Sundry Pictures

Written by Nick Ackerman.

Texas Devices Included (NASDAQ:TXN) would not make the thrilling and flashy chips that energy synthetic intelligence, or AI. They don’t seem to be catching any of these headlines that we have been persistently seeing from the opposite facet of the chip world, particularly Nvidia (NVDA).

As an alternative, they make the boring chips which are utilized in on a regular basis tools throughout us. This tends to make them extra delicate to the general financial system and the outlook of the place we may very well be heading on that entrance. Given the Fed’s need to decelerate the financial system in an effort to attempt to tame inflation, the macroeconomic outlook could be for a weaker financial system going ahead.

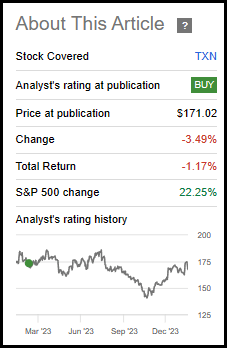

That is been the theme of the final yr as effectively. When we previously discussed this identify, they have been primarily in the identical scenario they’re now, as analog chips proceed to have a weak demand. Maybe it’s unsurprising, then, to see that shares on a complete return foundation have primarily moved nowhere since that prior replace.

TXN Efficiency Since Prior Replace (In search of Alpha)

Nonetheless, I imagine that Texas Devices remains to be value investing in. Maybe much more worthwhile, as day by day goes by, we needs to be getting nearer to that inevitable restoration for the corporate.

Newest Outcomes And Ahead Outlook

Reflecting on the persevering with actuality of weak point within the chip area, Texas Devices lately posted their latest quarterly results and noted weakness within the industrial area. Income within the automotive phase was additionally seen as comfortable and declining, although that was after beforehand robust development. Right here is the recap from their This autumn earnings call:

First, the economic market was down mid-teens as we noticed that growing weak point. The automotive market was down mid-single-digits after 3.5 years of very robust development. Private electronics was about flat. And subsequent, communications tools was down low-single-digits. And lastly, enterprise methods grew low single digits.

Industrial and automotive make up the majority of TXN’s whole revenues, as they famous these contributed to 74% of 2023’s income.

The TXN Q4 results weren’t terrible when it comes to expectations. The corporate noticed a slight beat when it comes to EPS and a reasonably mild miss on income estimates. That did signify a income decline of 12.6% year-over-year, even when it was solely a lightweight miss of analyst expectations.

The steerage of anticipating weak point to proceed, together with comfortable steerage that missed estimates for Q1, despatched shares downward. Clearly, the most recent outcomes are going within the incorrect path for shareholders and firm development. With a continued outlook remaining comfortable in 2024, the quick time period did not present any confidence both, and shares offered off after the preliminary launch. It additionally probably did not assist that TXN shares have been heading meaningfully greater into the earnings report, both.

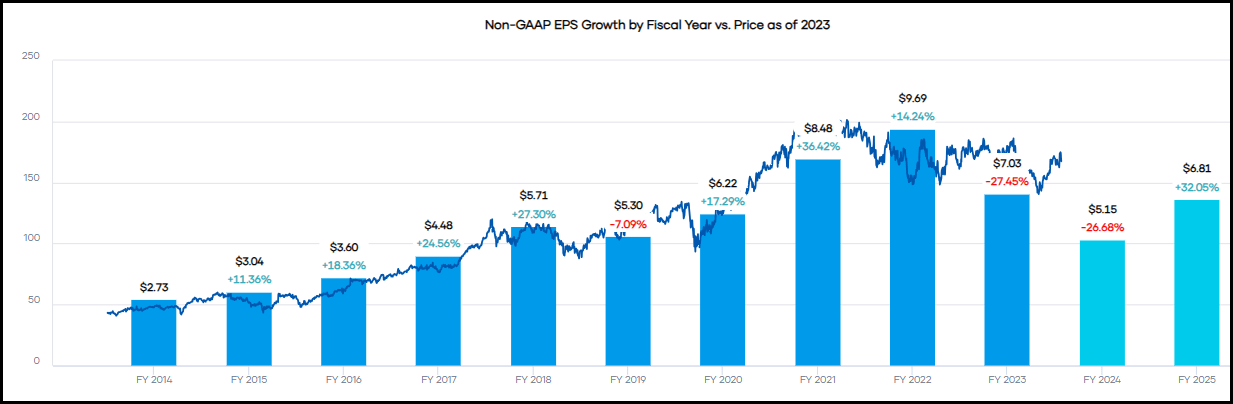

Nevertheless, in the long term, searching to 2025, analysts imagine {that a} return to development can happen.

