Torsten Asmus

I’ve coated a number of the extra essential trends impacting bonds and bond ETFs these previous few years, as Federal Reserve hikes have led to wild swings in rates of interest and broader bond market circumstances. Final time I coated these points for the Vanguard Whole Bond Market Index Fund ETF (NASDAQ:BND), nominal charges have been excessive, actual charges have been low, the yield curve was inverted, and credit score spreads have been barely narrower than common. A few of these developments have reversed course, some stay broadly the identical. Proper now, the next stands out about bond market circumstances.

Charges are at their highest ranges in a long time, throughout bond sub-asset courses.

The Federal Reserve will possible minimize charges within the coming months. Below present steering, charges would stay at above-average ranges for a number of years.

Longer-term bonds yield lower than shorter-term securities as traders count on vital fee cuts within the coming months.

Credit score spreads have narrowed at the same time as default charges rise, though neither development is critical. Thus far, not less than.

In my view and contemplating the above, bonds stay a robust asset class, and a broad purchase. Funding-grade bonds look extra compelling than riskier high-yield bonds, as a result of slender credit score spreads and rising default charges. Shorter-term bonds additionally look extra compelling, as a result of their increased yields and market expectations of fee cuts.

I will be specializing in BND for the rest of this text, as a stand-in for the broader bond market. Nonetheless, every part right here ought to apply to bonds as an asset class and to most bond funds in roughly equal measure.

BND – Fast Overview

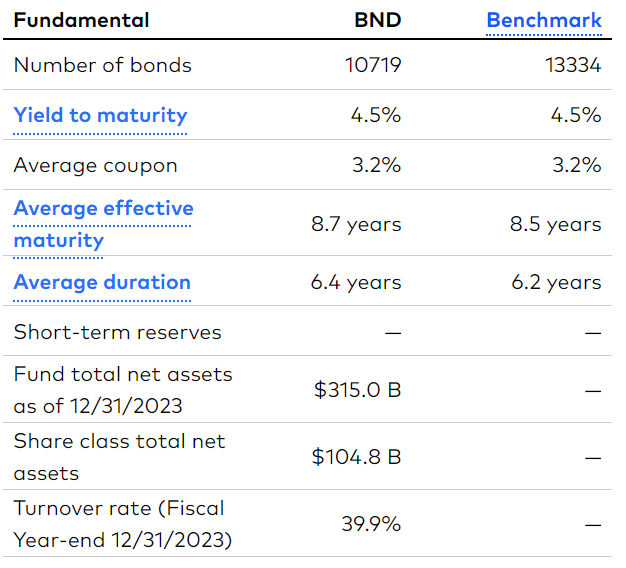

BND is a diversified bond index ETF, monitoring the Bloomberg U.S. Aggregate Bond Index. It’s a comparatively easy, broad-based index, concentrating on the U.S. bond market, and together with treasuries, investment-grade bonds, mortgage-backed securities (MBS), and different government-related securities. It excludes high-yield company bonds, with these accounting for round 8% of the U.S. bond market.

BND itself invests in over 10,000 securities from most related bond sub-asset courses. It’s also the most important bond ETF out there, with a whopping $315B in AUMs. Second largest is the iShares Core U.S. Mixture Bond ETF (AGG) with $100B, monitoring the identical index as BND.

BND BND

BND offers traders with broad-based publicity to U.S. bonds. Let’s take a look at some current developments impacting these securities.

