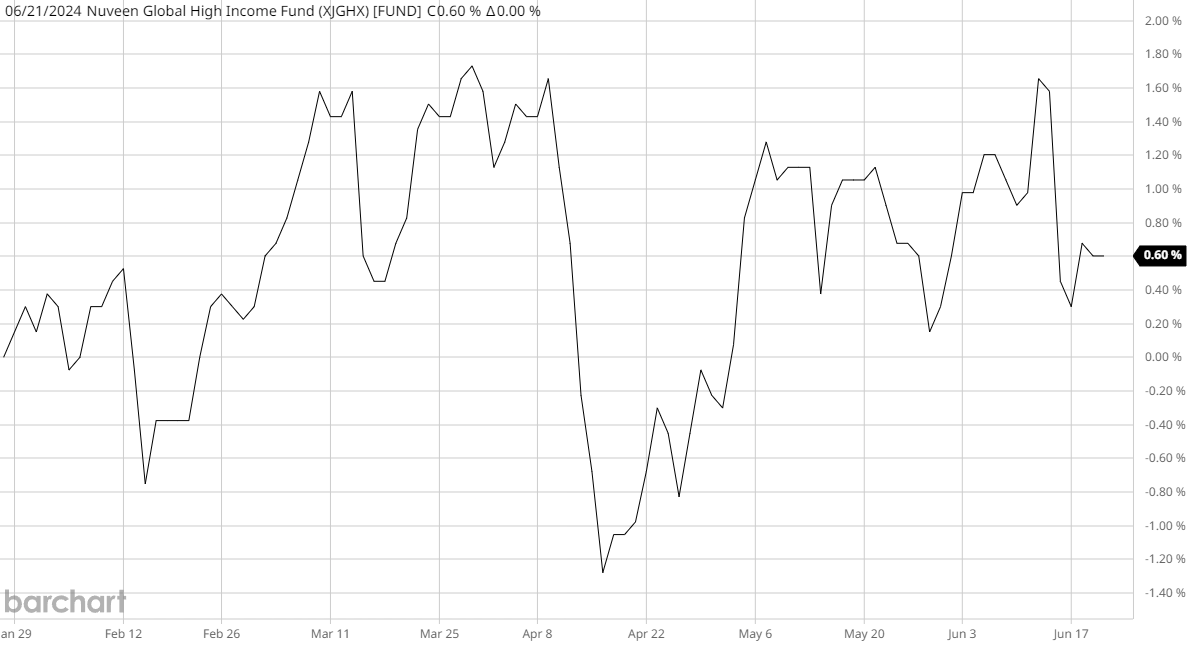

As of the time of writing, the Nuveen Global High Income Fund has leveraged assets comprising 27.75% of its portfolio. This is pretty similar to the 27.99% leverage ratio that the fund had the last time that we discussed it, which is a bit confusing at first glance. After all, we saw that the fund’s share price increased by 3.75% over the period. This could suggest that the fund’s share price performance was actually much better than the underlying portfolio delivered.

This was indeed the case, as we can clearly see in this chart that shows the performance of the fund’s portfolio from January 26, 2024 (the publication date of the previous article) until today:

Barchart

As we can clearly see, the portfolio of the Nuveen Global High Income Fund only increased in size by 0.60% over the period. That was much less than the share price gain, which suggests that the shares have become much more expensive over the past few months. This will be discussed later in this article. For now, we can see that the fund’s portfolio has been relatively stable overall, which explains why its leverage did not change much.

The Nuveen Global High Income Fund does not appear to be overleveraged relative to its peers:

|

Fund Name |

Leverage Ratio |

|

Nuveen Global High Income Fund |

27.75% |

|

BrandywineGLOBAL – Global Income Opportunities Fund |

42.31% |

|

DoubleLine Income Solutions Fund |

21.77% |

|

PIMCO Dynamic Income Opportunities Fund |

41.08% |

|

Western Asset Global Corporate Defined Opportunity Fund |

34.29% |

|

abrdn Global Income Fund |

30.52% |

(all figures from CEF Data)

As we can clearly see, the Nuveen Global High Income Fund has a lower level of leverage than all except for one of its peers. This is a very clear sign that the fund is not employing an excessive amount of debt in its overall strategy. For the most part, this fund seems to be striking a pretty good balance between the risks and the potential rewards of leverage, and investors should not need to lose too much sleep having this fund in their portfolios.