TXN Earnings Historical past (Portfolio Perception)

Going out even additional past 2025, analysts count on that restoration will proceed with earnings rising all over 2030. Nevertheless, it needs to be famous that 2029 and 2030 solely have a single analyst’s expectation. The nearer-term years can have a bit extra weighting, as there’s a bigger variety of analysts offering consensus.

TXN Earnings Estimates (In search of Alpha)

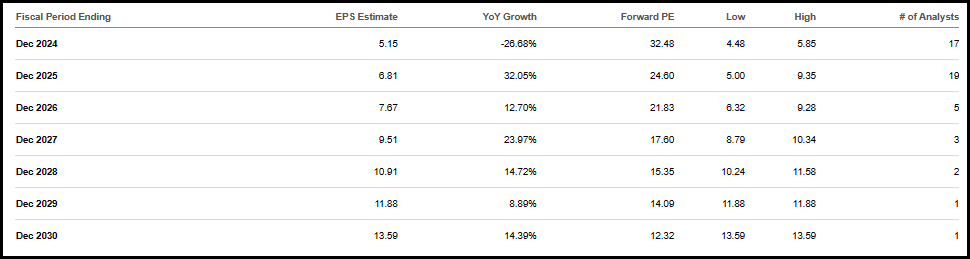

This all factors to a restoration that’s more likely to happen sooner or later. Given the shorter-term outlook of the subsequent yr, it will seem that TXN is considerably overvalued.

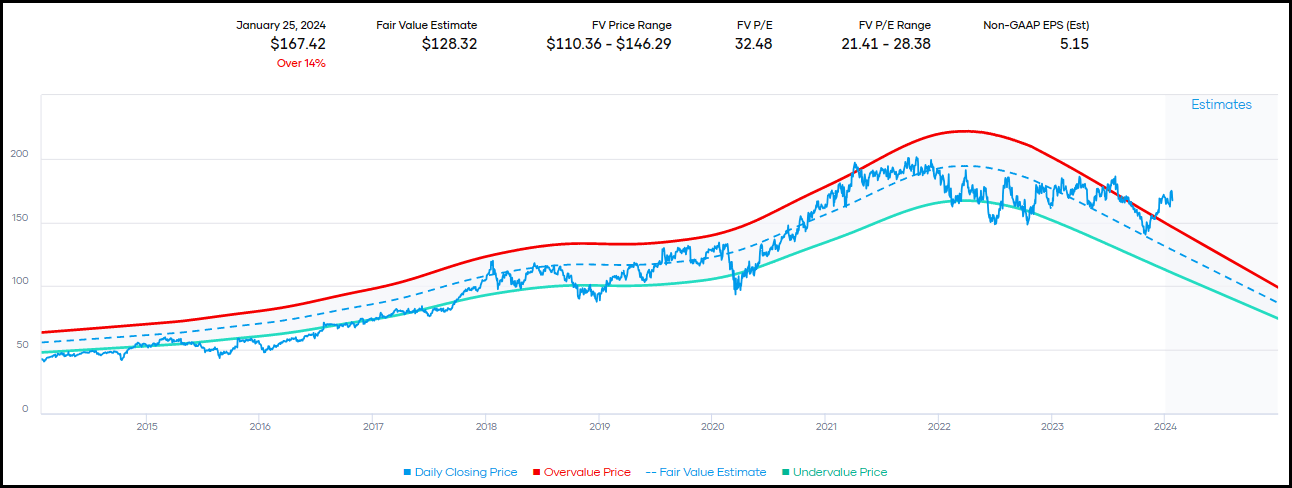

TXN Truthful Worth Vary (Portfolio Perception)

The corporate is carrying a ahead P/E of almost 32.5x. That may be in comparison with the historic P/E vary of 21x to 28x.