U.S. Bond Market – Latest Developments

Elevated Charges

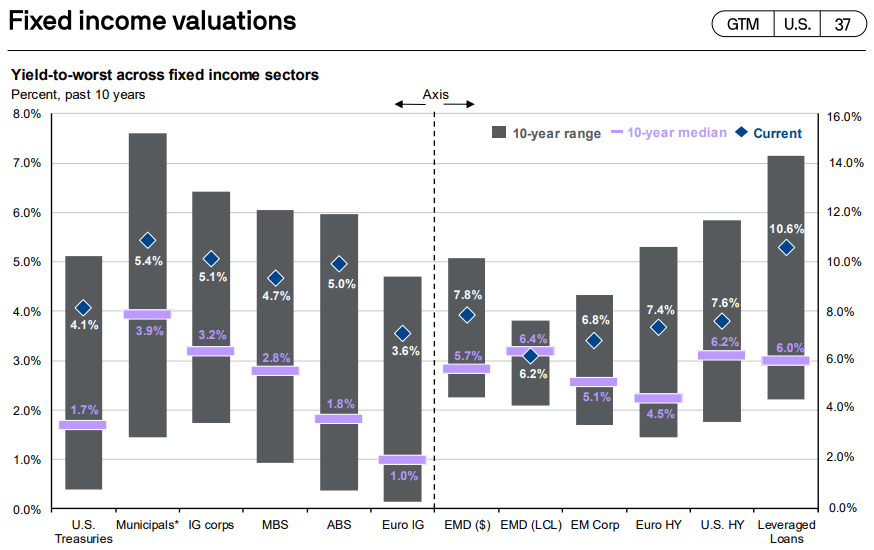

Federal Reserve charges rose throughout most of 2022 and 2023, to fight inflation. Larger Fed charges triggered market charges to spike throughout asset courses, with only a few exceptions. Presently, charges are round 2.0% – 3.0% increased than common, relying on the asset class. Senior loans are the best, at 10.6%.

JPMorgan Information to the Markets

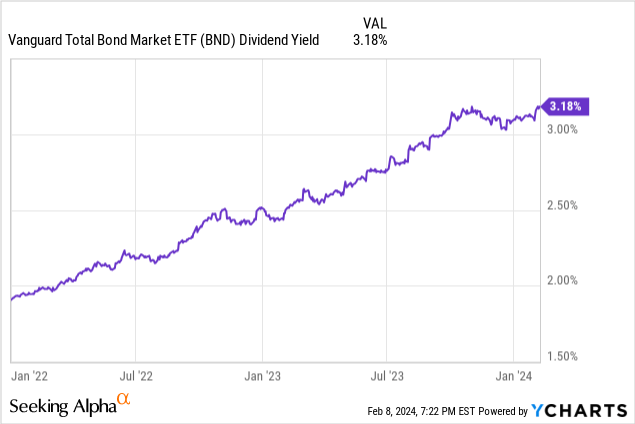

BND’s dividends have grown at a 12% CAGR since early 2022, with yields rising by round 1.3%. Below present circumstances, the fund’s yield ought to rise one other 1.2% within the coming years, as its older, lower-yielding bonds are changed with newer, higher-yielding options. Figures taken from fund information, and in keeping with the graph above. A lot will depend upon future Fed coverage, nonetheless.

Contemplating the above, I imagine that bonds are a robust asset class, and a broad purchase. Completely different traders would possibly favor several types of bonds, with risk-averse short-term traders sticking to treasuries, these in search of a bit extra yield specializing in high-yield bonds or senior loans.