Distribution Analysis

The primary objective of the Nuveen Global High Income Fund is to provide its investors with a very high level of current income. To this end, the fund pays a monthly distribution of $0.1035 per share ($1.2420 per share annually). This gives the fund a 9.76% yield at the current price. As we saw in the introduction, this is not a particularly impressive yield compared to its peers. It should still be enough to appeal to many income-seeking investors, however.

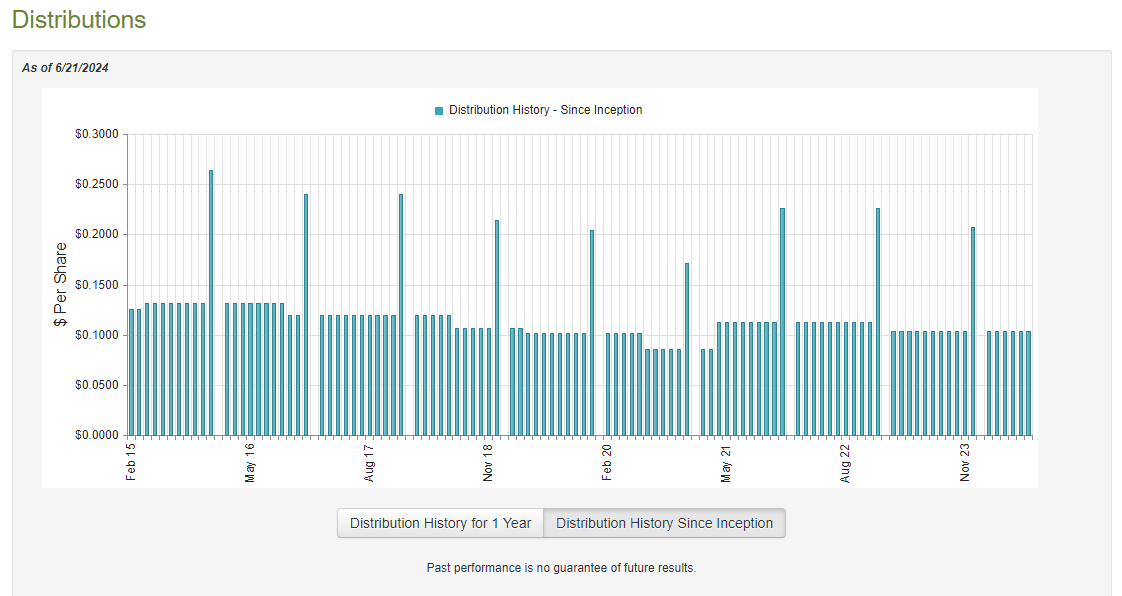

The fund has not been especially consistent with its distribution over its history:

CEF Connect

From the previous article:

The fact that the fund’s distribution has regularly changed might prove to be a turn-off for those investors who are seeking to receive a safe and consistent level of income from the assets in their portfolios. This is a group that likely includes many retirees and similar investors due to the fact that they are frequently dependent on the income from their portfolios to support themselves. However, a variable distribution is not unusual for a bond fund, as the profits of these funds tend to be highly influenced by interest rates and similar factors that frequently change and are completely out of the fund’s control. As such, the fund’s distributions may vary over time, but it can still usually provide a high level of income that can be combined with income from other sources to support yourself.

As mentioned earlier, the fund released an updated financial report following the publication of my previous article on it. This financial report corresponds to the full-year period that ended on December 31, 2023, so it will unfortunately not include any information about the fund’s performance year-to-date. However, this is still a more recent report than the one that we had available the last time that we discussed the fund so it should work pretty well to provide an update.

For the full-year period that ended on December 31, 2023, the Nuveen Global High Income Fund received $329,016 in dividends and $29,959,914 in interest from the assets in its portfolio. This gives the fund a total investment income of $30,288,930 for the period. The fund paid its expenses out of this amount, which left it with $18,999,710 available for the shareholders. This was not sufficient to cover the $28,786,322 that the fund paid out in distributions during the period.

Fortunately, the fund was able to make up the difference through capital gains. For the full-year period, the Nuveen Global High Income Fund reported net realized losses of $11,956,041, but these were more than offset by net unrealized gains totaling $35,188,563. Overall, the fund’s net assets increased by $13,445,910 after accounting for all inflows and outflows over the period.