That stated, if the earnings estimates do begin to get hit trying additional out, P/E can begin to come down rapidly. Actually, in 2025, we might see the ahead P/E are available in at lower than 25x – placing it proper close to the center of the historic truthful worth vary. Going out to 2026, we’re pushing under 22x, indicating a stage close to the underside of its historic truthful worth vary.

That is all provided that the corporate delivers on the present estimates. TXN has an extended historical past of beating most quarterly earnings estimates. With earnings revisions shifting massively decrease, it seems like that might point out setting the corporate up for that pattern to proceed. Nevertheless, when the restoration does begin to take maintain, we’ll probably begin to see upward revisions. Proper now, Texas Devices is in a tough interval, and I imagine that is when it’s value shopping for.

Dividend

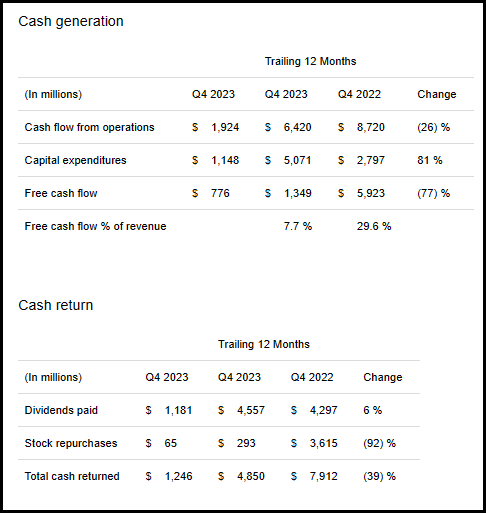

Free money circulate additionally took a considerable hit with the most recent quarter, and has been trending decrease within the final couple of years. Nevertheless, that is not too shocking, because it merely follows the general downward trajectory of earnings and income for the corporate. Within the newest quarter, free money circulate, or FCF, got here to $776 million in comparison with the $1.246 billion returned to shareholders. For the yr, we noticed FCF at $1.349 billion relative to the $4.85 billion returned again to shareholders.

They scaled again almost all of their inventory repurchases, probably in an effort to steadiness this shortfall.

TXN Money Era Vs. Money Return (Texas Devices)

So, which means protection of the dividend has been weak. We are actually at a time the place FCF is not protecting the dividend.

On the similar time, I do not imagine that they are going to be trying to lower the payout simply but – at the least in the event that they themselves can even take a longer-term outlook and see a return to development going ahead.