Doubtless Federal Reserve Cuts

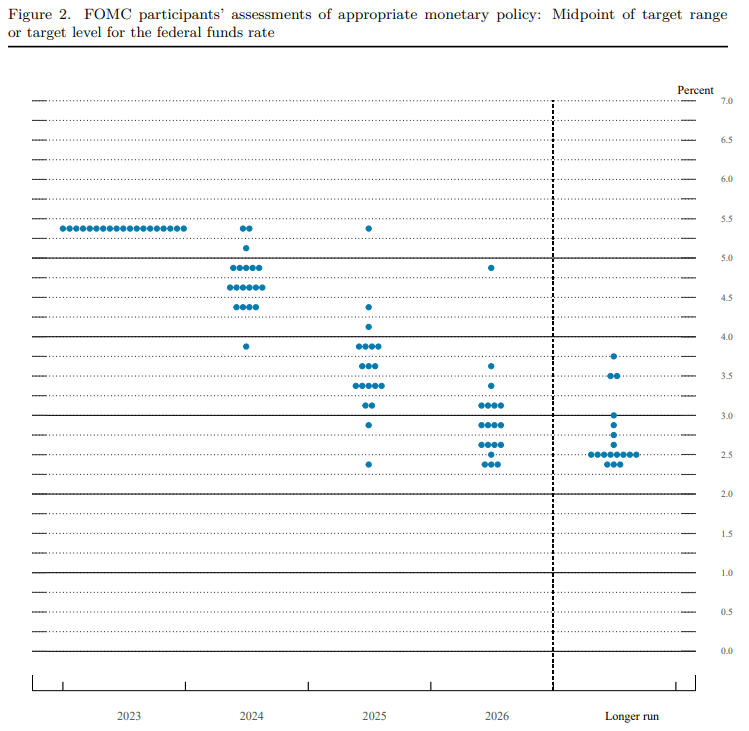

The Federal Reserve is guiding for 3 fee cuts this yr, a number of extra within the subsequent few years, and a 2.5% terminal fee.

Federal Reserve

Decrease Federal Reserve will virtually actually result in decrease rates of interest on roughly all short-term and variable fee asset courses, together with t-bills, CDs, floating fee treasuries, senior loans, CLO debt tranches, and others. Specifics fluctuate, however most of those ought to proceed to supply robust yields even after the Fed cuts charges.

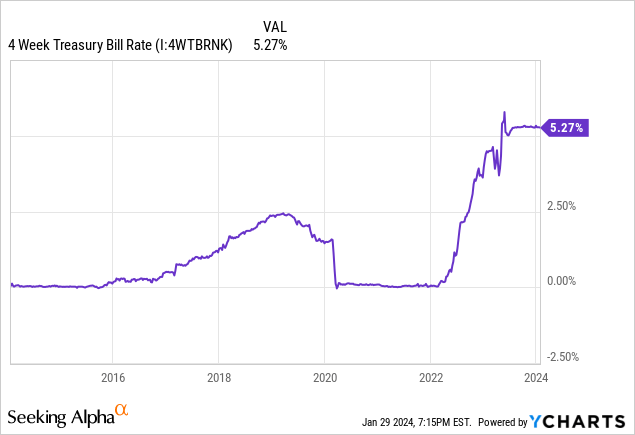

For example, present Fed steering implies t-bill charges of 4.50% – 4.75% at years finish, fairly good on an absolute foundation, and far increased than throughout a lot of the previous decade.

Knowledge by YCharts

As one other instance, senior loans presently yield 3.0% greater than high-yield company bonds. Below present Fed steering, senior loans would yield round 2.0% – 2.5% greater than these bonds at years finish, nonetheless a really wholesome unfold.

JPMorgan Information to the Markets

Vital fee cuts would result in additional declines in yields and dividends, nonetheless.

Decrease Federal Reserve charges ought to additionally result in decrease charges on most medium and long-term bonds, together with treasuries, investment-grade bonds, high-yield bonds, and municipals. Importantly, a lot will depend upon the magnitude and timing of any future cuts. Vital, swift fee cuts would virtually actually lead to decrease market charges, much less so for extra smaller, slower cuts. It’s because the market expects vital fee cuts already and is pricing bonds accordingly.