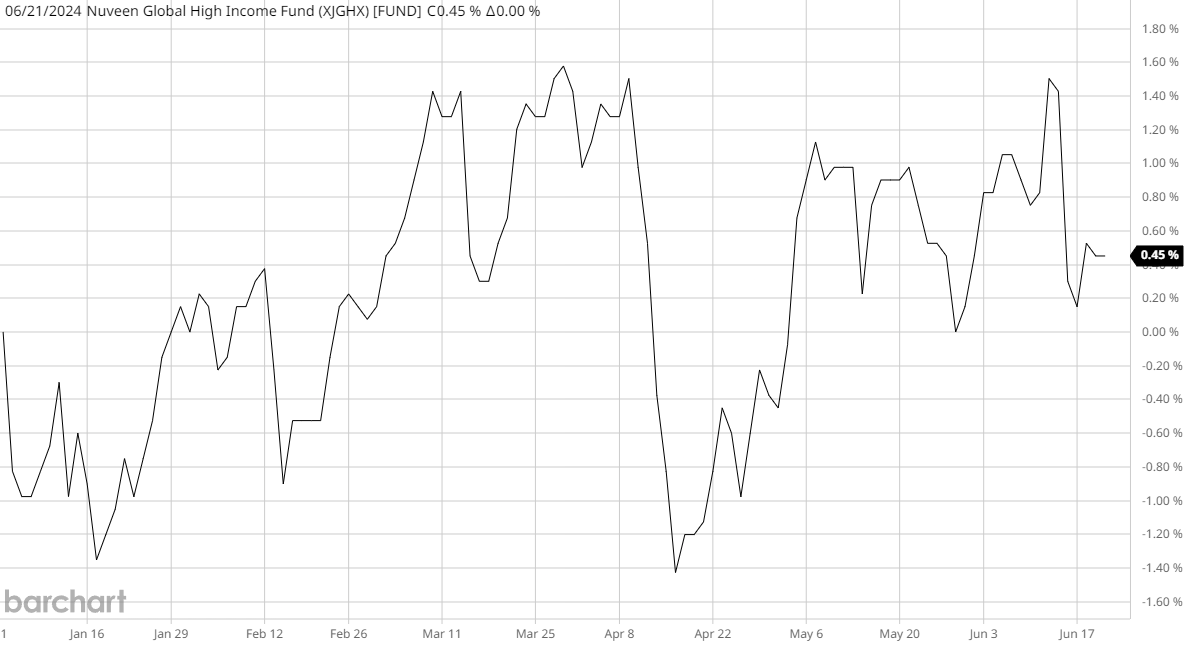

As we can see, the fund managed to cover its distributions over the course of 2023. However, it was only able to do that due to unrealized capital gains, which are not necessarily a reliable source of distribution coverage. After all, these gains can be quickly erased by a market correction. This does not appear to be the case with this fund, however. This chart shows the fund’s net asset value from December 31, 2023, until today:

Barchart

As we can clearly see, the fund’s net asset value has increased by 0.45% since the closing date of its most recent financial report. This clearly shows us that the fund has managed to fully cover all of the distributions that it has paid out year-to-date with a small amount of investment profit left over.

Valuation

Shares of the Nuveen Global High Income Fund currently trade at a 4.79% discount on net asset value. This is rather unattractive compared to the 6.06% discount that the fund’s shares have averaged over the past month. It also looks very expensive compared to the 7.64% discount that the shares had at the time of our last discussion.

It may be possible to get a better price by waiting for a market correction.

Conclusion

In conclusion, the Nuveen Global High Income Fund has delivered a far better market performance than its portfolio performance justifies over the past several months. The fund’s portfolio has been relatively flat, but its share price has delivered reasonably strong gains. This might put the fund at risk of a correction at some point, so investors may wish to remain wary.

The fund advertises itself as a global fund that invests in assets from all around the world. It does that, but it appears to have a stronger focus on the United States than some of its peers. This makes it less desirable than it could be for investors for whom international diversification is important. The fact that its yield is lower than that of some peers reduces its appeal further.

Overall, this is not a bad fund, but there is nothing really remarkable about it right now.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.