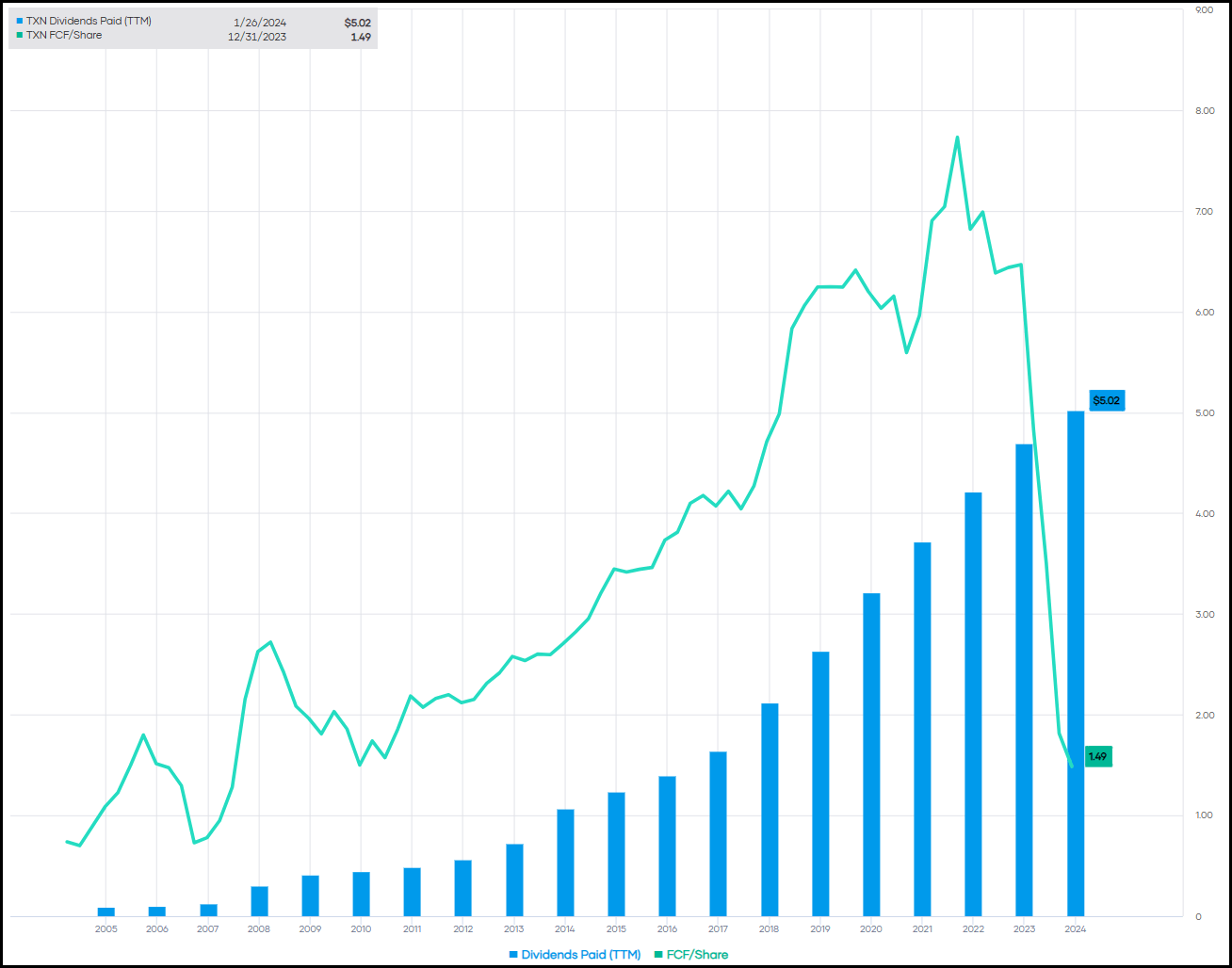

The corporate has a history of elevating its dividends, and that historical past goes again 20 years. That features simply in This autumn – once they usually enhance the dividend – seeing a 5% bump. I do not imagine they will wish to see this pattern of rising dividends finish.

TXN FCF/Share Vs. Dividend (Portfolio Perception)

Additional, it was a major ramp-up in CAPEX and never simply money circulate from operations alone that took a success on the corporate’s FCF within the newest yr. Money flows from operations declined 26%, however the CAPEX elevated 81%, leading to a 77% decline in FCF.

This was introduced up within the newest convention name as effectively, when an analyst requested concerning the FCF being under the dividend stage.

Right here was the CFO’s response:

first, I’d level you to our working money. Our enterprise mannequin could be very robust and our working money circulate could be very robust and it helps our funding for development by means of the cycle. So clearly with the degrees of CapEx that we now have proper now, that hits the free money circulate. However huge image perceive and take a look at the working money, even in a depressed setting with the income, depressed working money circulate could be very robust. We even have very robust steadiness sheet. And we simply completed the yr at $8.6 billion. You already know, in terms of repurchases, I’d take you to our aims on capital administration for money return, and our goal is to return all free money circulate by way of dividends and repurchases. Every a kind of has completely different aims on dividends and repurchases, however we now have a very good observe document over a few years of doing each of these.

They plan to proceed with CAPEX at this stage, too, by means of 2026. Like most corporations, they proceed to speculate for future development. So, which means the reduction on that facet of the equation is not going to finish within the quick time period. On the longer-term horizon, it ought to finally taper downward.

Alternatively, it may imply dividend development may pause ought to restoration not take maintain as anticipated or be one thing just like the token penny elevate. That might probably be a prudent transfer in an effort to maintain the company’s balance sheet sound.

Conclusion

Being that the analog chip firm is out of favor – persevering with to submit weak outcomes as restoration takes longer and longer, and steerage for 2024 is not an excessive amount of prettier – I imagine it presents a compelling time to contemplate including to at least one’s place or initiating a place. That’s, if one at the least believes a turnaround and restoration within the analog chip area is coming within the subsequent yr or two.

I’m not certain when a backside shall be in, however that is the place using a dollar-cost common method may very well be applicable. Choosing up and including to a Texas Devices Included place over the approaching yr may assist even with some shares at greater costs but additionally decrease costs ought to they arrive.