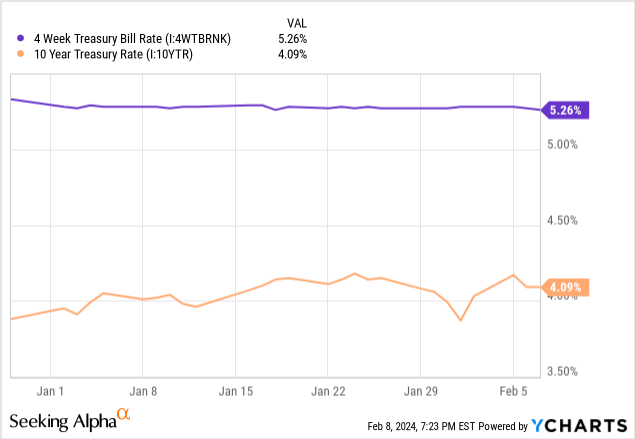

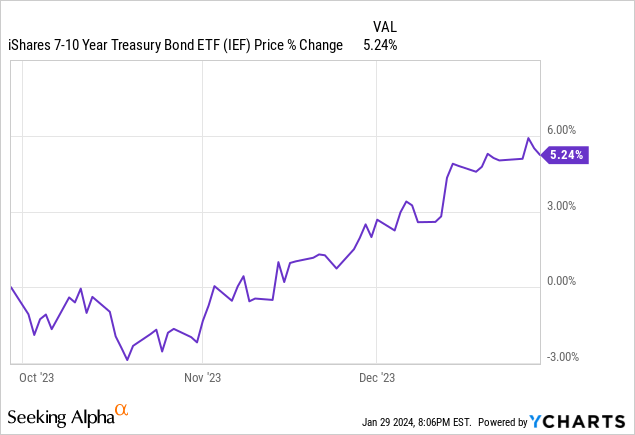

For example, 10Y treasuries already yield lower than t-bills, as a result of traders count on fee cuts within the close to future. Decrease Fed charges won’t essentially result in decrease 10Y treasury charges as a result of these already yield lower than Fed charges.

As one other instance, treasury costs rose 5.2% throughout 4Q2023, as a result of dovish Fed steering. At the least some positive aspects have already occurred, so additional positive aspects are removed from assured.

Knowledge by YCharts

As talked about beforehand, the magnitude and timing of any future cuts issues. I might not count on 10Y treasury yields to say no if the Fed cuts charges by 0.25% per yr for the following few years, however I might count on them to plummet if the Fed cuts charges to zero.

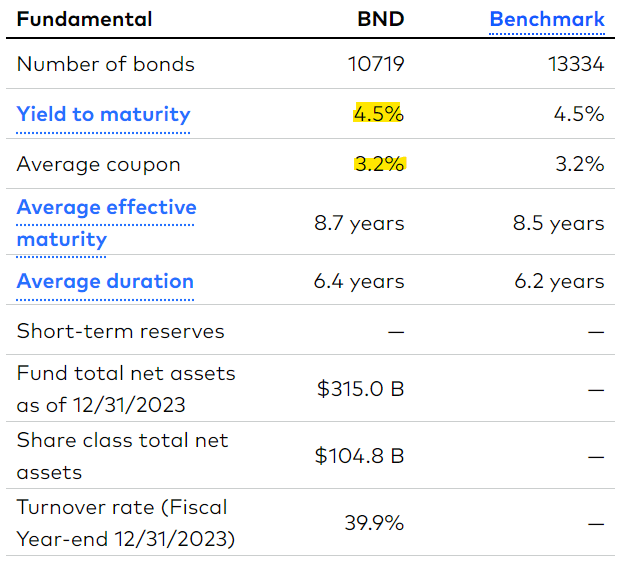

For BND itself the state of affairs is a little more sophisticated. Proper now, assuming no modifications to Fed or market charges, the fund ought to see its yield improve by round 1.3% within the coming years. It’s because the fund nonetheless holds a number of previous bonds from earlier than the Fed hiked, with low coupon charges. General, the fund’s present portfolio has a median coupon fee of three.2%, however a yield to maturity of 4.5%. As bonds mature that 3.2% ought to turn into a 4.5%. At the least assuming no modifications to market rates of interest.

BND

Contemplating the above, for BND’s dividends to say no market rates of interest must go down by extra than 1.3%.

As BND invests in fixed-rate bonds, modifications to market rates of interest ought to have roughly zero affect on the yield of its present portfolio, or on short-term fund dividends. These would solely begin to change because the fund’s bonds begin to mature, and get changed by newer, lower-yielding ones. The method ought to begin a couple of months after charges change however take a number of years to finalize. For example, the Fed began to hike in early 2022, and the fund’s dividends have solely grown by round half as a lot as anticipated.

General, I do not count on BND’s dividends to considerably decline this yr or the following. An excessive amount of dividend development is anticipated to occur as a result of prior hikes, and it’ll take months / years for future cuts to affect the fund’s dividends. Identical is true for many different medium and long-term bond funds. A lot will depend upon future Fed coverage, nonetheless.

Credit score Spreads and Default Charges

Credit score spreads have narrowed since early 2023 and are presently at traditionally below-average ranges. Spreads are round 1.0% narrower than the current common, virtually 2.0% than the long-term common.

JPMorgan Information to the Markets

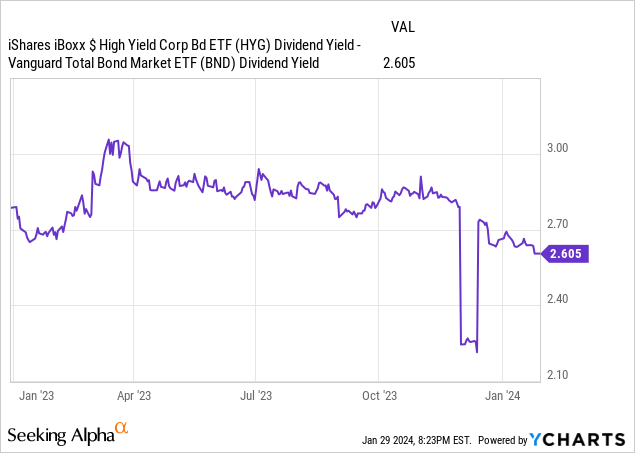

Spreads between benchmark high-yield company bond ETFs and BND itself have additionally narrowed since early 2023, with some volatility.

Knowledge by YCharts

Narrower credit score spreads improve the relative worth proposition of investment-grade bonds and bond funds, together with BND, over riskier high-yield company bonds and bond funds.

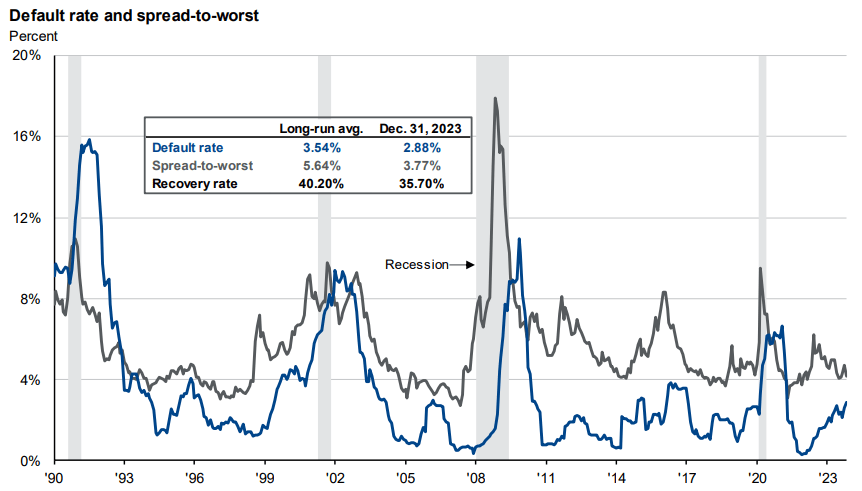

Default charges have additionally risen, from near zero in 2021, to three.0% – 4.0%, as per J.P. Morgan and S&P data. Default charges are considerably increased than lately, maybe a bit decrease than long-term historic averages.

Larger default charges additionally make investment-grade bonds stronger than high-yield bonds, not less than relative to the previous. Funding-grade bonds are much less impacted by rising default charges, as a result of being issued by comparatively robust, resilient corporations. BND itself virtually completely invests in investment-grade bonds. Excessive-yield bonds are issued by weaker, riskier corporations, and extra impacted by rising default charges.

The mixture of narrower credit score spreads and better default charges make high-yield company bonds much less engaging as an asset class over investment-grade bonds. I am personally fairly bullish on the economic system so stay bullish on high-yield bonds, however these two developments do level in the wrong way.

Conclusion

A number of essential developments and developments are impacting bonds and bond funds, together with BND.

Charges are at their highest ranges in a long time, throughout asset courses.

The Federal Reserve will possible minimize charges within the coming months. Market charges ought to decline as nicely, though a lot will depend upon the magnitude and timing of future cuts.

Longer-term bonds yield lower than shorter-term securities as traders count on vital fee cuts within the coming months.

Credit score spreads have narrowed at the same time as default charges rise, though neither development is critical.

In my view, and contemplating the above, bonds stay a robust asset class, and are a broad purchase.